(Bloomberg Opinion) -- Robert Stheeman has been at the helm of the U.K. Treasury’s Debt Management Office since 2003, overseeing sales of more than 2 trillion pounds ($2.6 trillion) of Gilts, as Britain’s sovereign bonds are known.

He’s the government’s agent in the debt marketplace, the link that smooths communication between the finance ministry and its 15 primary “market-makers” (the big banks from Barclays Plc to Morgan Stanley that underwrite Gilt auctions). His job is to keep the U.K.’s costs to a minimum and make the sale process seamless. The skill is in matching the government’s fund-raising needs with investor demand across the various Gilt maturities. Knighted in 2016 for services to debt management, he is one of Britain’s unsung treasures.

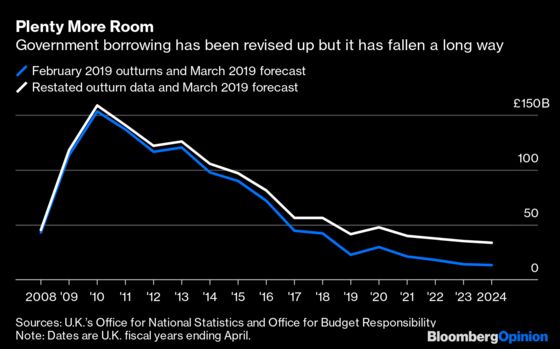

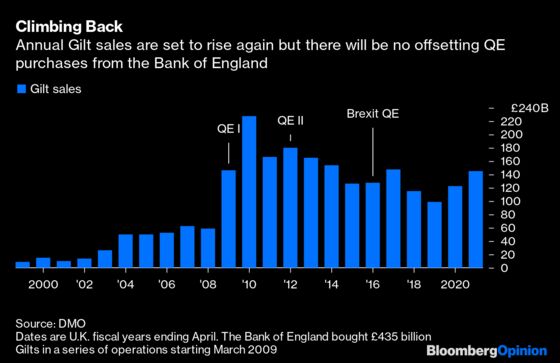

His reputation will certainly be tested over the next few years. Stheeman will have to oversee a big ramping up of Gilt issuance as Boris Johnson’s newly-elected Conservative government makes good on its spending promises. Because of the snap election, there is no clarity yet on financing plans for the next fiscal year. But debt sales will probably rise well above 150 billion pounds (more than half of this from refinancing maturing bonds), compared to 2019’s 123 billion pounds. There has been little reaction in Gilt yields to this prospect, suggesting the DMO is coping.

Helpfully, Stheeman has managed issuance spikes before: During the financial crisis Gilt sales ballooned to pay for the banking bailout. The Bank of England was, of course, on hand to hoover up sovereign paper in its Quantitative Easing program, but this was in the secondary market, never straight from the Treasury. Juggling primary government sales with central bank purchases took skillful coordination.

Britain’s saving grace in the crisis was having an average duration of debt in excess of 14 years, much longer than its global peers. This bought the country more time as there were no huge redemptions of maturing bonds needing to be rolled over. Government financing was never disrupted; although there was a failed long Gilt auction in March 2009, it was just a blip.

The longer age profile of Gilts as a whole also helped persuade the bond markets that U.K. notes weren’t as risky as many other sovereigns. As a result, when investors were only buying shorter-term stuff during the crisis, Britain took it in its stride. The value of shorter maturity Gilt sales (of three to seven years) rose six times between 2008 to 2009 to 58 billion pounds, more than doubling the percentage share of total supply from this type of debt to 43%.

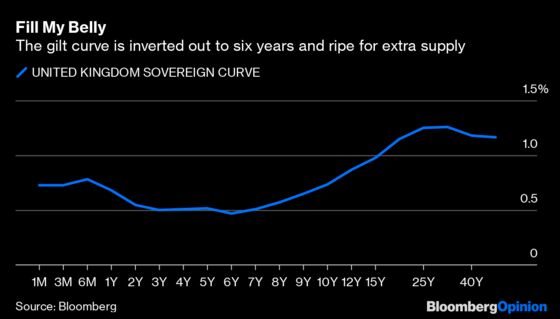

This time around there is no crisis, but there’s still lots of demand for shorter-term paper — pushing down the price of issuance for the Treasury to pay for all those Tory spending and infrastructure promises. The gilt yield curve is inverse from six months to six years (meaning yields are higher on six-month bonds than they are on all subsequent maturities out to six years), which shows there’s strong appetite in the so-called belly of the curve (see chart below). Overseas investors, who have been underweight U.K securities during the Brexit turmoil, tend to prefer maturities up to 10 years too.

The gilt curve inverts again much further out between 30 years and 50 years, driven by demand for ultra-long assets to match pension and insurance liabilities. But the real sweet spot for sales is more in 20- to 30-year paper to cover final salary pension funds. The U.K. was ahead of the game by issuing 50-years as far back as 2005, near the beginning of Stheeman’s tenure. A consultation back in 2012 on issuing perpetuals and ever-longer debt found insufficient demand beyond 55 years. The DMO holds quarterly consultations to monitor any changes, but instead of reaching for 100-years it sees more interest in back-filling the gaps between 15 and 45 years.

Stheeman’s team has maintained the U.K.’s position as the most liquid and efficient of Europe’s bond markets. If you don’t hear his name over the next few years, he’ll be doing his job.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.