(Bloomberg Opinion) -- TUI AG, the world’s biggest package-holiday company, has just secured enough government funding to see it through the lean Covid-affected winter season. A glance at its latest quarterly earnings, released on Thursday, shows this is probably just as well.

The German company reported a 1.1 billion-euro ($1.3 billion) operating loss in the quarter ending June 30, after revenue slumped 98%. It said it burned through 550 million euros to 650 million euros a month during the period. The London-listed shares fell 5%.

Some people have started to brave air travel again in recent weeks, but TUI acknowledged that the situation was still fragile. Demand hasn’t fully recovered since draconian restrictions were lifted, and renewed quarantine measures against popular destinations such as Spain have added to the pain.

Consumer confidence is at risk from a resurgence in cases in some countries and worsening personal finances from job losses and lost business due to lockdowns. Holidaymakers are still reluctant to fly long-haul, important for the autumn-winter season, when TUI now plans to slash capacity by 40%.

The good news is that it has the German state’s backing. Additional funding agreed on Wednesday, which brought the overall aid package to 3 billion euros, is a safety net to get it through the traditionally quieter winter season, when it needs to pay its suppliers for the previous summer. It removed the threat of a short-term cash crunch, which would be devastating. When consumers are nervous about a holiday company’s finances, they avoid booking with it, and the situation spirals. Just look at what happened to British travel giant Thomas Cook, which collapsed last year.

The aid comes with strings attached, though, including restricting TUI's ability to pay executive bonuses. It also includes a 150 million-euro convertible bond, which would give the German state a 9% stake in the company if ever TUI were unable to meet the interest costs.

The question is how long can TUI, which has sold just 16% of its originally planned summer 2020 program, keep managing the uncertainties brought by this virus? And if the outbreak doesn’t go away soon, how much job cutting and asset sales will it take to be nimble enough to operate in a radically new market environment?

While bookings for next summer are up by 145%, some of that is pent up demand from people who canceled this year’s vacations. Even so, TUI plans to operate at 80% of capacity for next summer, an indication it’s preparing for better times ahead. It optimistically expects conditions to return to normal by 2022, based on the demand it has seen since July and the level of bookings going forward.

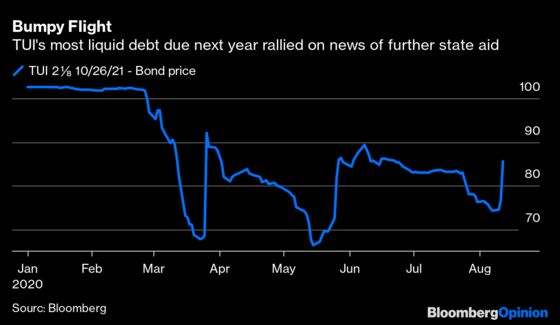

Against this backdrop, leverage looks too high. Net debt, including lease liabilities, stood at just under 6 billion euros at June 30. The company has a market capitalization of about 2.2 billion euros. It also faces about 300 million of bonds maturing in October 2021.

TUI has already undertaken some self-help measures, including a plane leaseback deal and the sale of Hapag-Lloyd Cruises to a company it jointly owns with Royal Caribbean Cruises. But more disposals look inevitable. Up until now, TUI’s strategy has been asset heavy: It has an airline, hotels around the world and cruise ships. TUI still owns the ships within its Marella cruises business for example, so a sale and leaseback of these assets, as well as hotel real estate, is possible. It could also enter into a joint venture for its airline.

The company said on Thursday that it was looking at options to strengthen the balance sheet, including a rights issue, although this could prove tricky given that the London-listed shares are down almost 60% over the past year. It has also outlined a big cost reduction program to save 300 million euros a year by 2023.

With the extra funding and some glimmers of hope on trading, TUI just booked itself some winter sun. The danger is it turns out to be a mini-break from the ravages of the Covid-19 pandemic, rather than a long-term stay.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2020 Bloomberg L.P.