Wall Street Sets High Stakes for Next Fiscal Stimulus

(Bloomberg Opinion) -- The biggest U.S. banks are done reporting second-quarter earnings, and the message to congressional leadership is clear: Congratulations, you staved off the worst-case scenario from April through June. But now what?

Consider Bank of America Corp., where Chief Executive Officer Brian Moynihan called the past few months “the most tumultuous period since the Great Depression” in a statement on Thursday. While it’s true that profit at the second-largest bank by assets fell 52%, a look under the hood suggests the results could have been far worse. Net charge-offs were effectively unchanged from the first quarter at $1.1 billion, lower than estimates, while those for consumers declined by $138 million. The bank chalked that up to “deferrals and government stimulus.” Similarly to JPMorgan Chase & Co., a large chunk of credit-card holders who requested deferrals from Bank of America ended up making payments each month anyway.

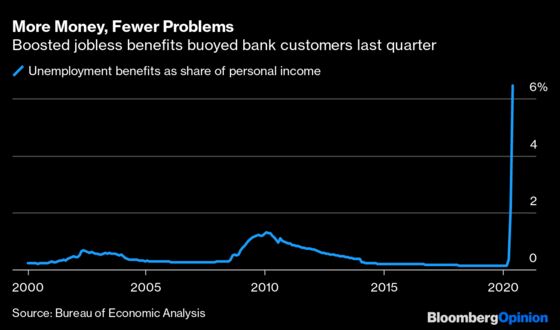

It’s not hard to construct the narrative behind these trends, especially in light of Bank of America ending the quarter with a record $1.7 trillion in deposits. By and large, Americans simply have more money than they thought they would when the coronavirus pandemic and ensuing economic shutdowns began in March. First, there were the one-time $1,200 checks sent to middle and lower income adults in April. But, more crucially, those who lost their jobs have received $600 a week in extra federal unemployment benefits on top of what they get from their state. According to researchers at the University of Chicago, that provides two-thirds of workers who are eligible for unemployment insurance more than what they lost in earnings.

Whether that program, called Federal Pandemic Unemployment Compensation, is extended beyond the end of this month remains in doubt. Democrats want to extend it, while Republicans aim to cap the funds in some way, such as making it so workers don’t receive more than they did at their last job. In June, the Treasury Department sent out more than $100 billion in jobless payments, an unprecedented sum.

“This is not a normal recession. The recessionary part of this you’re going to see down the road,” JPMorgan CEO Jamie Dimon said earlier this week. “You will see the effect of this recession. You’re just not going to see it right away because of all the stimulus.”

Naturally, that raises the question: What if the stimulus doesn’t stop?

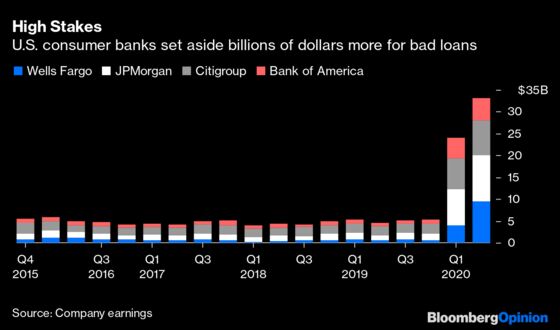

As it stands, Bank of America, JPMorgan, Citigroup Inc. and Wells Fargo & Co. have set aside roughly $33 billion for bad loans, which provides some sense of what’s at stake as Congress debates what its next relief package should look like. For a more micro perspective, Bloomberg News interviewed a handful of jobless Americans on the verge of losing their $600-a-week lifeline. They said they’d have to dip into savings to get by, which could erode deposit growth at big banks.

The thing that makes bank earnings so useful as a macroeconomic indicator is that consumer preferences are largely irrelevant. In industries like retail, travel and entertainment, there are real long-term questions about how Covid-19 will fundamentally change business models. Banks, on the other hand, at a basic level simply move money around to support the economy and seek to collect what they’re owed. That’s obviously a lot easier to do when there’s ample cash in the system.

Interestingly, Paul Donofrio, Bank of America’s chief financial officer, disputed the notion that federal relief programs have made it more difficult to assess the true strains felt by U.S. households. He pointed to the bank’s modest net charge-offs. “If you’re looking for objective evidence that the health of the consumer is pretty good right now even though we’re in the middle of this pandemic, that’s probably the best evidence I can give you.”

The words “right now” do a lot of heavy lifting there. Consider two pieces of crucial economic data released Thursday. First, U.S. retail sales jumped 7.5% in June from a month earlier, topping estimates of a 5% increase. However, Labor Department figures showed initial jobless claims in regular state programs totaled 1.3 million in the week ended July 11, down just 10,000 from the prior period. That’s the smallest improvement since March, with forecasts calling for a steeper drop to 1.25 million initial claims. Put together, Americans continued to open their wallets last month — and Moynihan said consumer spending in early July was above where it was in 2019. But with persistent job losses and the status of federal benefits unclear, it remains to be seen whether that will hold up.

The second quarter could have been catastrophic for banks and the U.S. economy as a whole. Instead, it’s hard not to feel as if a widespread reckoning has been delayed, if not averted entirely. The Federal Reserve certainly lifted the investment banking divisions to blockbuster results and helped large companies acquire funding, but, as Chair Jerome Powell has said repeatedly, it’s a credit to Congress that it acted so swiftly to mitigate the pain of individual Americans.

The spotlight is squarely back on Washington again. How elected officials resolve their standstill will go a long way toward determining whether those tens of billions of dollars of provisions at U.S. banks turn into real losses or simply reflect an economic calamity that never came to pass.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.