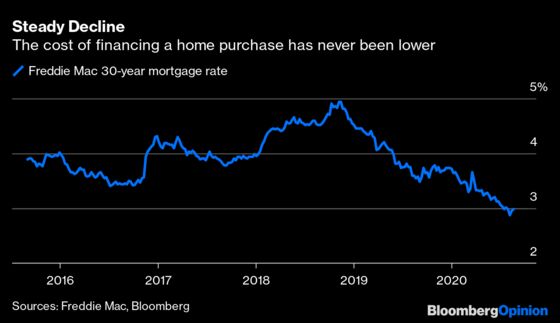

(Bloomberg Opinion) -- With 30-year fixed U.S. mortgage rates dropping to below 3% last week, many have decided it's a good time to buy a house. Existing home sales rose by the most on record in July, while new homes sales jumped to the highest level in almost 14 years.

If you’re now considering buying a home, you need a carefully planned strategy.

The very first step should be to draw up a plan around when you would like to buy, in what location and at what price range. As simplistic as this may sound, not knowing these three things can keep you from saving, or not saving enough, and delay your ability to buy.

Know how much to save. Financial advisors generally recommend saving for 20% or more of a house purchase price as a down payment. The larger your down payment, the smaller the loan you’ll have to take out, the less you’ll pay in interest over the long-term and the more sought after you’ll be as a borrower, with banks competing for your business.

Banks typically lend at more favorable rates and do not require you to buy private mortgage insurance if you put down 20% or more on the property. You don’t have to pay this much up front — there are programs for first-time home buyers that will lend if you can put down even 5%. But the cost of borrowing will usually be higher.

On top of saving for the down payment, you should also make sure to save for closing costs and potential repairs.

Know your financing. For those fortunate enough to have saved up a substantial down payment, financing options have never been better. The 30-year fixed mortgage rate in the U.S. has dipped to the lowest level it has ever been.

Even though mortgage rates are already very low, it still pays to shop around and get quotes from multiple lenders. This is especially true for women and people of color, as research shows lenders tend to unfairly offer them higher mortgage rates.

When you are ready to buy but are still searching for your dream house, consider getting a pre-approval letter from a bank stating the amount of a loan they are willing to extend you. This process is the same as applying for a mortgage, just without the signed purchase contract, and is typically valid for 90 days. It is easier to make offers with a pre-approval letter, as it shows sellers you are serious about buying, and it expedites the closing process.

Consider additional costs. Choosing to buy versus rent should be grounded in a careful comparison of the financial implications of each choice. There are numerous mortgage calculators online that can give you a sense of what your monthly mortgage payment would be based on the home price, loan amount, loan term and interest rate. Some calculators also factor in “approximate” property tax and insurance costs that you’ll be responsible for. On top of these, homeowners also have costs associated with maintenance. More affluent areas may also have homeowners’ association fees.

On the plus side of owning, one of the advantages is the tax break you can get by deducting mortgage interest from your income tax if you itemize your deductions. This is especially true if you are a top earner and your annual mortgage interest is higher than the standard deduction of $12,400 for single filers or $24,800 for those married filing jointly in 2020.

But buying a home also means tying down a big portion of your wealth in an illiquid asset, after depleting your savings to pay for a down payment. And while it’s true that most homes appreciate in price over the long term, the constant maintenance will often mean plowing money into them rather than using them for income.

Location, location, location. Until recently, location was one of the biggest factors determining the price buyers were willing to pay for a home — and being near the workplaces was their number one criterion. For the same reason, houses near major transportation hubs were also highly sought after. As a result of the Covid-19 pandemic, however, people seem to be less concerned about commuting and are instead choosing homes based on the actual structure and whether they are designed for working from home.

But other aspects of where you live are still important, as your zip code determines property taxes you’ll pay, schools and hospitals you’ll have access to and other amenities. We may be moving around less during the pandemic, but being close to highways, train stations and airports will probably become valuable once again.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anora Gaudiano is a senior adviser associate at Wealthspire Advisors. Before joining Wealthspire, she spent more than a decade writing about markets and investing for the Financial Times, MarketWatch and Bankrate.

©2020 Bloomberg L.P.