Trickle-Down Economics Has Failed Its Growth Mission

(Bloomberg Opinion) -- The bipartisan infrastructure bill recently passed by the Senate is a sign that U.S. leaders are starting to think differently about government investment. For decades, legislators have tried to push down the cost of capital, believing it would spur a financial investment boom that would trickle down through the economy. But it never seemed to do much to boost capital spending, so a change in strategy is warranted.

When you hear the term “trickle-down economics,” you probably think of the simplified, popular version: Give rich people money by cutting their taxes and they’ll create jobs. But there’s actually a more sophisticated version of that argument support by classical economic theory. Basically, the idea is that if government policy rewards financial investment, people will save more, which will increase the amount of financial capital in the market. That flood of financial capital will reduce the cost that companies pay to borrow money or issue stock, making it more attractive for them to invest. And that investment will create jobs.

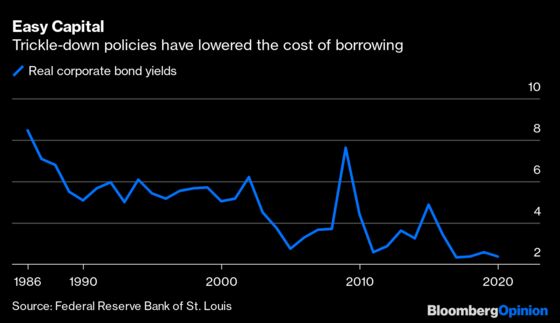

To this end, we’ve cut taxes on capital gains and dividends. And we’ve used financial deregulation to make it easier for savers to put their money into asset markets — stocks, bonds, real estate, etc. — instead of just stashing it in a bank. Those policies have helped push the cost of capital down for businesses. For example, here are real bond yields — the price that big businesses pay to borrow money:

But this flood of cheap capital has notably failed to spur the private sector to spend more on capital projects. Since the investor-friendly policy era began, net private domestic investment has fallen from about 5% of GDP to less than 3%:

Private nonresidential fixed investment has held up better, but is still lower than in the early 1980s.

Without the investor-friendly measures, would business investment have fallen even further? Perhaps, but economists have determined that dividend tax cuts did essentially nothing to spur capital spending in the 2000s. Likewise, the new consensus among academics seems to be that capital gains taxes probably don’t affect real investment that much.

In other words, making asset markets more attractive, in the hopes that this will entice businesses to invest, has been a bit like pushing on a string. It’s likely that when capital costs get low enough, big business finds financing to be less of a constraint.

The broken link in trickle-down economics — even the smart kind of trickle-down — is the one between financial investment and business investment. We may use the same word for both of those activities, but rich people and mutual funds buying up stocks and bonds simply isn’t the same thing as companies purchasing equipment, building buildings or training workers. The economic theories that draw a link between the former and the latter are simply not good descriptions of the way the business world makes decisions.

When a policy approach doesn’t work, you change the approach. The U.S. government needs to abandon trickle-down policies in favor of better ways of boosting investment, and there are some signs it's doing that.

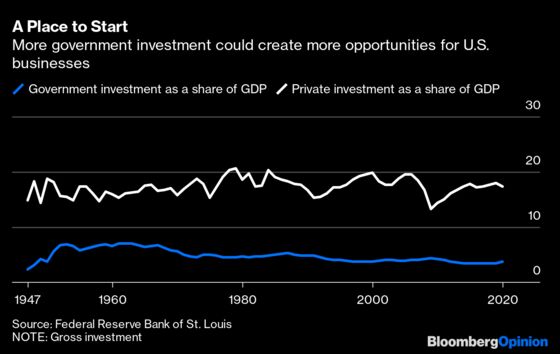

The most obvious alternative is for government to simply do more investing directly. In fact, government investment has diminished significantly since the 80s:

Building the kinds of capital projects that private businesses tend not to do on their own — such as power grids, roads and bridges, trains and ports, clean water infrastructure and broadband — will directly fill a hole in the nation’s investment landscape. If done wisely, it will also draw out more private investment — for example, solar power companies will be much more likely to build plants where there’s a good modern power grid to dispatch the electricity to where it’s needed.

A second idea, whose details are still hazy but which has garnered a large amount of intellectual interest, is industrial policy. If companies’ investment is being limited not by the availability of financing but by the number of good business opportunities, perhaps the government can provide them with more opportunities by helping them export more to foreign markets (or by purchasing their products outright).

It would be wrong to call these approaches “trickle-up” economics, since demand would essentially be coming from the government. But they do form a viable, credible alternative to the trickle-down policy of pumping ever more cash into financial markets and hoping that factories somehow emerge on the other side. That approach has produced notably few actual factories, and thus deserves to be consigned to history’s dustbin.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2021 Bloomberg L.P.