(Bloomberg Opinion) -- Given the latest data on the U.S. economy, the Federal Reserve may well be tempted to adopt a less dovish posture on interest rates. But with markets already counting on a 25 basis-point rate cut next week, the Fed’s challenge will be to make clear exactly how it’s thinking about the outlook for the next year.

The data that’s come in since the Fed’s last meeting in June describes a stronger-than-expected economy: The June jobs report was positive, bouncing back after a softer picture in May. Some regional manufacturing surveys have been showing good bounces, suggesting that at least some of their earlier weakness was due to fears about an escalation of trade wars, which have subsided for the time being. Measures of consumer confidence such as Bloomberg’s weekly Consumer Comfort Index have continued to rise. And second quarter earnings have helped lift the S&P 500 and NASDAQ to new highs, with Chipotle, McDonald's, Starbucks and other consumer companies especially strong.

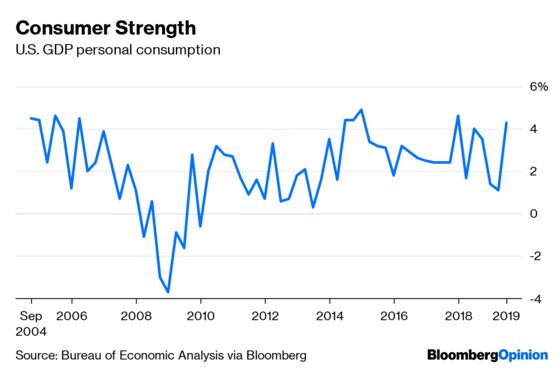

This morning’s GDP report caps off the upward trend, with estimated second quarter growth at 2.1% at a seasonally adjusted annual rate, higher than the expected 1.8%. Personal consumption was particularly robust, growing at a seasonally adjusted annual rate of 4.3%.

If, in response, the Fed signals it may not lower interest rates as much as it had considered doing, it will need to say so delicately. There have been occasions in the past when the Fed has walked back its own expectations for rate hikes, and the markets have welcomed the shift.

But now that markets are positioned for multiple rate cuts, a signal that the Fed may take less action will have a different effect. Although, in June, half the members of the Federal Open Market Committee expected to cut rates twice in 2019, fixed-income markets have been way ahead of that — priced for a better than 50% chance of at least three rate cuts, and at least a 40% chance of four of them by next June.

Should the July meeting end up shifting to “one and done,” with no further cuts to follow, that will be, from the markets’ point of view, the equivalent of three rate increases by the middle of next year.

If the Fed has learned anything from its recent communications struggles, it should be that when talking about the economy and tipping its hand on monetary policy, it needs to consider how markets are already positioned. When New York Fed President John Williams spoke last week, markets took his dovish remarks to imply that the Fed was considering a 50 basis-point cut this month. His office had to clarify that this was not what he meant to say.

Essentially, the Fed has two difficult tasks next week: determining policy, and communicating that without disrupting markets. The outlook has shifted since June, when global economic data and sentiment among U.S. business leaders were moving in the direction of more rate cuts. Yet fixed income traders appear to be ignoring the change. Should the Fed feel the need to let down those hoping for multiple rate cuts, it will need to tread lightly.

To contact the editor responsible for this story: Mary Duenwald at mduenwald@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Conor Sen is a Bloomberg Opinion columnist. He is a portfolio manager for New River Investments in Atlanta and has been a contributor to the Atlantic and Business Insider.

©2019 Bloomberg L.P.