Bond Market Plot Twist Puts Europe's Recovery at Risk

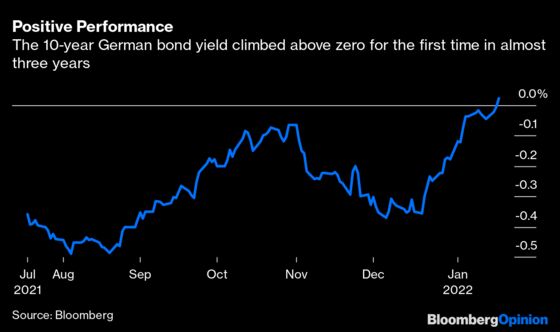

(Bloomberg Opinion) -- The 10-year German bund yield has turned positive after almost three years below zero. It's a sign of the times as government borrowing costs are on the rise globally. With the euro zone’s nascent economic recovery more fragile than that of the U.S., however, the European Central Bank needs to remain vigilant that increased market interest rates don’t choke growth.

Renewed hawkishness at the Federal Reserve has spooked the bond market, with the 10-year Treasury yield approaching 1.9% from 1.5% at the end of last year. German levels have duly increased, climbing above zero on Wednesday after averaging -0.3% in 2021. Foreign holders exiting euro zone debt for the higher income available in the U.S. will naturally drive yields higher unless there is sufficient demand within the euro zone to soak up the slack. The ECB, the biggest buyer in the room, is still scooping up bonds as part of its stimulus effort. Its pandemic quantitative easing program, known as the PEPP, is drawing to a close in March to be replaced by a pre-existing, albeit smaller, package.

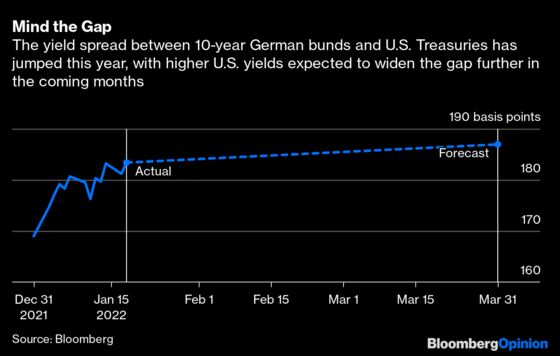

While European bonds haven’t been able to avoid the upward pressure exerted by the climb in U.S. government borrowing costs, they have put up some resistance. The yield gap between 10-year bunds and U.S. Treasuries has widened, to about 188 basis points currently from fewer than 170 basis points at the end of last year, reflecting the faster pace of rising yields in the U.S. bond market. That trend is expected to continue; the consensus forecast of economists is for the differential to remain above 180 basis points by the end of the first quarter.

The more yields rise elsewhere, the greater the attraction for investors to shun the very low income available from European debt in search of more attractive returns across the pond. The timing is far from ideal; analysts at NatWest Group Plc reckon that the net supply of euro government bonds will increase by 424 billion euros ($480 billion) this year as the ECB’s purchases are stepped back as planned.

Higher yields look inevitable even if the asset purchase program is employed skillfully to smooth yield jumps, and particularly to combat any wild swings in the spreads of peripheral countries above that of the German benchmark. Keeping bund yields pegged helps significantly with restricting Italian levels from rising too sharply — the key stress test point of the euro project.

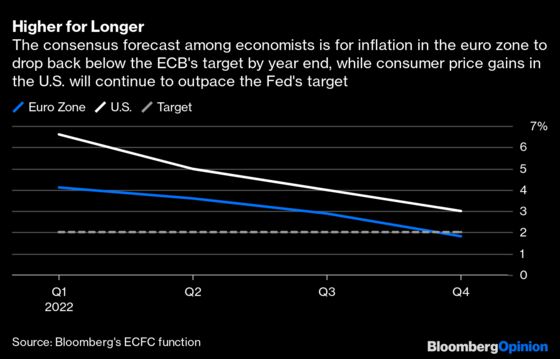

Inflation has rocketed higher everywhere, defying central bankers’ repeated claims throughout last year that price pressures would prove transitory. Consumer prices rose by a record 5% in December in the euro zone, while in the U.S. the measure reached 7% last month, the fastest pace in almost four decades.

In Europe, though, surging energy costs have been the key driver of increased inflation. Those are set to ease as winter ends and gas stockpiles get rebuilt, with economists predicting that inflation will be back below the ECB’s 2% target by the end of December. In the U.S., by contrast, a tight labor market may lead to increased wage demands from workers that leads to price gains continuing to exceed the Fed’s target throughout this year.

It is not just at the 10-year maturity where it’s important to slow the ascent of German yields. The shorter end of the yield curve arguably matters more. The German two-year security has had a rate even lower than the official ECB deposit rate, currently -0.5%, for much of the past decade. The note yield has risen to about -0.55% from -0.78% as recently as November; a breach of the official rate would be a key signal that the market was beginning to price in an ECB interest rate rise, something policy makers will want to avoid given the economic backdrop.

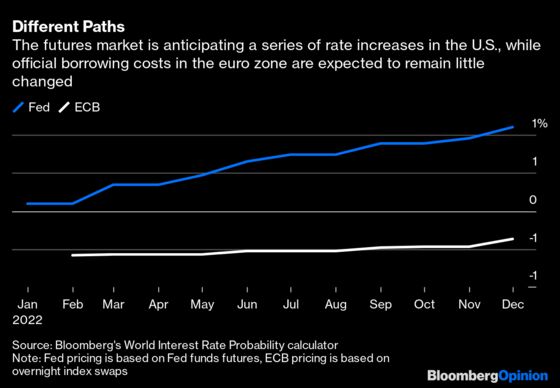

The euro zone’s recovery from the pandemic is far from assured, with Germany likely be in a technical recession by the end of this current quarter. That explains why the ECB is expected to follow its own monetary policy path. Little action is expected from Frankfurt, with scant prospect of an increase in the ECB’s deposit rate anticipated in the futures market. The Fed, however, is seen getting busy in the coming months, with the upper bound of its Fed funds target rate now predicted to reach 1% by the end of the year, up from 0.25% currently.

By breaching zero and turning positive, German bonds have made a symbolic break with recent market history and illustrate that even the Herculean multi-trillion efforts of the ECB can’t hold back the tide indefinitely. Policy makers in the euro zone need to remain alert to the risk that market influences from overseas could undo their efforts to keep a lid on domestic government borrowing costs.

More From Bloomberg Opinion:

- Central Banks Are Playing Catch-Up Differently: Mohamed El-Erian

- The Federal Reserve Needs to Get a Lot More Hawkish: Bill Dudley

- The Fed Faces a Troubling 1965 Parallel: Narayana Kocherlakota

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2022 Bloomberg L.P.