(Bloomberg Opinion) -- Fracking may be America’s most powerful weapon against Russian aggression.

President Joe Biden’s administration was already working to bring down gasoline prices before the crisis and war in Ukraine. Those measures, however, mostly depended on quick fixes such as a suspension of the federal gas tax or an opening of the strategic petroleum reserve. They would do little to relieve the financial hardship of U.S. consumers and nothing to weaken Russia’s geopolitical position.

That’s because they don’t address the fundamental problem: The world’s demand for oil is growing faster than its ability to produce oil. A reduction in the gas tax would have no effect on the supply of oil, and would actually increase the demand for it. Likewise, a release from the strategic petroleum reserve would increase the supply of oil now, but because it doesn’t increase production, the bump would be short-lived.

Fortunately, the U.S. has a technology that would not only increase the total supply of oil, but also keep a lid on prices. What the fracking industry needs is more support from the president and Congress.

A short history of the last decade of the U.S. fracking industry is instructive. When fracking first took off in 2011, the price of oil had broken through $100 a barrel and was expected to keep rising, to perhaps $200 or more. But the rise of fracking arrested that expected price increase and held oil to about $100 for the next three years. In response, OPEC rapidly increased the supply of oil in an attempt to drive down the price and put the U.S. fracking industry out of business.

It didn’t work. Fracking declined at first, but drillers became more efficient until they could be profitable at about $50 a barrel. OPEC and Russia then tried driving the price all the way to down $36 — but at that level, many of OPEC’s member countries, as well as Russia, faced serious financing difficulties.

{kind=link}

{kind=link}

OPEC and Russia then reversed course and cut supply, hoping to bring oil prices back to the level that had prevailed before the price war. But the newly efficient fracking industry was able to rapidly increase supply. The end result was a kind of truce, with oil trading at about $60 until the pandemic.

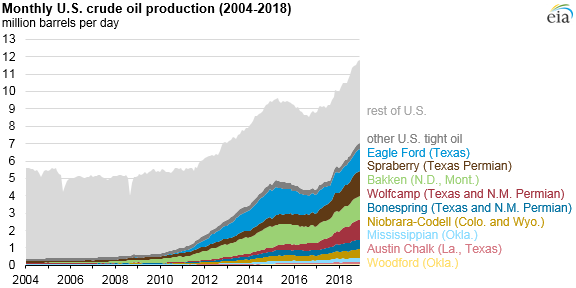

Covid hit the U.S. fracking industry hard, and it has yet to recover. From 2018 to 2020, U.S. oil production grew from almost 10 million barrels a day to almost 13 million. Today, however, oil production is about 11.7 million and rising slowly. As a consequence, the price of oil has steadily risen — filling the coffers of the Russian treasury.

Only Russian President Vladimir Putin can say why his invasion of Ukraine began when it did. It’s worth noting, however, that periods of high oil prices have coincided with periods of Russian aggression. When Russia invaded Crimea in 2014, the price of oil was roughly $100 barrel. It crashed later that year. Oil stayed well below that level until just last month, when it rose above $95.

Higher oil prices strengthen the Russian economy and weaken Western Europe’s. Higher oil prices also hurt America — so long as fracking production stays muted.

To be sure, market forces will cause fracking production to pick up in response to the elevated price. But there are several things the Biden administration can do to speed the process along.

The first is simply to be vocal about the vital role of the fracking industry in national security. Democrats are perceived as actively hostile to the oil and gas industry. That limits the amount of exposure investors are willing to have to U.S. production. If the president himself were to say that energy security is as important as climate security, it might mitigate some of the current hesitancy to invest.

The government should also reopen federal land to fracking. That will allow for some increase, but it will be mostly helpful as a signal to investors that the government supports expanded oil and gas production.

Congress can and should go further, offering to guarantee the debt that drillers incur over the next year if they decide to expand production. That would be a dramatic and controversial step. But it would create an incentive for drillers to move quickly.

Of course, such a measure would not bring oil prices down immediately. Most of the boost would be felt late this year and into the next. Lower oil prices would increase the U.S. and Europe’s ability to endure sanctions while reducing Russia’s ability to fund its war in of Ukraine. And that would help shift the balance of power away from Putin and toward the West.

Related at Bloomberg Opinion:

- The World Has Been Using A Lot More Oil Than We Thought: Julian Lee

- Oil, Gas and Commodities Aren’t Being Weaponized — for Now: Javier Blas

- Biden’s Ukraine Response Is Mired in Barrels of Oil: Liam Denning

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Karl W. Smith is a Bloomberg Opinion columnist. He was formerly vice president for federal policy at the Tax Foundation and assistant professor of economics at the University of North Carolina. He is also co-founder of the economics blog Modeled Behavior.

©2022 Bloomberg L.P.