(Bloomberg Opinion) -- Thursday's Monetary Policy Committee meeting of the Central Bank of Turkey will almost certainly deliver a reduction from the current 24% policy rate. The initial question is just quite how big. But the real question is: can the lira cope?

The Bloomberg survey consensus is for a 225 basis point cut, but the range varies from just 50 basis points to a whopping 800 basis points. Anything can happen.

This isn’t just any policy decision. President Recep Tayyip Erdogan has long complained that interest rates need to fall quickly in order to contain inflation (an unusual view, to say the least). His sudden replacement of central bank Governor Murat Cetinkaya with his deputy, Murat Uysal, on July 6 seemed to mark the end of central bank independence.

The lira’s performance throughout this drama has also been unusual. It has, against every expectation, been the best performer of all currencies versus the U.S. dollar over the last six weeks, gaining about 8%. It helps that tight money market restrictions have reduced volumes to a trickle, and that the Federal Reserve is about to enter into an easing cycle, something that tends to give an outsize benefit to emerging markets.

The currency still has room to express concern about the country’s political and economic direction, and this week’s central bank decision will test this. The MPC announcement may show whether policy makers have succumbed to severe political pressure, set aside their better judgment on what the Turkish economy actually needs and made a significant reduction in interest rates.

Fortunately, Turkey probably needs rate cuts. The economy expanded 1.27% in the first quarter, boosted by government spending. Though this is the technical end of the country’s recession, second-quarter growth is not expected to be as strong. A little extra help wouldn’t go amiss.

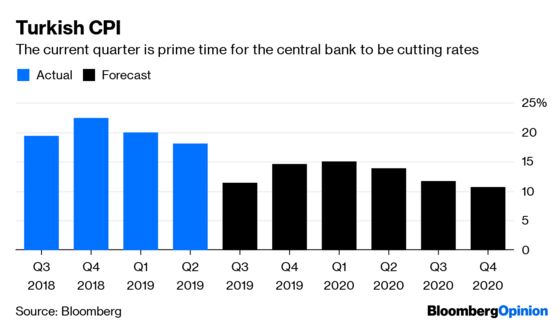

And price gains are heading in the right direction, if policy easing is what’s wanted. Erdogan clearly does. Inflation peaked at more than 25% in October, and cooled to 15.7% in June. Forecasts are for it to fall further over the third quarter due to favorable comparisons to last year. However, upward inflation pressure is likely to resume before the end of the year, so the easing window is short.

It’s hard to read Uysal’s thinking. He has said there is “room for maneuver...as long as there remains a reasonable rate of return,” and from one perspective that’s true. Turkey’s real rate – the difference between the inflation rate and the central bank benchmark – is more than 800 basis points, one of the highest in emerging markets. The question is what is reasonable. Erdogan’s policy position suggests a massive reduction right away.

For the lira, everything depends on the size of Thursday’s rate reduction, and the central bank’s forward guidance.

Rate cuts to boost the flagging economy need to be gradual and backed up by consistently improving data. If a cut of around 225 basis points tomorrow is accompanied by an MPC statement emphasizing a slow but steady path of future reductions the currency could not only handle it, but perhaps even appreciate as the economy recovers.

However, a one-off monster rate cut this week could shock the lira, potentially revive last year’s currency crisis and send inflation back up again. So would a smaller reduction if it were accompanied by hard MPC guidance that further substantial cuts will come.

Ziad Daoud of Bloomberg Economics expects as much as 1,200 basis points of rate reductions by the end of the year. Such a breakneck drop seems a recipe for significant lira weakness.

While the measures that have contained the lira so far could still limit any selloff, there’s still room for a reaction. Trapping the currency would give the appearance that everything is under control, but that can’t last. The longer-term costs would be ruinous, as it is hard to see how foreign investors could be induced to return to Turkey.

A moderate move would signal that there is some independence left at the central bank. Anything else would be the realization of investors’ deepest concerns.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.