With a Debt Pile This Big, It Pays to Think Different

(Bloomberg Opinion) -- Vodafone Group Plc Chief Executive Officer Nick Read certainly doesn’t lack creativity.

Plenty of mobile carriers sell stakes in their cellphone towers operations to reduce debt. Altice Europe NV, Telefonica SA and Telecom Italia SpA have all done it. But Vodafone, in a sense, is doing it twice.

Read outlined the plan on Friday. To begin with, Vodafone and Telefonica are likely to sell a stake in their British towers joint venture, probably to an infrastructure fund. Vodafone’s remaining interest will be housed in a new holding company which will oversee all of its European tower investments. In turn, Read intends to sell a slice of that holding company, or possibly list some of the shares publicly. It could divest further stakes in national tower companies down the line.

It’s an innovative approach to a proven method of debt reduction for telecoms firms. And cutting debt is a priority for Vodafone after its 18.4 billion-euro acquisition of Liberty Global Plc.’s German and Eastern European operations, a deal that could close as soon as next week. After it does, the company’s net debt will hit around 2.9 times Ebitda.

Towers are a pretty straightforward business. They’re essentially the real estate where carriers lease space for their mobile antenna. Typically, those owned by carriers have lower occupancy rates than those held by independent companies, since mobile operators are wary of being beholden to the whims of their competitors. Specialist companies average 1.7 tenants per tower, while those run by operators have about 1.2, according to consultancy Delta Partners. That represents a straightforward opportunity for infrastructure investors to improve profitability.

When infrastructure funds’ enthusiasm for such assets was at its peak a year ago, Altice sold a stake in its French towers at an enterprise value of 18 times Ebitda. On that basis, Vodafone’s towers could be valued at about 16 billion euros, given its stated Ebitda of 900 million euros.

The market has perhaps cooled a little over the past year, but that didn’t stop Read from trying to bolster his assets with the assertion that Vodafone is a “more attractive anchor tenant than the typical sub-investment grade tenants who have sold towers in the past” – surely a dig at the likes of Altice, whose debt has a junk rating at Standard & Poor’s.

Read’s preference for a structured approach instead of a straight sale could help resolve three problems.

Firstly, the debt issue. Recent changes to accounting standards mean there's not a straight line between proceeds from a sale and the reduction in net debt, since leasing costs become a liability. Still, were the division valued at just 10 times Ebitda, it could return Vodafone’s debt levels to the low end of its target range within three years, according to Bloomberg Intelligence analyst Aidan Cheslin (Read aims to complete the process in 2021).

Secondly, it helps to share the cost of the infrastructure investment required for 5G, where more antenna will be needed to provide the required density of coverage, leading to a more efficient use of capital.

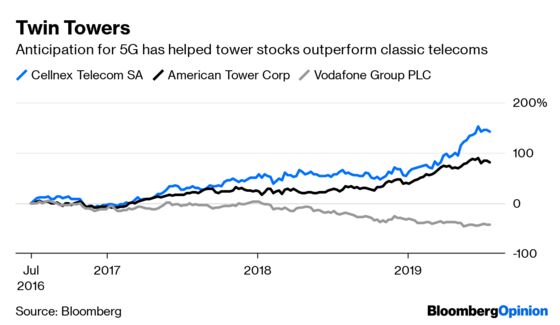

Thirdly, should he opt for an initial public offering of the holding company, Vodafone’s own shares could benefit from any anticipated upside. Investors will have better visibility into the performance of units with predictable long-term returns. Cellnex, currently Europe’s biggest independent towers operator, has climbed almost three fold in the past three years.

Vodafone hurtled into the upper echelons of Europe’s most indebted carriers with the deal for Liberty. Read is moving astutely to ensure that doesn’t remain the case.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2019 Bloomberg L.P.