Metro Bank Is Paying an Awful Lot Just to Keep Going

(Bloomberg Opinion) -- Metro Bank Plc, the upstart U.K. lender, evidently has little other option than to enter the last-chance saloon. The first company in more than a century to go head-to-head with Britain’s big four banks is struggling to recover from an accounting error (underestimating the risk on some loans) , which led to a sell-off in its shares. Confidence was undermined and its business model has looked under threat.

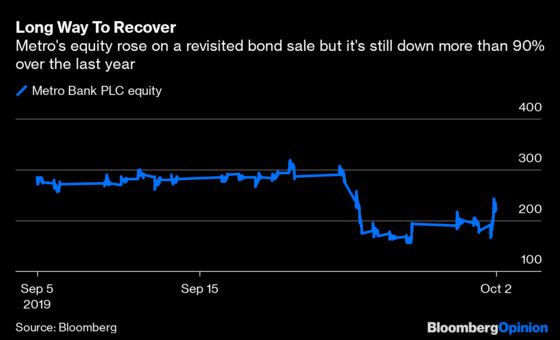

The bank failed to secure investor interest last week for a desperately needed bond issue with a 7.5% coupon, so it came back on Wednesday with a 9.5% offer. That did the trick and the bank even managed to bump up the size of the sale to 350 million pounds ($430 million). It should now have the regulatory capital required to keep functioning, hence the relief rally in its shares.

At this point Metro simply has to prove it has access to funding even if it reduces shareholder value. The more urgent need is to make sure its depositors stay put, especially the more fickle corporate clients.

But that near 10% coupon on its issue of senior non-preferred debt — a new class of bond that can be “bailed in” if the bank fails (the debt-holders bear the losses) — inflicts a heinous blow on its profitability. Barclays Plc analysts have estimated that a one percentage point increase in the cost of 200 million pounds of debt would wipe out 10% in the company’s statutory pretax profit this year.

The interest rate on this bond is way above what other junk-rated banks are paying, even on deeply subordinated debt (the stuff that’s last in line for being paid out). Metro Bank’s issue was a senior bond.

Both its existing bond and its share price rose sharply on the news. But they were already at distressed levels; its previous subordinated 5.5% 2028 bond is still yielding more than 13%.

Investors also reacted well to the departure of the bank’s founder Vernon Hill from the chairmanship and board, even though he’d said before that he’d “probably die” at the company.

While an independent chairman will offer some comfort to investors, Metro may need more management changes. The accounting blunder and its aftermath, which prompted the bank to raise capital in May, prompted questions about the chief executive officer Craig Donaldson.

The bigger fear is that it’s become so much more expensive for Metro to fund growth. It has about 22 billion pounds of assets, but it needs to bulk up to improve profitability at a time when fierce competition and rock bottom interest rates are squeezing profit margins.

Metro is paying dearly just to remain in the game; whether it can stay in it is another thing entirely.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

Elisa Martinuzzi is a Bloomberg Opinion columnist covering finance. She is a former managing editor for European finance at Bloomberg News.

©2019 Bloomberg L.P.