America’s Bonds Are Caught in a European Tractor Beam

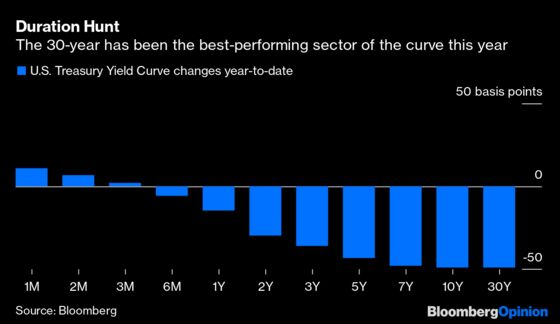

(Bloomberg Opinion) -- The yield on a 30-year U.S Treasury bond has finally fallen to a record low of 1.83%, having dropped a staggering 50 basis points this year already. With the coronavirus outbreak forcing people to look for havens, there are few signs that this investor frenzy for long-maturity sovereign debt is going to abate anytime soon.

The U.S. appears to be headed at breakneck speed toward the same incredibly low interest-rate return environment as Europe and Japan. If the trend continues, U.S. benchmark yields might end up flirting with zero — especially if the coronavirus becomes a pandemic and trashes global growth. There’s the added dimension of the democratic nomination race being led by the hard-left Bernie Sanders.

Leaving politics and health emergencies aside, U.S. yields are a bargain anyway when compared to the world’s other major bond markets. The dollar’s unrelenting strength makes the country’s debt even more compelling.

Renewed quantitative easing by the European Central Bank is clearly a major factor in pushing the world’s bond investors to hunt elsewhere for yield — and, as my colleague Ferdinando Giugliano points out, the coronavirus outbreak in Italy will put the pressure on the ECB to go even further.

Core European sovereign yields are falling further into negative territory, and credit spreads on euro-denominated corporate bonds are tightening rapidly too. Beyond Europe, 10-year Japanese government yields have also turned negative again. The meager pickings everywhere else means there’s a material incentive for fixed-income investors to be overweight in U.S. Debt.

At the same time, Jay Powell’s Federal Reserve is clearly ready with stimulus as needed, as shown by its rapid pumping of “non-QE” temporary collateral into the repurchase markets in September. In a presidential election year, the Fed would doubtless prefer to pause, but the U.S. yield curve is pricing in another rate cut; bond buyers have a strong belief that rates are much more likely to be cut than raised.

There is no compelling domestic U.S. macro reason for the downward pressure on yields. As evidenced by the record high in U.S. equities, the American economy is pretty strong — certainly when compared to Europe or Japan. Annual consumer inflation is at 2.5%, and there’s hardly a shortage of U.S. Treasuries for sale as the deficit balloons.

This is largely about a global flight to quality, magnified by coronavirus fears. The herd instinct is then intensified by index trackers and exchange-traded funds tripping over themselves to add longer term debt too. The two-year to 30-year yield curve (the difference between rates on short-term debt and long-term debt) has flattened by more than 20 basis points this year.

Bond funds are increasingly adopting a two-pronged policy: First, adding maximum duration in government bonds to benefit from the highest possible yield; second, they are buying more corporate credit in short-to-medium maturities. This year has set another record so far for fixed-income sales. It has become something of a self-perpetuating spiral.

Until central banks are able to wean themselves off QE and negative to zero-bound rates, it’s hard to see any meaningful reversal of the multi-decade trend lower in yields. The Fed tried to break free with a march higher on interest rates and quantitative tightening. As both policies have reversed decisively, the tractor beam of European and Japanese-style rates has locked on.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.