Unilever Must Look Mighty Tasty to Activist Hedge Funds

(Bloomberg Opinion) -- Hey, activist investors! You have a European target hiding in plain sight.

With an underperforming share price and a clear route to creating value, Unilever Plc has all the ingredients for a hedge fund swoop.

The European consumer sector has been a fertile hunting ground for activists, with Dan Loeb’s Third Point taking a stake in Nestle SA in 2017 and more recently, Bluebell Capital Partners’ campaign for change at Danone SA. Although Unilever, which reports second-quarter earnings next week, was briefly the subject of a $143 billion approach from the Kraft Heinz Co. in 2017, it hasn’t attracted an agitator. Yet.

Perhaps, with a market capitalization of 113 billion pounds ($156.5 billion), it’s simply too big. But Elliott Management Corp.’s intervention at pharmaceutical giant GlaxoSmithKline Plc demonstrates that scale is no protection, particularly when there are some obvious invitations to activism.

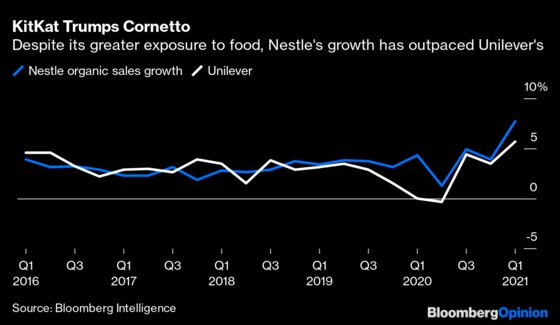

Although the maker of Ben & Jerry’s ice cream and Dove moisturizers had a strong first quarter, it has lagged the growth rate at rival Nestle for the past two years. That’s despite Unilever’s heftier sales to emerging markets — almost 60% compared with just over 40% at Nestle, and two-thirds coming from beauty, personal care and household products. All this should add up to faster expansion than at the world’s biggest food group.

Meantime, Alan Jope, who became chief executive officer of Unilever in January 2019, has made a plethora of acquisitions, from fake meat to fancy laundry products. While buying into trendy sectors — such as vitamins and supplements — should deliver superior sales growth, the danger is that it creates an unwieldy empire. And Unilever still has a big food business — the sleepy cousin of grooming, beauty and over-the-counter medicines.

While Jope has begun tidying up the portfolio, the process has been slow. Early last year, Unilever initiated the separation of its tea business in the developed world, but it’s a complex undertaking and has yet to be completed. It recently began to put some smaller consumer brands, including Timotei shampoo and Impulse body spray, into a separate unit, a possible prelude to a sale.

That’s in stark contrast to Mark Schneider, chief executive of Nestle, who has reshaped the portfolio with a laser-like focus. Bold acquisitions include paying $7 billion for the right to sell Starbucks products in supermarkets — a move which allowed home workers to become their own baristas. He’s also made a string of disposals, including U.S. confectionery, its North American bottled-water brands and its skin health division.

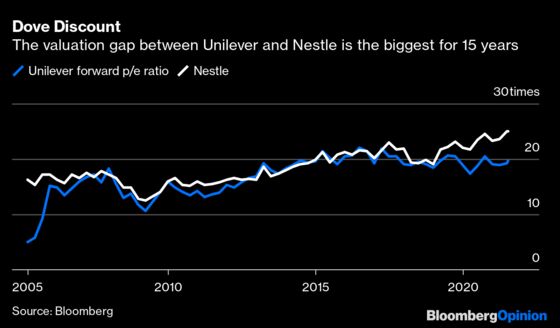

Little wonder that Unilever’s shares have underperformed those of Nestle since Jope arrived. Unilever’s forward price earnings ratio is at its biggest discount to Nestle’s for 15 years. A 3 billion-euro share buy-back announced in April has done little to close the gap.

There is an obvious remedy to this underperformance that’s straight out of the activist playbook: spinning off parts of the conglomerate.

A simple break-up valuation shows there’s merit to this idea, as can be seen from grouping Unilever’s divisions into two broad areas of operation: beauty, consumer and household products; and food and refreshment. Putting the estimated 2021 earnings before interest, taxes, depreciation and amortization (Ebitda) for the first on a forward multiple of 16.5 times — in line with consumer peers — generates an enterprise value of 121 billion euros. Putting food and refreshment Ebitda on 12 times generates 52.5 billion euros. The sum of these two parts is greater than the whole: The enterprise value of all of Unilever is about 155 billion euros.

Selling off the food and refreshment arm to private equity is tantalizing, particularly given the current interest in undervalued staples businesses, as demonstrated by the bid for Wm Morrison Supermarkets Plc. But it would be a huge morsel for buy-out groups to swallow.

More likely is a demerger. That is much easier since Unilever finally combined its separate U.K. and Dutch arms into a single British parent company last year.

There will be costs associated with a split. These include transaction fees as well as the expense of each division having its own corporate infrastructure and product distribution network, particularly in emerging markets. Carving out tea is taking so long because it requires the creation of more than 50 legal entities and over 20 sales forces. There may also be tax implications.

But even if half of the enterprise value unlocked by a separation is swallowed up by expenses, it’s worth exploring. There’s a chance at least some will be offset by greater management focus on what’s left and the possibility of regaining scale through deals.

Of course there’s nothing to stop Jope stealing a march on the hedge fund crowd, and taking an ax to his own empire. The longer the share price performance drifts, the more likely the CEO — or a muscular investor — will pursue a radical restructuring.

Based on the Bloomberg consensus of analysts estimates for 2021 operating profit and assuming that depreciation and amortization and share-based compensation and other non-cash charges are the same as in 2020.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2021 Bloomberg L.P.