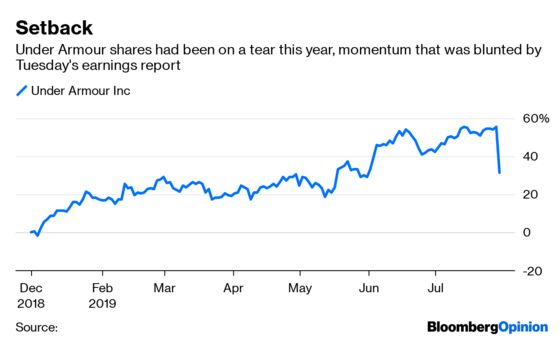

(Bloomberg Opinion) -- Wall Street has rewarded Under Armour Inc. this year, sending its stock up more than 55% through Monday’s close as the company made progress toward putting a bad chapter behind it. Tuesday’s earnings report suggests that investors got ahead of themselves.

The athletic-apparel giant improved on some key measures. In particular, gross margin expanded to 46.5%, in part thanks to initiatives aimed at bolstering its supply chain. And inventory fell 26% to $966 million, a major step toward clearing bloat that had been a serious problem for the company a year ago.

However, the sales picture in its largest market, North America, looks shaky enough that it should temper enthusiasm about those operational improvements. Revenue in Under Armour’s North America division fell 3% from a year earlier in the second quarter. That follows a 3% decline on this metric in the first quarter, meaning it didn’t show sequential progress in this critical area. Perhaps most importantly, the company said it is now expecting a “slight decline” in revenue in North America for the full year, a gloomier view than the “relatively flat” sales it had previously expected.

I warned back in May that investors shouldn’t cheer the Under Armour turnaround story quite so enthusiastically until we saw clearer signs that its North America division, which accounted for 72% of sales in the latest fiscal year, was in a stronger position. Tuesday’s results offered validation of my skepticism. Shares fell nearly 20% in early trading.

During the conference call, executives offered some detail on what caused the soft results in this segment. Its wholesale business declined as it worked to reduce off-price selling; that’s a predictable consequence of a sensible, ongoing effort to restore its brand cachet. But the situation at its own stores and website was more complicated. At its physical stores, conversion – the rate at which visitors go from browsing to buying – was up, but not enough to offset weak foot traffic. On its website, it was the reverse: Traffic was up, but conversion was down. That is a confusing tangle of challenges that won’t be easy to quickly diagnose and resolve. Under Armour is right to try to move away from a constant cascade of discounts, but Tuesday’s results are a reminder that this isn’t easy to do after shoppers have become conditioned to expect them.

I can see several avenues for Under Armour to heal itself in its home market. Executives have said they feel they have a strong pipeline of product innovation for the second half of the year. There is nothing quite as powerful as buzzy, covetable merchandise to invigorate a clothing brand, so if they’re right about the strength of their forthcoming selection, that could make a difference.

Additionally, CEO Kevin Plank noted on Tuesday’s call that while the company’s product-specific marketing efforts have been effective of late, Under Armour has been “fairly quiet” on the brand marketing front. I can easily imagine Under Armour getting a boost from a splashy campaign that casts it as a premium, performance-oriented brand.

I’m reminded here of a consumer brand in a different sector that was in turnaround mode not long ago: Chipotle Mexican Grill Inc. Its CEO, Brian Niccol, noted when he first arrived in 2018 that Chipotle had been “invisible” from a marketing standpoint. Since then, it has unleashed a steady stream of brand ads, reminding people of the restaurant’s focus on premium ingredients, and that has contributed to a serious acceleration in the business.

Under Armour’s progress on operational issues shouldn’t be disregarded. But without a sales revival in its home market, Under Armour falls short of a win.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Sarah Halzack is a Bloomberg Opinion columnist covering the consumer and retail industries. She was previously a national retail reporter for the Washington Post.

©2019 Bloomberg L.P.