Boris Johnson's Six-Month Covid Plan Carries a Heavy Cost

(Bloomberg Opinion) -- Britain’s new lockdown measures may be in place until late March 2021, according to Prime Minister Boris Johnson. That makes one thing clear: It’s too early to withdraw fiscal support from the U.K. economy. That will pain many of Johnson’s fellow Conservatives, who understandably fear creating a culture of financial dependency. But the damage from a major economic downturn, or a chronic loss of confidence in the government, would be far worse.

The pandemic has hit Britain harder — in terms of deaths and economic loss — than any other European nation, but there have been reasons for optimism too. Growth fell less than many expected at the height of the full lockdown in the spring and recovered faster than many dared hope over the summer. Consumers shifted their spending online but still made purchases. Many businesses adapted. My local restaurant began selling fresh fish and produce when it couldn’t serve cooked meals.

And yet, it’s important not to get carried away by the successes. As Michael Saunders, a member of the Bank of England’s Monetary Policy Committee, noted earlier this month, the recent rebound reflected a confluence of several factors: namely, massive fiscal support (equal to roughly 9% of annual gross domestic product) coinciding with a loosening of lockdown measures and greatly reduced rates of infection.

The happier days of summer are over. Covid cases are spiking again and tougher lockdown rules are being reintroduced, including curfews on pubs and restaurants and telling people to work from home where possible.

Johnson’s manifest failure to deliver a working system for mass testing and contact tracing in time for the reopening of schools and other parts of the economy made these restrictions inevitable. The new rules are nowhere near as draconian as those in March, but they’ll have an impact on consumer sentiment and the “lunchtime economy” of London and other cities and large towns.

It’s crucial not to compound the testing fiasco by withdrawing the biggest factor in Britain’s better-than-expected recent performance: the very visible hand of the state.

Of all the claims made by Johnson’s government to preside over “world-beating” coronavirus measures, the one that isn’t risible is Chancellor of the Exchequer Rishi Sunak’s furlough program. It has supported 9.6 million jobs, saved untold businesses from collapse and prevented the economy from suffering a much deeper slump. The support (initially paying 80% of people’s wages) was tapered in July and is due to be withdrawn at the end of October.

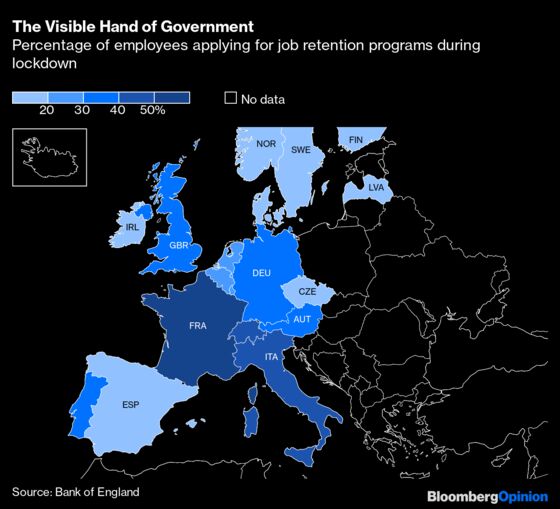

So generous a program naturally raises concerns. The 52 billion-pound ($66 billion) cost is eye-watering and the debt will have to be paid down eventually, even if the current cost of capital is cheap. Continued for too long, such schemes can create a dependency mindset and interfere with market competition. France and Germany have extended their furlough programs long into the future, but Britain doesn’t usually model its economic interventions on continental spending.

Nevertheless, while the furlough program can’t continue forever, nobody’s seriously arguing it should. Most furloughed workers have returned to their jobs, but those still using the system tend to be in sectors that are hardest hit, such as hospitality, suggesting support now can be more targeted. The question Sunak hasn’t answered is why ending it now makes sense, just as the increase in infections is threatening more economic harm and Health Secretary Matt Hancock admits the “cavalry” of a vaccine or mass testing is nowhere in sight.

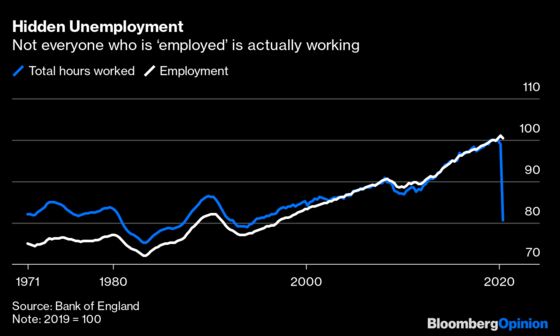

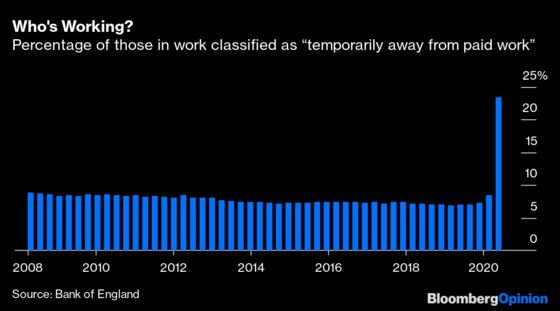

Johnson promised this week that the government will be “creative” in supporting businesses and workers. It will need to be. As BOE Governor Andrew Bailey noted Tuesday, the underlying rate of unemployment is probably much higher than the official 4.1% figure.

The number of companies that have filed notifications of anticipated redundancies and other indicators of a weak labor market, despite the government’s help, suggests a spike is coming as fiscal support is withdrawn. How much is a matter of disagreement. The U.K.’s independent Office for Budget Responsibility estimates that unemployment could hit nearly 12% by the end of the year; the Bank of England’s August estimate is a more optimistic 7.5%. Either way, this is territory not seen since the financial crisis.

Given the fall in business investment, it doesn’t seem realistic to expect many of the newly redundant to find new jobs immediately. Much of the hidden unemployment is in sectors still dependent on the furlough scheme.

Many of these workers may become long-term unemployed, with the physical and mental toll that creates. Some will be unable to afford housing, almost certainly contributing to Britain’s high rate of homelessness. The costs to society, and the taxpayer, of trying to restore normal levels of employment will be enormous.

You can understand Tory fears about propping up zombie companies. Some industries, such as brick-and-mortar retail, face structural declines and some jobs aren’t coming back. But which ones? It’s not easy for anyone to say right now. Tailoring relief for where it’s most needed during the new six-month restrictions would avoid a cliff edge at the end of October.

Over time, it’s right that the government gradually shifts its financial support to retraining. That’s already happening with the 2 billion-pound Kickstart program to help young people, the age group that has suffered worst economically during lockdown.

Sunak’s Treasury looks set to extend its business-loan support scheme, which suggests it has already accepted the need to keep the money taps on. There’s too much uncertainty and virus-dictated disruption to expect companies or workers to cope alone. Let’s hope the Chancellor and his cabinet colleagues are persuaded on furloughing, too.

For a government that’s hemorrhaging credibility by the day, Johnson’s U-turn in guidance from a month ago will only further damage business and consumer confidence. The last thing he needs now is to change the one policy that has really delivered.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Therese Raphael is a columnist for Bloomberg Opinion. She was editorial page editor of the Wall Street Journal Europe.

©2020 Bloomberg L.P.