Don't Blame Short Sellers for THG's $2.6 Billion Problem

(Bloomberg Opinion) -- “Well, what a year,” said Matthew Moulding, chairman and chief executive officer of THG Group Plc, the seller of protein shakes, skincare and designer clothes, as he introduced an investor event on Tuesday.

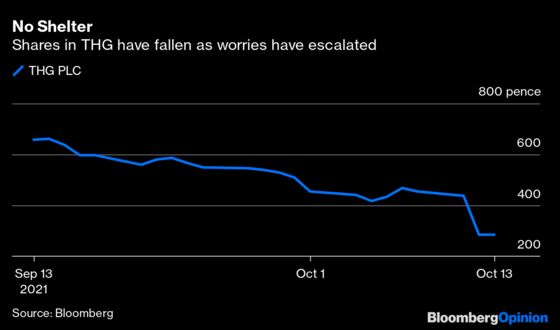

The British e-commerce company has had a rough ride since its 4.5 billion-pound ($6.1 billion) initial public offering in Sept. 2020. And it was about to get worse: Its shares slumped 35% after the meeting, wiping 1.9 billion pounds off of the group’s market capitalization.

THG, formerly known as The Hut, missed a golden opportunity to reassure shareholder doubts about its Ingenuity division, which helps consumer brands sell direct to their customers via the web. Investors rightly punished it.

To recap, Masayoshi Son’s SoftBank Group Corp. has an option to acquire a 20% stake in Ingenuity next year for $1.6 billion, valuing the business at $4.7 billion excluding cash. Should SoftBank exercise this, Ingenuity, which offers services such as hosting websites, managing influencers, facilitating online payments and delivery, would then become a standalone business.

Tuesday’s event was supposed to shine a light on the division, which under the terms of this deal is worth about as much as the whole group. There were upbeat presentations from Revolution Beauty Group Ltd. and the maker of Glenfiddich whisky William Grant & Sons, extolling the virtues of the Ingenuity business. The unit had won more than 100 clients over the last 12 months and lost only two. And THG reiterated that the business was achieving a 60%-70% Ebitda margin. So far, so good.

But some key questions were left unanswered — such as what Ingenuity’s Ebitda margin would be when it is separated. The group stopped short of spelling out the profitability of its other two main divisions, beauty and nutrition. And it didn’t say what an independent Ingenuity would charge these units for its services. (It currently provides them at no additional cost.) That’s crucial to figuring out the valuation of each part of the business.

It was also notable that there were no glowing testimonies from the consumer giants, such as Nestle SA (aside from a reference to personalizing tins of Quality Street sweets), that are also Ingenuity clients. Much of the optimism about the business has been pinned on them.

THG did reveal that SoftBank would not be exercising its option early. Instead, the potential transaction remained on schedule to take place in the first half of next year. Worries now include whether the price will need to be renegotiated and if so, just how much capital, if any, will be injected. That matters, because THG, which is highly acquisitive, has a voracious appetite for cash. The fact that Son hasn’t stepped up to show support for Ingenuity has also sown some doubt about SoftBank’s commitment.

THG tried to calm the situation early Wednesday, saying it had available cash of 700 million pounds as of Sept. 30. The shares fluctuated between a 13% fall and 9% gain.

Against a backdrop of stalling online demand and crumbling consumer confidence, the company needs to offer more reassurance about its future. THG should start by spelling out divisional profitability and explaining exactly what Ingenuity will charge the other divisions. Appointing an independent chairman as a counterweight to Moulding should be a priority too.

As he kicked off Tuesday’s event, the CEO blamed short sellers for the group’s current predicament. But THG’s own lack of transparency is the main culprit. If Moulding wants to build some shelter at his Hut from investor angst, he must do better.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2021 Bloomberg L.P.