Tokyo’s Real Superhero Stocks Need to Take Center Stage

(Bloomberg Opinion) -- To wipe out superheroes, the villain of the Pixar movie “The Incredibles” had a fiendish plot: He would make them ubiquitous. “When everyone’s super,” the villain named Syndrome opined, “no one will be.”

The Tokyo Stock Exchange has no such diabolical goals. Yet it’s at risk of making Japan stocks just as irrelevant with its much-hyped but disappointing market reorganization, which created a new “Prime” segment to house Japan’s best companies — then opened the category to almost everyone.

The exchange ditched its confusing existing segments at the start of April and created three new sections for Japan’s nearly 4,000 listed companies, including the top-tier Prime segment. But Prime has launched with 1,836 members. Some of its members include Brass Corp., a wedding planner in the industrial heartland of Aichi with a $37 million market cap; Tokyo Ichiban Foods Co. Ltd., which operates 75 blowfish restaurants; and P-Ban.com Corp., a maker of circuit boards with 28 employees. Do these stocks really represent the best of Japan’s business world?

Reaction among investors has been less than kind. “The Sinking of the Tokyo Stock Exchange,” declared the cover of the weekly magazine business Toyo Keizai last week, asking rhetorically: “Is this good enough, Japanese stocks?”

In other words: when nearly everyone is a Prime stock, no one is.

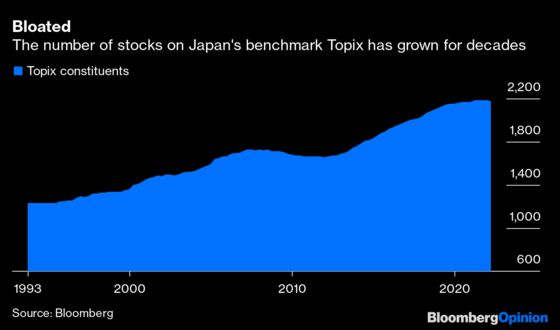

There’s a feeling that the restructuring is a missed opportunity that won’t soon come again. The plan began as a grand vision to overhaul Tokyo’s confusing, overlapping market structure and reduce bloat. Investors had complained that the benchmark Topix index contains too many companies.

Until Prime, the Topix was made up of the companies on the TSE’s First Section, as the top tier of firms was known. Saying that you (or your recently graduated son or daughter) work at an ichibu jojo kigyo became synonymous with success — the equivalent of being employed at a Fortune 500 company, at least before everyone wanted to work for a Silicon Valley startup.

But over time, lax listing standards meant that being part of the First Section became akin to a participation prize. The number of companies on the index has more than doubled in the past three decades to some 2,172 constituents. Index funds tracking the Topix must buy and sell shares in hundreds of these low-liquidity minnows.

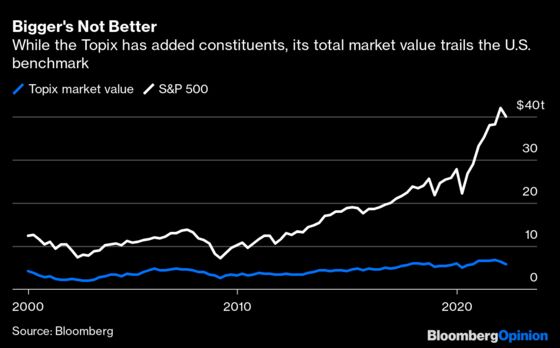

Compared to the S&P 500, China’s CSI 300 or the 40 members of Germany’s Dax, Japan’s benchmark looks ludicrously swollen (the trimmer but price-weighted Nikkei 225 faces different but equally frustrating issues), even as the country’s stock market has largely treaded water compared to the U.S.

The hope was that the market reshuffle would fix this, and help make Tokyo a more attractive location for the foreign investors crucial to the long-term success of Japanese stocks. Prime promised to be a stage for the country’s biggest firms, with the exchange promoting a market for companies who valued “constructive dialogue with global investors.”

But those initial hopes failed to materialize. The criteria for Prime stocks ended up being pretty lax, including a market cap requirement for new listings of just $200 million, and less for firms grandfathered in. By contrast, the smallest company on the S&P 500 has a market cap of nearly $6 billion, or some 30 times larger.

Worse, the standards were fudged still further: Companies that didn’t make the listing criteria could apply to be on Prime nonetheless, simply by submitting a plan that promised to meet the requirements somewhere down the road. Even as the restructuring came into effect, the TSE has yet to outline when this “comply or explain” approach will give way for something with more teeth.

The result: fully 84% of the companies on the First Section ended up on Prime. The Topix itself also remains, set to be slimmed slightly in an excruciating multi-year period. Where’s the reform?

The exchange is asking for patience. Over time, the market will be pared down, Tokyo Stock Exchange Chief Executive Officer Hiromi Yamaji told me in January, as the burden of meeting corporate governance standards takes a toll. He encouraged investors to focus on the change in each company rather than the number of companies.

For now we’re left with a muddle. The reorganization gave no boost to the market. All three market segments having fallen since its inception. Investors haven’t noticed any improvements to pay attention to Tokyo.

A glacial pace of change and desire to please all parties is a familiar refrain to followers of Japanese reform. But like so many of the issues the country faces, the luxury of time is no longer on Tokyo’s side as rivals in other countries move faster.

The vision isn’t wrong. The goal is commendable: Market simplification is long overdue. But Japan has real stock market stars — for example, Keyence Corp., the robotic automation specialist; Recruit Holdings Co. Ltd., the operator of the largest U.S. job-hunting site; and Daikin Industries Ltd., the air-conditioning giant deserve larger global recognition than they now receive. Tokyo needs to put its authentic superhero collective together and let them take center stage.

More From This Writer and Others at Bloomberg Opinion:

-

With Borders Still Shut, Japan Risks Becoming ‘Pure Invention’: Gearoid Reidy

-

I Caught Omicron. People in China Thought I Was Dying: Shuli Ren

- Hong Kong Expats, Where’s Your Next Destination?: Anjani Trivedi

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Gearoid Reidy is a Bloomberg News senior editor covering Japan. He previously led the breaking news team in North Asia and was the Tokyo deputy bureau chief.

©2022 Bloomberg L.P.