Boris Johnson Is the Financial Market's Best Friend

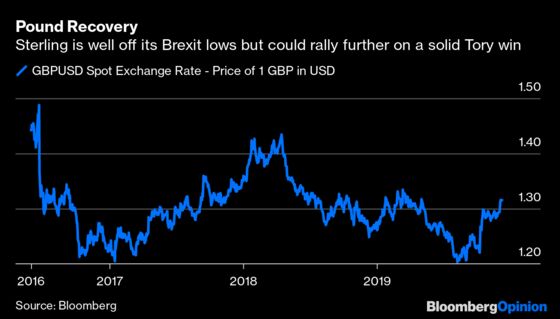

(Bloomberg Opinion) -- Sterling has risen 9% against the dollar since August on hopes of a Boris Johnson victory in Thursday’s general election. The larger the parliamentary majority for the Conservatives, the more the pound should rise. Anything less than a decisive Tory win is unlikely to strengthen the currency.

The pound is cheap relative to other currencies because of the protracted wrangling over Brexit; there ought to be reward for some promise of certainty even if a Johnson victory wouldn’t be a surprise (and even if the markets would then move on to wringing their hands about trade deal negotiations with the European Union). With a solid Conservative win, the pound could exceed its recent March peak of $1.338, although the post-referendum high of $1.43 looks ambitious.

Indeed, there are plenty of reasons to not get carried away — including a tightening in the polls this week. While a Tory majority should encourage the return of some foreign direct investment, the British economy isn’t as strong as it was after the 2016 referendum, when the pound fell sharply. Relying on a big post-Brexit bounce is for the optimists.

Beyond the pound, U.K. government bonds (gilts) have held up well since 2016, following global yields lower — and acting as a haven for those worried about the impact of Brexit on U.K. stocks. Johnson’s big spending plans would need more bond issuance, but this should only cause a modest uplift in yields if spread over several years.

Equities should gain from a more shareholder-friendly Conservative government. Nonetheless much will depend on that EU trade deal, while a stronger pound would adversely effect the plentiful foreign earnings of blue chip FTSE 100 companies.

A failure by Johnson to secure a majority (an outcome that’s entirely plausible) would see the recent sterling gains evaporate, first because it would mean a prolongation of Brexit uncertainty and second because it might see the hard-left Labour leader Jeremy Corbyn sitting in Downing Street.

To govern, Corbyn would almost certainly need propping up by the Scottish National Party and the more moderate Liberal Democrats, weakening his ability to enact the most economically radical manifesto in recent British history. If he had a free hand, you’d be looking at dollar parity. Gilt yields would soar as Labour’s lavish spending would cost many multiples more than the Tories’ already expansionary fiscal plans. Even so, with inflation subdued and global bond yields on the floor, there’s a lot of room before debt sustainability becomes an issue.

Equity investors will be hoping for a Tory victory or some kind of coalition around Labour to soften its pledge to nationalize utility companies, probably without full compensation to shareholders. A Labour-SNP-Lib Dem coalition would also offer the prospect of a second referendum on Brexit, something that might support the pound.

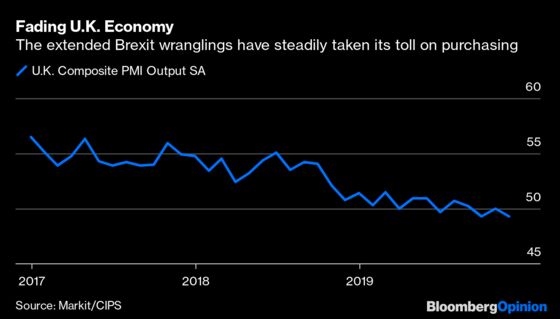

Whomever takes power this week (or later if it’s a hung parliament) will have to balance all of their promises to the electorate with an ugly economic backdrop. The composite purchasing managers survey has fallen steadily from the high-50s in 2017 to below the 50 line; this weakness hasn’t shown up fully in gross domestic product but the sentiment is evident. The Bank of England's next move could be cutting rates before any promised fiscal splurge kicks in.

A Tory win still looks the most market-friendly outcome — even with the prospect of a hardish Brexit. A healthy Johnson majority would let him pass an EU withdrawal bill before Christmas and formally exit on Jan. 31. That should defuse the hard-line Brexiters in his party, perhaps letting him negotiate a more sensible EU trade deal. A return of investment and consumer confidence would soften the impact of the slowing global economy.

Understandably there’s skepticism on whether the trade deal could be completed by the Dec. 2020 deadline, but a modest extension shouldn’t be an impediment. A clear Tory majority would at least change the narrative of the past three years.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.