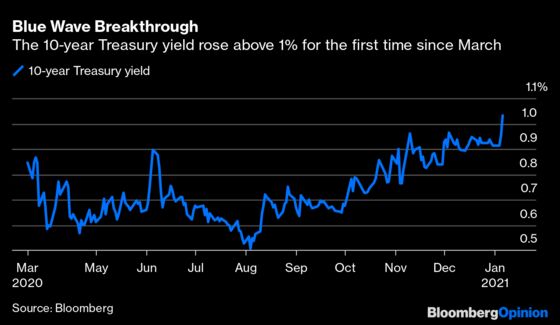

(Bloomberg Opinion) -- For the first time since March, 10-year U.S. Treasury notes yield more than 1%.

That number, of course, is largely a psychological threshold, and interest-rate strategists widely expected the move if Democrats Raphael Warnock and Jon Ossoff both won their Georgia Senate runoff races against Kelly Loeffler and David Perdue, respectively. After the Associated Press and top TV networks called the race for Warnock early Wednesday, and with Ossoff leading Perdue, the benchmark 10-year yield touched 1.03% and the U.S. yield curve reached its steepest level in four years. Meanwhile, stocks fell, with technology shares leading the decline.

These knee-jerk reactions fit neatly into the “blue wave” narrative that has been around financial markets since before the November elections. With Democrats holding the presidency, the House of Representatives and now likely 50 seats in the Senate (with Vice President-elect Kamala Harris breaking any ties), investors expect a larger dose of fiscal aid to propel the U.S. economy past the Covid-19 pandemic. Goldman Sachs Group Inc. economist Alec Phillips, for one, said a Democratic sweep of Georgia would probably lead to $600 billion of stimulus, mostly this year, in addition to the recent $900 billion package.

However, even with a clearer picture of what the Senate will look like in the next two years, a handful of pressing questions remain for bond traders.

For one, a 50-50 split in the Senate leaves a lot of power in the hands of the most moderate members of each party, like West Virginia’s Joe Manchin. Over the past four years, he received a “Trump Score” of 51.2% from FiveThirtyEight, the highest of any sitting Democrat (for context, Harris’s score was 16.7%). Now, it’s not as if Manchin is necessarily stingy with stimulus funds — he has said he wished Democrats found a way to strike a deal closer to $1.8 trillion in October. But he also reportedly clashed with Senator Bernie Sanders of Vermont over the size of stimulus checks. As my Bloomberg Opinion colleague Karl Smith pointed out Tuesday night, Sanders now stands to head the Senate Budget Committee. The party is not a monolith: a “Green New Deal,” for instance, is almost certainly a nonstarter in West Virginia even if it’s popular in the Green Mountain State.

Ascertaining the next move in the world’s biggest bond market may require sifting through the policy priorities of President-elect Joe Biden and his administration and determining what can get passed and how they will impact U.S. economic growth. For all the talk of fiscal stimulus, with the Senate and House on his side, there’s also the possibility of stricter regulation and, once through the pandemic, higher taxes on wealthy Americans and corporations.

One thing investors were counting on, regardless of what happened in the Georgia runoffs, was former Federal Reserve Chair Janet Yellen taking over as Biden’s Treasury secretary. Given her long history of working with current Chair Jerome Powell, it’s reasonable to expect that they will work to keep interest rates under control until they’re confident that the labor market is on its way back to pre-pandemic levels and inflation meets and exceeds the central bank’s 2% target. In a sign of just how far there’s still to go, ADP Research Institute data released Wednesday showed U.S. business payrolls unexpectedly declined in December for the first time since April, causing the 10-year yield to briefly dip back below 1%.

Whether the move higher in Treasury yields lasts may also depend on whether the U.S. and other countries can improve their rollout of Covid-19 vaccines. In its first three weeks, the effort to inoculate 328 million Americans has strained state and local governments as they decide which groups have priority access while also trying to navigating the logistical challenges involved with administering shots that must be kept at subzero temperatures. It’s unclear just how much and how quickly a Biden administration could rectify these nationwide issues. Wall Street largely expects something close to a “return to normal” around mid-year — a delay could have serious economic repercussions.

All the while, investors are seeking to make sense of incoming economic data that all seems to point to building inflation pressure. Institute for Supply Management data released Tuesday showed the gauge of prices paid for materials in December rose to 77.6 from 65.4, clobbering expectations for a modest move higher to 66. It was the highest level since May 2018, with all 18 industries reporting that they paid higher prices last month. Earlier this week, the 10-year break-even rate, a market-based measure of inflation expectations over the next decade, jumped above 2% for the first time since late 2018, around the time the Fed finished raising interest rates. Commodity prices are breaking higher, too.

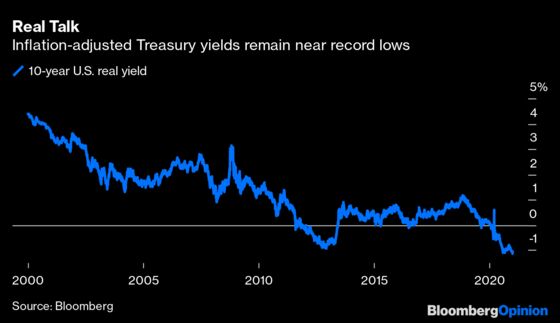

Fed officials hardly seem concerned. “I welcome above 2% inflation. Frankly, if we got 3% inflation, that would not be so bad,” Chicago Fed President Charles Evans said on Tuesday. That sort of scenario, of course, is the bane of all bond investors because future coupon and principal payments will be worth less. Yields would usually race to catch up with that kind of price growth. But as I’ve noted before, the Fed will all but guarantee negative real rates for the foreseeable future, even if it spells trouble for pension funds and insurance companies, in an effort to push traders into riskier assets and boost the economy. As it stands, 10-year real yields are -1.08%, close to a record low.

This context is more important than the round number of 1%. But, at the very least, reaching 1% provides some hope that the U.S. might not be mired in a Japan-like state of near-zero or negative bond yields forever. John Hollyer, global head of fixed income at Vanguard Group Inc., explained what he sees as the strategy from Powell and Yellen in the coming years: “If they’re successful, nominal interest rates are lower, hopefully generating somewhat higher inflation at or slightly above 2%, and that enables stronger nominal GDP growth, which over the course of 10 years or more could lead to a deleveraging as we essentially grow our way out of the debt,” he said. My Bloomberg Opinion colleague John Authers referred to this dynamic as “something close to market Nirvana.”

The obstacle to a coordinated monetary and fiscal policy effort has always been political machinations during times of divided government. That roadblock looks as if it will be removed, at least for the next two years. Still, whether this newly unobstructed path truly takes markets to an idyllic place depends on a series of difficult questions and circumstances that won’t be easily remedied by a simple majority in the Senate.

Getting back to 1% on the benchmark 10-year yield is a big deal. But now comes the hard part.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2021 Bloomberg L.P.