(Bloomberg Opinion) -- In polite British company, there are certain subjects that are to be avoided: politics (especially Brexit), religion and house prices being chief among them. Hence, these are inevitably where the less mannerly discourse ends up.

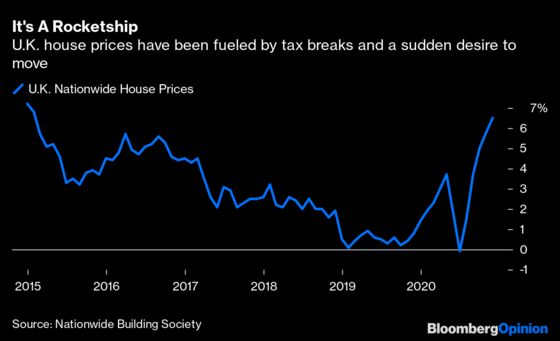

For those lucky enough to own their own home, house prices are up 6.5% this year, according to the Nationwide Building Society survey. It is the biggest annual gain since early 2015 and the strongest quarterly gain in over a decade. Mortgage approvals are also at their highest since 2007. It’s almost as if homebuyers don’t realize the U.K. has suffered its worst economic drop in over 300 years, resulting in 2.5 million deferrals of mortgage payments.

Of course, there are other things going on. Covid has fueled a desire to relocate out of crowded cities, and after five seemingly endless years of bickering, a conclusion to Brexit (of sorts) is within sight. Pent-up demand, combined with a naked rush to cash in on a tax break window, has been enough to drive a mini housing boom.

The time-honored question is: Will the boom last? I think it just might. It seems more than likely that a vaccine will drive up economic growth next year by 6% or more, according to Bloomberg Senior U.K. Economist Dan Hanson, with it projected to pick up notably in the spring.

The British also have a fascination with owning bricks and mortar. Britain is an overcrowded island with limited property supply and lots of demand. Because of some seriously arcane planning laws, it is trickier to build a home here than in other countries, which is why so many focus on improvements and extensions instead.

Although nearly 200,000 homes were built in England in 2019, that was still below the level seen before the global financial crisis. Building this year is likely to be significantly lower. On top of that, sporadic government programs designed to boost homeownership keep demand high. So housing just continues to become ever more expensive. And it’s bigger homes in the country (where they are more likely to be detached) that are rising in price fastest.

The Bank of England also seems determined to send mixed signals. Its monetary policy committee has just increased QE bond-buying by 150 billion pounds ($200 billion) and is even contemplating taking interest rates negative in order to pump-prime the economic recovery. But until this QE is turned into actual new lending, all it does is drive up prices on existing assets.

Yet this lending isn’t really happening. The BOE’s other arm, the Prudential Regulation Authority, is enforcing rules on mortgage lenders to avoid underwriting risk loans during an economic crisis. So those who want to take advantage of the temporary relief from the housing-purchase tax are either being rejected, held up in a long administrative queue or forced to pay higher interest rates.

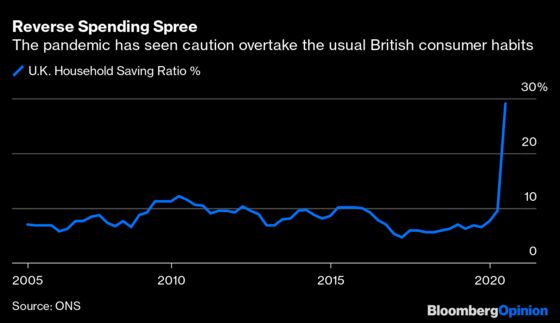

This confusing message is causing a lot of frustration, but it’s doing little to stop demand from pension-minded buyers looking for reliable income in a super-low-yield savings environment, or from foreign buyers looking to capture cheap sterling assets before a Brexit resolution. The savings rate has also jumped during the crisis, so those fortunate enough to have kept their jobs and cut expenses have been able to funnel that cash into property. As unemployment widens, inequality can only get worse.

It is not as if we haven’t seen this kind of boom before. London house prices soared during the depths of the financial crisis as QE stimulus kicked in. When there’s so much economic uncertainty and money is this cheap, there is reassurance in a real asset that can improve your quality of life. So until the landscape changes, we’re going to keep seeing house prices tick up. And don't rule out the chancellor extending that tax relief window. Since when has government liked a falling housing market?

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.