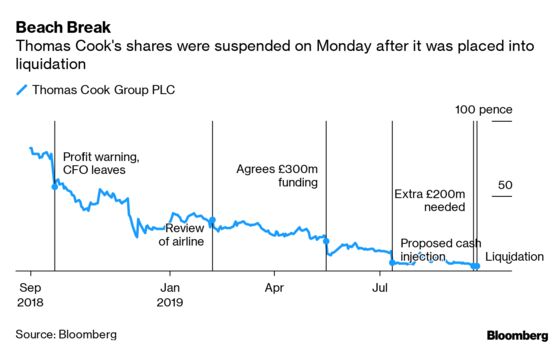

(Bloomberg Opinion) -- As the operation to fly home stranded Thomas Cook Group Plc passengers begins — and the blame game gets going over why the 178-year-old travel agent collapsed — another parallel process is underway: Seeing what can be salvaged from the ruins.

Even before the company entered liquidation, there was never going to be much left for shareholders. They would probably have been wiped out by the failed rescue attempt: A 900 million pound ($1.1 billion) debt-for-equity swap led by China’s Fosun Tourism Group.

Bondholders face a similar fate. Under the rescue plan they would have taken a big writedown on the value of their holdings, but they would have been left part of a group that owned 25% of Thomas Cook’s tour operating business and 75% of its airline. The company’s 750 million euros of 6.25% bonds maturing in 2022 fell as much as 70% on Monday.

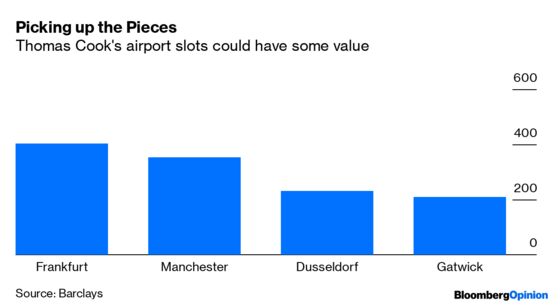

Thomas Cook has some assets that may be worth something. Its British and German airlines have slots at Frankfurt, Dusseldorf, Gatwick and Manchester airports (the German airline is still operating).

There’s an aircraft fleet too. Although the average age of the 100 jets is a fairly old 15 years, according to Citigroup Inc., there might be appetite from emerging market buyers.

The big question is whether there will be anything to gain from snapping up the tour operating arm. Fosun, Thomas Cook’s biggest shareholder, had planned to inject 450 million pounds in the failed rescue deal. It could try now to acquire what is left, which would at least secure the future of its Chinese joint venture with the British company.

Fosun would pick up the historic Thomas Cook name for much less than 450 million pounds. But the collapse, and the emergency repatriation of hundreds of thousands of vacationers, will have done irreparable damage to the famous old travel brand. Would holidaymakers in Britain ever book a Thomas Cook break again? That is the question any potential new owner will be grappling with.

Whatever value can be obtained, it won’t come anywhere near meeting Thomas Cook Plc’s liabilities, which have spiraled over the past year. Net debt stood at 1.25 billion pounds at the end of March. There are also almost 500 million pounds of pension obligations.

No wonder its rivals were looking pleased on Monday. Shares in Germany’s Tui AG rose as much as 10%, while Dart Group Plc, owner of the tour operator Jet2, rose a similar amount. Thomas Cook’s collapse will take capacity out of the holiday market. That’s good news for an industry that has suffered from the shift toward internet booking and slumping consumer confidence as Brexit approaches. Indeed, those factors hastened the company’s demise.

Any positive news for the sector is of no comfort for Thomas Cook’s creditors, of course. The holiday is over for them.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.