Unilever Might Be Better Off Out of the Food Business

Alan Jope needs to take a more radical look at the consumer giant’s portfolio. If not, someone else might do it for him.

(Bloomberg Opinion) -- Unilever NV has made a great deal of “instilling purpose” into its products, trying to flag up the social and environmental credentials of things from Dove shower gel to Magnum ice cream to appeal to millennial consumers. It doesn’t seem to be doing much for its sales.

The Anglo-Dutch company surprised the stock market on Tuesday, warning that revenue growth this year would be below its 3% to 5% range. And it won’t bounce back quickly. Unilever forecasts sales increases will be in the lower half of its target range in 2020, with most progress coming in the second half.

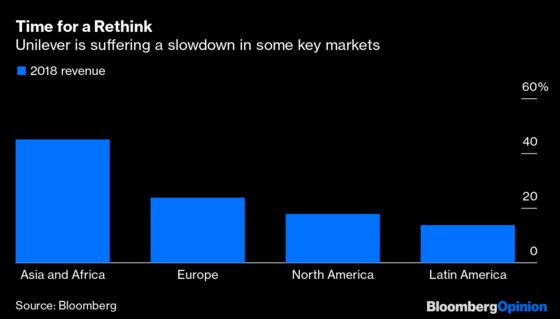

The company said it was suffering from an economic slowdown in south Asia, particularly India, Pakistan and Bangladesh, and difficult trading conditions in west Africa. Meanwhile, its big-selling north American products such as ice cream and hair care are still recovering from a sluggish period, while competition is fierce in parts of Europe.

Yet Unilever must take some of the blame for its own predicament. Its rival Nestle SA has managed steady sales growth, while pulling off some canny acquisitions and disposals.

After a failed takeover approach from Kraft Heinz Co. back in 2017, Unilever set the goal of lifting its operating margin from 16% to 20% by 2020. Alan Jope, the chief executive officer, could have ditched this target when he took the reins at the start of this year to give himself more firepower to invest. But it seems he’s sticking with it: The company said on Tuesday that the goal wouldn’t be affected by the sales slowdown.

While Unilever insists it’s spending enough on research and development and marketing, Jope may have to back his biggest brands with more funds to make sure they’re competitive. That would have to come at the expense of margins.

He also needs to decide in which categories Unilever wants to compete, and reshape its sprawling portfolio accordingly. It’s admirable that the company generates close to 60% of its sales in emerging markets, and operates in popular areas such as beauty and personal care. Unfortunately, it is also over-exposed to more sluggish food ranges such as tea and dressings.

Jope could do worse than learn from Nestle’s CEO Mark Schneider. The latter has been quick to prune unwanted categories, recently selling its U.S. ice cream business to a joint venture between itself and private equity. Nestle has also been buying in its preferred product areas, such as coffee.

Unilever, meanwhile, has been less bold, undertaking a plethora of small acquisitions — from fake meat to fancy laundry products. The group generated only about 0.5 percentage points of growth from its acquisitions and disposals in the first half of the financial year; Jope says he’ll slow the pace of bolt-on deals and step up disposals.

If he doesn’t hurry, someone else might attempt to do some portfolio tidying for him. Kraft Heinz isn’t in a position to make another approach. But an activist investor may be tempted. Selling Unilever’s foods and refreshments business for cash is a possibility, although a demerger might be complicated by Unilever’s dual British and Dutch structure.

The food unit could have an enterprise value of 55 billion euros ($61 billion), according to UBS analysts. So offloading it would generate proceeds to invest in higher growth products, while allowing the return of cash to investors. On a price-to-earnings basis, Nestle’s premium over Unilever is widening. An aggressive investor may spot a corporate purpose of their own.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.