Trump’s Cure for Negative Oil Prices Is … More Oil?

(Bloomberg Opinion) -- As the old saying goes, the cure for low oil prices is funneling federal dollars to over-indebted producers, thereby delaying shutting in supply (or something like that).

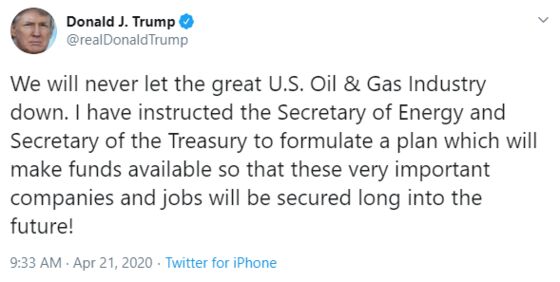

President Donald Trump has been floating various ideas to revive America’s frackers since the jab of a Saudi-Russian price war and the upper cut of Covid-19 sent them reeling. These have included such novelties as paying producers to keep oil in the ground and branding it a strategic reserve. After oil closed in negative territory on Monday, some wags suggested frackers might pay the feds to take the oil under that scheme. But no, this doesn’t work like that. The idea is for money to flow from Washington to the shale fields, not the other way around. I would bet Trump’s “funds available” tweet on Tuesday — henceforth forever known in oil circles as The Day After — is closer to where this is going than, say, “funding secured.”

No American president, Trump or otherwise, can allow the domestic oil and gas industry to simply collapse in chaos — from an economic, security and electoral point of view. Extending help is a fraught exercise, though, given the hazard (and stigma) of corporate welfare and the great divide between the White House and House Democrats in terms of affinity for (and donor links with) the oil and gas sector.

What has compounded the problem is Trump’s “energy dominance” mantra. For starters, the current crisis has laid bare its incoherence. Recall that America’s resource riches combined with free enterprise loosed from the shackles of regulation were supposed to give Washington free rein in global energy markets (and geopolitics). Now, less than a fortnight after the president was haggling with Saudi Arabia, Russia and Mexico to help prop up prices — and not much longer after saying the free market would take care of it — Trump’s tweet hints strongly at a straight-up bailout for the industry.

What shouldn’t be lost, though, is that energy dominance itself helped tee up all of this. With its emphasis on expanding oil and gas supply as much as possible, it mirrored and encouraged the industry’s worst instincts. Frackers roughly doubled America’s share of the global oil market over the past decade. But in doing so, they destroyed untold value for investors; hence their deep unpopularity in the stock market, which long predated Covid 19.

Moreover, the tsunami of supply helped push down oil prices. That’s great for the drivers Trump used to prioritize; less so for producers themselves, both foreign and domestic. At its heart, energy dominance is deflationary, which is lethal for an overextended sector such as this.

In that sense, Trump’s evident desire to push more funding the industry’s way — rather than, say, targeting help to furloughed rig-hands — fits right in. Trying to delay the necessary curtailment to supply (and industry restructuring) would exacerbate the underlying problem of too much supply running into too little demand. Call it energy whiplash.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2020 Bloomberg L.P.