(Bloomberg Opinion) -- Compared with stock buyers, bond investors are usually considered a rational bunch. They scour through a company’s financials, measure its cash flows and calculate their odds of recovery in the event of a default.

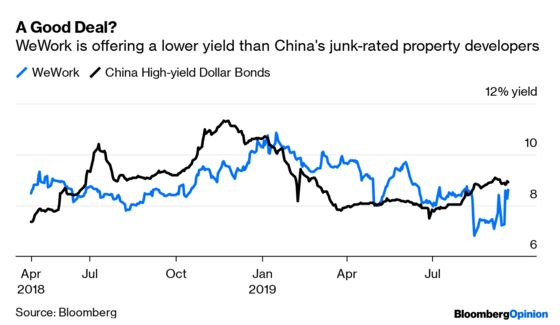

So when it comes to WeWork’s $669 million junk-rated debt due 2025, which pays less than an 8% coupon, you can’t help but wonder: Who owns these things? This is a company that managed to burn through more than $2 billion of cash last year, thanks to an expansion spree. Its Ebitda margin, at -75%, effectively says that for every dollar the co-sharing work-space operator earns, it manages to spend $1.75.

WeWork’s biggest backers are getting cold feet, and the once hotly anticipated IPO of its parent company, We Co., is being delayed. Now, some board directors are planning to push CEO Adam Neumann to step down as chief executive, Bloomberg News reported over the weekend. Sure, WeWork’s bond price has fallen; yet considering all the drama, it’s been fairly firm, oscillating between 95 cents and 105 cents on the dollar. What explains this reserve of faith?

One factor could be a “change of control” clause in WeWork’s prospectus. If it’s triggered, the company will be required to offer to repurchase all outstanding notes at 101% of their principal amount plus accrued and unpaid interest to the purchase date. Imagine the lucrative capital gain: As of Monday morning, WeWork’s 2025 bond was trading at 95.8 cents. Could SoftBank Group Corp., with a 29% stake, take over the troubled company? Founder Masayoshi Son, for one, has lost faith in Neumann’s leadership skills.

So a change of control is on the way, right?

Not so fast. Just like its stock, whose multiple-class voting rights give Neumann disproportionate control, WeWork’s bonds also work against company outsiders. A change of control is triggered when outsiders gain more than 50% of the total voting power of the company; but it’s not just Neumann that investors have to wrangle power from. The insiders, or “permitted holders” in the bond jargon, include WeWork’s earlier investors such as Benchmark Capital and SoftBank Group Corp., to name a few.

In the bond world, the threshold that determines control can be pretty low. Hong Kong-based real estate developer SOCAM Development Ltd., for instance, considers the clause triggered if its key man Vincent Lo “and other permitted holders together own less than 35 percent” of the issuer. Not so at WeWork.

My hunch is that even if Neumann loses his CEO job and is forced to sell some of his voting shares, cash-strapped WeWork will argue against the implementation of this trigger. A change of control would not only force WeWork to exercise a put option on its $669 million bond, but to retire its bank facilities early. As of the end of June, the company had $1 billion of stand-by letters of credit outstanding. As we can see in the prospectus WeWork offered to investors in April 2018:

… under the Bank Facilities, a change of control (as defined therein) constitutes an event of default that permits the lenders to accelerate the maturity of borrowings and other credit extensions under the Bank Facilities and the commitments to lend or otherwise extend credit would terminate.

So when the fight for WeWork’s operating control unfolds in public, institutional investors could find themselves arguing, too. You might say that they should have seen this coming: In a world of negative and zero rates, risky borrowers are in the drivers’ seat.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.