Virus-Stricken Markets Couldn’t Care Less About Jobs Blowout

(Bloomberg Opinion) -- In ordinary times, February’s U.S jobs data would have been labeled as nothing short of a blowout. Treasury yields would have climbed, with the expectation that the Federal Reserve would leave interest rates alone and let the labor market run hot, reviving dormant inflation.

Needless to say, these are far from normal times.

U.S. payrolls surged by 273,000 in February, easily beating the median estimate in a Bloomberg survey of a 175,000 gain, according to a Labor Department report Friday. The prior month’s 225,000 advance was also revised upward by 48,000, to 273,000. Even the manufacturing sector unexpectedly added jobs. Average hourly earnings rose 3% from a year ago, meeting expectations, and the unemployment rate dipped to 3.5%, matching a 50-year low. Strong across the board.

That didn’t matter to traders in the world’s biggest bond market — their world had long since changed, thanks to the coronavirus. The benchmark 10-year Treasury yield, which was already lower by almost 20 basis points, barely budged at 0.75%. Two-year yields remained below 0.5%, indicating little change in expectations for the Fed to further reduce interest rates at its upcoming meetings. And 30-year Treasuries were barely thrown off from their breathtaking rally that has pushed their yields down to 1.3%.

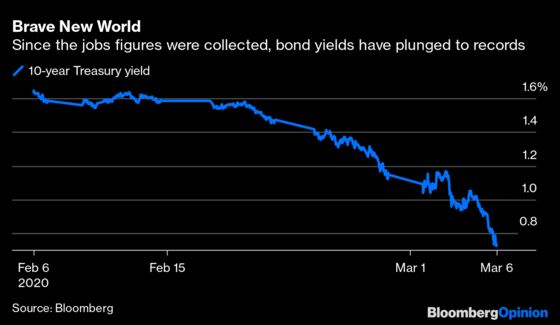

Now, this report was always going to be somewhat inconsequential because the first round of figures only use data though the middle of the month. Here are the specifics from the Labor Department’s website:

CES begins collecting sample reports for a reference month as soon as the reference period — the establishment's pay period that includes the 12th of the month — is complete. Collection time available for first preliminary estimates ranges from 9 to 15 days, depending on the scheduled date for the Employment Situation news release. The Employment Situation is scheduled for the third Friday following the week including the 12th of the prior month, with an exception for January.

Obviously, the world has changed since the week that included Feb. 12. One week after that date, on Feb. 19, the S&P 500 Index set an all-time high. Less than two weeks after that, on March 3, the Fed delivered its first inter-meeting interest-rate cut since 2008 to stem a market collapse, causing the benchmark 10-year Treasury yield to fall below 1% for the first time ever. Now it’s March 6, and the global outlook remains very much in question due to the spreading coronavirus. Wall Street’s stock investors have simply admitted “we don’t know what’s going on.”

Bond traders have long been pessimistic about the outlook for the world economy. Treasury yields fell throughout 2019 even as equity markets hit new highs, with investors widely expecting steady — if unspectacular — growth. A broad swath of the Fed’s primary dealers predicted the 10-year yield would end 2020 in a range of 1.5% to 2.25% after ending the year at about 1.9%. On Feb. 12, it remained comfortably tucked into the lower end of that range, at 1.63%. It’s in uncharted territory now.

It’s doubtful that this jobs figure will change any minds at the Fed. If anything, the central bank’s Beige Book provides slightly more up-to-date information, even if it’s largely “anecdata.” Here were some excerpts that specifically called out the coronavirus:

Boston: “Two firms, in advanced sensors and chemicals, pointed to disruptions related to uncertainty and supply chain challenges from the coronavirus as factors leading to their slower 2020 start. Seven of ten manufacturers did not mention disruptions from the virus to date.”

Atlanta: “Due to the coronavirus, canceled flights to China have reduced air cargo capacity significantly, which is expected to negatively affect first quarter revenues.”

Chicago: “Some manufacturing contacts reported low inventories of inputs produced in China due to disruptions from the coronavirus outbreak; while most said the impact had been minimal so far, many expected a larger effect if the disruptions continued much longer.”

The high-level takeaway: It’s not dire yet, but businesses are concerned.

As for the jobs report, at best, “good numbers from February will stabilize the foundation of the U.S. economy as investors and economists consider the capacity to bounce once the smoke clears from Covid-19,” Jim Vogel at FHN Financial wrote. Chris Rupkey at MUFG Union Bank called the data “nearly perfect” but warned that “this could be the last perfect employment report the market gets for some time.”

Like everything related to the outbreak, markets will only know more as time goes by. As of now, Treasuries are priced for a dire economic scenario that will force the Fed to drop interest rates toward zero. The strong February jobs report apparently didn’t do much to assuage those fears. If bond traders are right in their outlook, this data might have provided a glimpse at the recent top of the U.S. economy.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.