(Bloomberg Opinion) -- Brexit has had little noticeable impact on the market for U.K. government bonds, commonly known as gilts. Up until now all of the political risk has been expressed in the value of sterling.

But with a general election underway, and some monster spending commitments being bandied about by the Conservative and Labour parties, the spotlight will turn naturally to Britain’s cost of borrowing. The gilt market certainly isn’t pricing in the prospect of a victory for Labour’s hard-left leader Jeremy Corbyn. So it might seem fair enough that one of the world's biggest bond funds, Pacific Investment Management Co., is expressing a negative view; warning in the FT that the inevitable fiscal splurge will push gilt issuance higher and yields along with it.

Unfortunately Pimco is sounding like a broken record on U.K. sovereign debt. The fund expressed similar misgivings in April and November 2017, as well as March and September 2018, and is yet to be proved right. We get it: Pimco doesn't like gilts, has been underweight forever and will no doubt remain so.

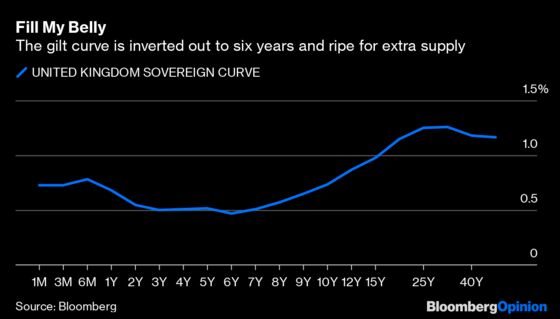

But on a relative basis to most major bond markets, gilts don’t look expensive. At least they yield something (about three-quarters of a percent on 10-year notes) at a time when there’s more than $12.5 trillion of negative-yielding debt in the world.

In fairness to Pimco, it seems certain that gilt issuance will rise as either a Tory or Labour-led government turn on the money taps. Indeed, expectations of an increase of between 20 billion pounds ($26 billion) to 30 billion pounds are already baked into the price after substantial funding commitments on health, education and the police from the current Tory government.

Chancellor of the Exchequer Sajid Javid signaled on Thursday that a Conservative administration would loosen fiscal rules from a current budget deficit cap of 2% of gross domestic product to a maximum of 3% in order to fund extra infrastructure and state spending. Much of the money to pay for all of this will be raised via gilts.

John McDonnell, Labour’s shadow chancellor, has even greater ambitions that might involve another 150 billion pounds of spending above and beyond his already lavish plans for the next five years. That would scare the gilt market more if there was a realistic chance of Labour securing power by itself. But unless the electoral polling changes drastically there’s a much greater likelihood of either a Conservative win or some form of Labour-led coalition with other parties, which would check its more outlandish spending plans.

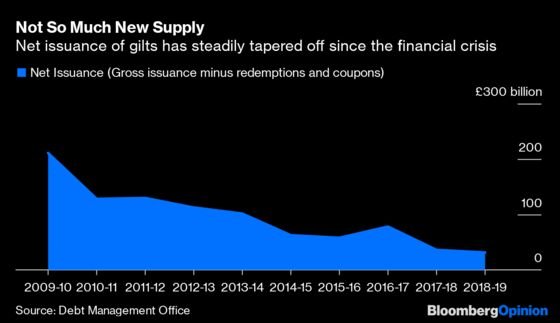

It’s not as if the the extra gilt issuance would be a huge stretch. The Bank of England has hoovered up 435 billion pounds of sovereign paper over the past decade as part of its quantitative easing program. An extra 30 billion pounds to 60 billion pounds of gilts annually (which would cover most eventualities) could probably be absorbed without a major shift higher in yields. Admittedly, an outright Labour victory would test this thesis.

As always with government bonds, though, it’s often about relative value. With U.S. Treasury issuance also increasing rapidly, the extra gilt supply may not stand out that much. That will be doubly true if the European Central Bank’s new president Christine Lagarde persuades euro zone governments such as Germany to boost fiscal spending.

Gilt investors know a lot more supply is coming down the track. That will be well-received if the politics remain relatively normal.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.