U.S. Data Is Beating Forecasts. Hold the Applause.

(Bloomberg Opinion) -- A closely followed gauge that has abruptly signaled that U.S. economic data is consistently exceeding expectations might be the statistical equivalent of fool’s gold.

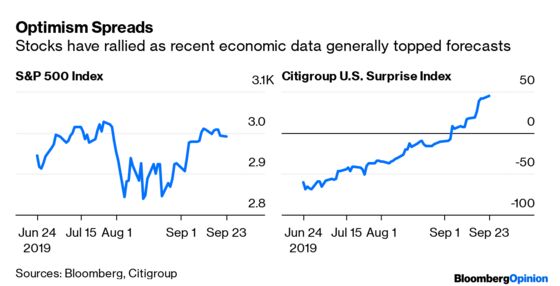

U.S. stocks have rebounded, with the S&P 500 Index gaining about 5% since late August, built on the notion that the economy isn’t doing as poorly as Treasury yields suggested. Indeed, more than a few market participants said bonds were priced for a depression, let alone a recession. Then economic data suddenly started to affirm that things weren’t so bad. Falling mortgage rates have bolstered the housing market. Consumer spending has been resilient. And data on factory orders for July and industrial production in August beat expectations.

These and other reports have propelled the Citigroup U.S. Economic Surprise Index to a reading of 41.70, the highest since April 2018. As recently as early July, it was below negative 60, flirting with some of its lowest levels since the Great Recession. A positive number means the recent economic data has exceeded forecasts in the aggregate.

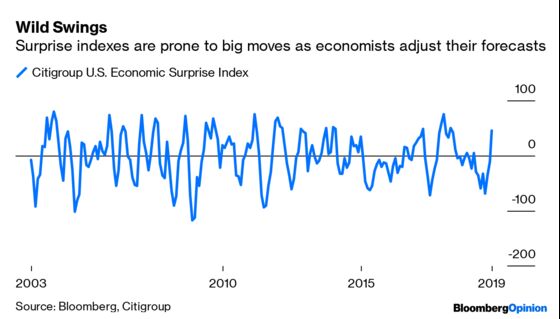

Before concluding that the economy is performing much better than many expected, however, it helps to have a little context. It’s one thing for the Citigroup index to be above zero when the economy is booming and quite another when it is slowing, like now. All it means is that the data is generally topping lowered estimates rather than exceeding raised forecasts. In other words, the bar is lower. That helps explain why surprise indexes have a history of wild swings, marked by big, rapid shifts between positive and negative readings. In short, such gauges are best at influencing market sentiment but less useful in forecasting economic direction.

A prime example might be the end of 2013 and start of 2014, when the Citigroup index shot up from reading of below zero to above 70 over 10 weeks. The economy ended up contracting 1.1% in the first quarter of 2014. Or consider early 2015, when the index went from about 40 to negative 70 by the end of March, yet the economy ended up expanding 3.2% in the first quarter and 3% in the second. The index did track a stronger economy as it rebounded from about negative 80 in mid-2017 to positive 80 at the end of that year. But it failed to anticipate the slowdown that was to come.

In all fairness, accurately forecasting the economy has humbled even the brightest minds on Wall Street. With a seemingly infinite amount of variables, it’s difficult enough to say with any degree of accuracy what is happening at any given moment, let alone months or quarters or in the future. This time last year, the median estimate of 69 economists surveyed by Bloomberg News was for gross domestic product to expand 2.8% in 2018; it came in at 2.5%.

And there are plenty of reasons for caution. Besides the trade war between the U.S. and China, some of those include the rising tensions in the Middle East after an attack wiped out about half of Saudi Arabia’s oil output capacity, the potential for the U.K. to crash out of the European Union without a deal, protests in the Asian financial hub of Hong Kong and the rapidly deteriorating euro zone economy. And for those who think the U.S. economy is big and strong enough to withstand what else is going on around the world, consider that rising globalization means that by Morgan Stanley’s estimates, the U.S.’s share of global gross domestic product has shrunk from 22% in 1990 to 15% today.

The crucial takeaway is that surprise indexes probably say more about how economists have adjusted their estimates and less about where the economy may be headed.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.