The U.S. Unemployment System Is Broken But Fixable

(Bloomberg Opinion) -- Now that Congress is on the cusp of boosting direct payments to $2,000 for all but high-income Americans to help them through the pandemic, lawmakers should focus on shoring up and fixing the system of unemployment insurance.

The goal of unemployment insurance, which was created in 1935 along with Social Security and other safety net programs, was to provide “security against the hazards and vicissitudes of life,” according to then-President Franklin Delano Roosevelt. But current jobless benefits—even with extra weeks of benefits and expanded eligibility in the $2 trillion Cares Act— do not reach all of those that need it the most.

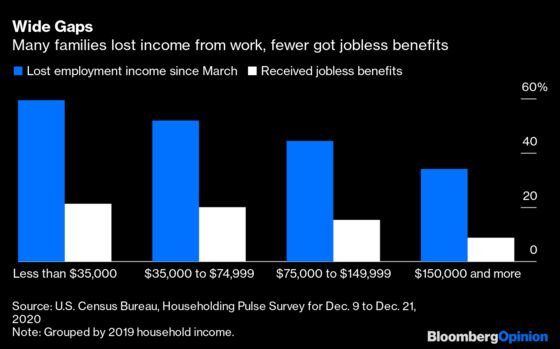

U.S. Census Bureau data show that although almost half of all households have lost income from work since March, only 17% have received jobless benefits. That’s one-third of American families with economic “hazards and vicissitudes” from the Covid-19 crisis who are going without help from unemployment insurance. The gaps are even larger for families with low and moderate income.

The problem is not new. Only four in 10 unemployed workers have, on average, received regular benefits from the program over the past 50 years. In addition, the benefits typically replace only one-third to one-half of wages. Congress often enhances the benefits in recessions, but those efforts are ad hoc and tend to expire well before a recovery takes hold. The world’s richest country should be serving all workers and their families who can’t find work in good times and bad. So how do we reach more of the six in 10 workers who are not getting benefits?

First, make the successes in the Cares Act permanent. The temporary expansion in eligibility—via the Pandemic Unemployment Assistance program—was a godsend to people who do not have traditional, full-time employer-employee work arrangements. In fact, 36% of the 16 million people receiving jobless benefits are getting them via this special program. This includes gig workers, the self-employed, independent contractors and part-time workers who lost income due to the crisis.

Expanding eligibility would also help address longstanding racial inequities in the system. At its start, the unemployment insurance program deliberately excluded categories of workers, such as domestic and agricultural, leaving out many Black workers as a result. While the program did expand to other industries over time, jobs in which minority groups are over-represented, such as part-time or seasonal work, are less likely to be covered than jobs with mostly White workers.

In addition, the $600 increase in weekly benefits from the Cares Act made the insurance stronger. Research from the JPMorgan Chase Institute shows that the policy increased spending for many low-wage workers. When the extra $600 payments expired at the end of July, spending slowed. The latest relief package added back $300 per week but it will expire early in the spring.

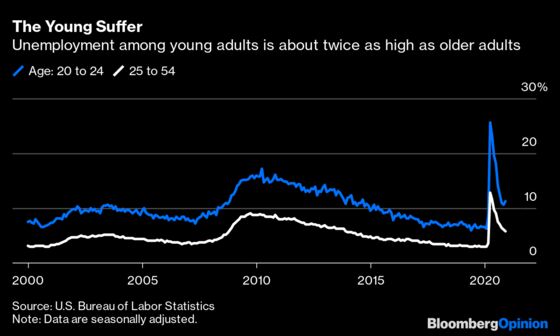

Second, we need a program to support people who do not meet the work history requirements of the regular unemployment insurance system. For example, many young adults who graduate from school and enter the labor market for the first time are not eligible for benefits. That’s a problem because in April, one in four workers ages 20 to 24 were unemployed, and one in 10 are still looking for work. Young workers are twice as likely to be unemployed—in good times and bad—as older workers and yet they are much less likely to receive jobless benefits.

As a solution, policy experts from the Center for American Progress, National Employment Law Project and the Georgetown Center on Poverty and Inequality propose a Jobseekers Allowance. It would provide short-term weekly benefits for people looking for jobs but who don’t quality for unemployment benefits. They estimate that adding a Jobseekers Allowance would mean that three in four workers would be eligible for some benefits, substantially more than unemployment insurance alone.

Finally, Congress must address the huge geographic differences in unemployment insurance. When the system was launched in the 1930s, political concerns about too much power in Washington led to it being administered at the state, not the federal level. In addition, states were given leeway in how to interpret the guidelines of the program. Fast forward to today and big differences in funding, eligibility, generosity and ease of access exist. How well unemployed workers are supported depends on where they live.

Millions of workers are paying for this flaw in the system. When comparing Florida and Massachusetts, only 12% of families have received jobless benefits in the former versus 22% in the latter even though about the same percentage of residents in each state lost employment income.

Within states, systemic gaps in benefits exist. The California Policy Lab, a research center at the University of California, has documented that poor neighborhoods and those where more people of color live are less likely to receive benefits. The unemployment insurance system is failing those most in need and it is piling on the racial discrimination in the labor market.

In response, Congress should set more stringent minimum standards for states and enforce them. Everything from funding levels to administering of benefits needs to be standardized. As its founders intended, states may choose to run more generous programs and experiment with improvements, but every state must meet the national standards, and those standards must be sufficient to support the unemployed and their families though temporary jobless spells. No more letting geography determine generosity.

We must do better, or we will pay for it as a country in stunted careers and lost dreams for years. President Joe Biden and Congress must guarantee relief to the unemployed now and in the future.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Claudia Sahm is a former Federal Reserve economist and creator of the Sahm rule, a recession indicator.

©2021 Bloomberg L.P.