A Biotech Giant Not Named Biogen Also Had a Good Week

(Bloomberg Opinion) -- Vertex Pharmaceuticals Inc., a nearly $50 billion biotech company that develops treatments for just one rare disease, is having a truly excellent week.

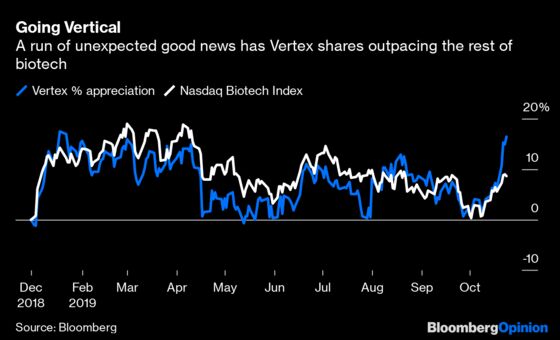

On Monday, the Food and Drug Administration approved Trikafta — a highly effective triple combination of drugs for the chronic pulmonary ailment cystic fibrosis — five months ahead of schedule and just three months after Vertex submitted it to the agency. The approval was expected; the exceptional rapidity of it wasn’t. Then Thursday, Vertex announced that the U.K.’s National Health Service will finally cover all of the company’s treatments, resolving a years-long battle over the price of its drugs. Taken together, the good news helped drive up the shares more than 10%, putting the stock on track for its biggest weekly gain in almost a year.

Had it been another week, these developments might have dominated biotech headlines. Instead, Vertex was overshadowed by Biogen Inc., another $50 billion biotech company whose shares surged after it announced on Tuesday that it planned to file for FDA approval of an Alzheimer’s treatment that had failed earlier. It’s a risky gamble that’s likely to fail, however. Vertex has delivered something far more concrete and confidence-boosting.

Vertex has been working on drugs to treat cystic fibrosis, a potentially deadly disease that causes mucous buildup in the lungs, for more than a decade. It already has a single treatment and two different combinations on the market, but they can’t treat a majority of patients. The company pioneered an unusual strategy to rapidly reach more of the population, testing multiple triple combinations at once to find the best option.

It’s hard to argue with the results. The FDA’s quick green light of Trikafta, which could help 90% of cystic fibrosis sufferers, is a powerful endorsement. The approval gives Vertex a substantial head start on selling a treatment that is expected to generate more than $3 billion in sales by 2023 and should create confidence in the medicine that could translate to further upside.

To live up to its $50 billion market value and a multiple that is nearly 30 times next year’s expected earnings, Vertex has to turn this good news into sustained growth. The U.K. development is particularly promising.

The price of Vertex’s treatments has always been controversial; each of its medicines reaches well into the six-figure range in the U.S.; Trikafta, for instance, will cost more than $300,000. While that’s not unusual in the rare-disease space, the U.K. and some other European countries have balked at the prices, arguing the company’s drugs weren’t cost-effective and refusing to cover them for years despite enormous patient pressure. The standoff escalated to the point where Vertex became a villain in U.K. tabloids and Parliament.

Agreeing to an undisclosed discount with the U.K, which keeps its health system on a strict budget and has an unusually high proportion of the world’s population of people with cystic fibrosis, represents a big step forward for Vertex. The company, which also secured reimbursement in Spain on Monday, seems to have gotten better at making the right concessions. Giving a bit on price to get access to these markets is the right thing to do from both a commercial and humanitarian standpoint. Vertex will see a sales benefit in short order for its existing medicines, and a better relationship with the U.K. will mean even more when Trikafta hits the market, given its much broader utility.

Vertex may have to prove that it isn’t a one-trick pony to justify a further large jump in its valuation, but this run of terrific regulatory and commercial news helps justify its current worth and gives it a longer and more stable runway from which to branch out.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.