Richard Branson's Virgin Galactic Is a Huge Financial Risk

(Bloomberg Opinion) -- Instead of reaching for the stars, much of the technology industry seems preoccupied nowadays with finding new ways to serve up advertising or to keep eyeballs glued on cellphone screens.

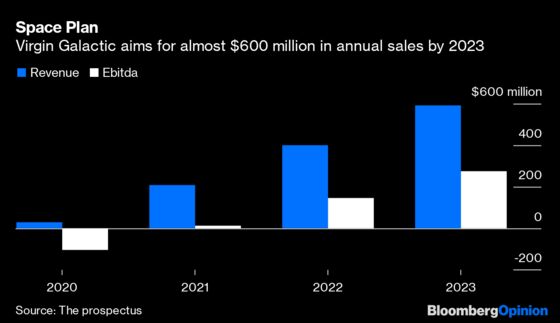

It’s refreshing then that from Monday you’ll be able to buy shares in a company, Virgin Galactic Holdings Inc., whose core business is suborbital space travel. Richard Branson’s pet project will doubtless provide a thrilling service, but as an investment it’s not for the fainthearted. Virgin Galactic expects to be valued at $2.3 billion. Deduct its cash and that’s three times the revenue it might generate in 2023 and 7 times expected Ebitda (a measure of cash earnings). That’s a sky-high price for a business with so much to prove.

Branson and his backers have sunk more than $1 billion into their dream of allowing regular folk to fly beyond the stratosphere. In 15 years they’ve built a spaceport, a launch vehicle and a spaceship; they’ve also completed two crewed test voyages and are on the cusp of starting commercial services. This is all hugely impressive. However, their need for fresh money underscores the capital intensive and risky nature of the space business.

By completing a merger with Social Capital Hedosophia — a so-called “blank check company” (which raises cash to spend on some unspecified deal) — Virgin Galactic has secured more than $450 million in new money. SCH’s backers include hedge funds Och-Ziff Capital Management Group, Arrowgrass Capital Partners and Suvretta Capital Management, according to regulatory filings.

Virgin Galactic will use the cash to build more spaceships. It says the funds will last for at least two years, by which time commercial space flights should have begun. Right now the company isn’t generating much revenue and is burning through cash rapidly. Over the past 30 months its net losses totaled more than $360 million.

The business plan sketches out a smooth path to profitability: By 2023 Virgin aims to have five spacecraft, each carrying at least five passengers and conducting five flights per month. In reality, things could be bumpier. The company still needs final authorization from the Federal Aviation Administration to achieve its aim of starting to transport customers next year. In view of a fatal accident involving Virgin Galactic in 2014, one assumes the FAA will be cautious.

Once paid-for flights start, the commercial pressure will ratchet up. Any technical problems that ground the fleet would shake customer confidence. If Virgin can’t take off, it will have to use more of its cash and might conceivably have to raise more equity, which would dilute investors.

Even if all goes well, Virgin Galactic can’t be sure of the demand for space travel. Few experiences are as exclusive as traveling to space but it’s also the ultimate discretionary purchase. Nobody needs to go there.

It’s reassuring that more than 600 customers have put down a refundable deposit for the 90-minute journey, which entails ascending more than 50 miles above the earth and then floating around weightless for a few minutes. The ride costs $250,000, and Virgin thinks its target customer will probably have at least $10 million in assets (there are about 1.8 million of these people in the world, apparently).

The company expects the cost per ticket to increase somewhat before falling again because of economies of scale and manufacturing improvements. While barriers to entry for competitors are high, Virgin Galactic probably won’t have the space tourism market to itself for long and its potential rivals have deep pockets. Jeff Bezos’s rocket venture Blue Origin LLC also plans to start carrying space tourists and he’s renowned for forcing down prices.

It’s possible Virgin Galactic will use its know-how eventually to try to make money from complementary businesses, including supersonic point-to-point intercontinental aviation. In the near term, though, I suspect real money in the space economy will be made from launching satellites (the “Virgin Orbit” small satellites launch business is not part of the listing). Morgan Stanley analysts value Elon Musk’s Space Exploration Technologies Corp, which carries such payloads into space, at more than $50 billion.

Space tourism is more exciting than transporting lumps of metal and circuitry. It’s also far more risky.

--With assistance from Lara Williams.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2019 Bloomberg L.P.