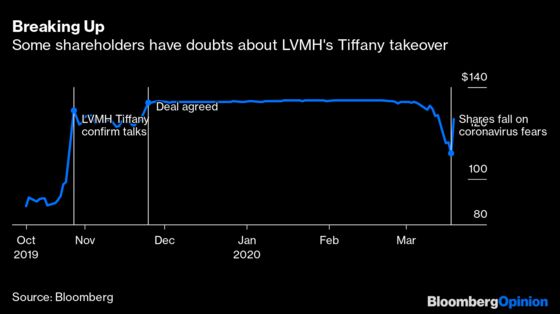

(Bloomberg Opinion) -- A diamond is forever and so, perhaps, is Bernard Arnault’s interest in Tiffany & Co. Investors have been having some doubts that the chairman and founder of LVMH Moet Hennessy Louis Vuitton SA would deliver on his $16 billion takeover of the storied jeweler. But right now, Arnault is behaving like a classic luxury buyer.

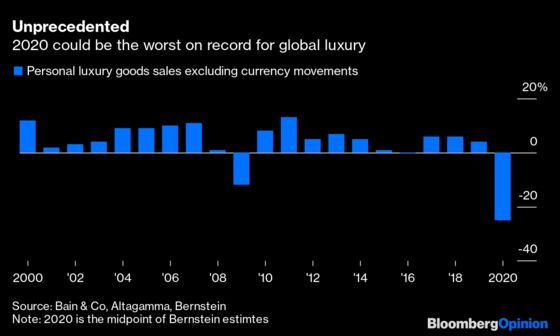

The bid for Tiffany is a long-term investment. Since the deal was agreed in November, the outbreak of the coronavirus has brought an abrupt end to luxury spending, first in China, and now in Europe and the U.S. Bernstein analyst Luca Solca estimates a decline of 20% in industry sales before currency movements this year, assuming a recovery in the second half, and a fall of 25-30% in the event of a global recession.

Tiffany’s stock price is supported by the $135-a-share offer, but touched a year-to-date low of about $111 earlier this week. That large spread suggests an element of uncertainty the deal will actually close.

Shareholders in the U.S. group approved the transaction in early February. Even with the collapse of luxury goods demand, financing shouldn’t be an issue. LVMH raised about $10 billion in a bond sale last month. Bernstein estimates net debt could be in the range of between 1.5 times and 2.5 times Ebitda at the end of this year, depending on how long the pandemic lasts. That’s hardly a stretched balance sheet.

The question is whether there is any provision in the fine print of the deal agreement that LVMH lawyers could use to walk away — and whether Arnault would even want to if there was. Wriggling off the hook would damage Arnault’s reputation and send a terrible message to investors about the strength of LVMH.

The company would also miss out on the long-term potential of Tiffany. Expanding in jewelry is a deeper strategic priority for LVMH. Trophy assets never come cheap, and if LVMH balked, it might struggle to get a second hearing especially if other suitors emerged.

That all fits with what Arnault is doing — mulling the purchase of Tiffany shares in the market, below his offer price. This would be a pragmatic way to try to bring down the overall cost of the deal, without trying to renegotiate, or pressing the panic button.

Of course, staying the course has some cost too. Tiffany needed some polish even before the luxury and the non-food retail industry shuttered stores in response to the Covid-19 outbreak. Elevating the brand just got even harder. And by sticking with Tiffany, LVMH is tying up financial resources that might otherwise be available to buy other assets. In reality, some of the smaller luxury houses have family shareholders who may be unwilling to sell out in a weak market.

The Tiffany deal was never about buying the jeweler’s 2020 earnings. Just as well, for all sides.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2020 Bloomberg L.P.