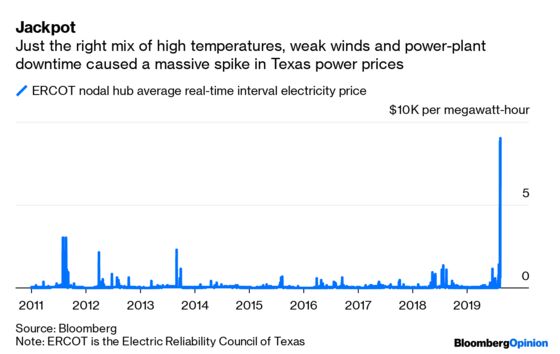

(Bloomberg Opinion) -- There’s a Vegas-like quality to the Texas electricity market. Whereas other regions use factors like capacity payments to encourage new power plants, Texas relies on the spin of the wheel. If temperatures are hot enough, and the wind is calm enough, and enough power generators go offline unexpectedly, a scramble for power spurs prices from the usual range of $20 to $30 per megawatt-hour up to $9,000.

And that’s what happened last week:

Merchant generators in Texas play this slot machine, hoping for a handful of these windfalls. BloombergNEF estimates the state’s generators reaped $1.5 billion across just two days last week, equivalent to more than 10% of the money paid in the wholesale electricity market last year.

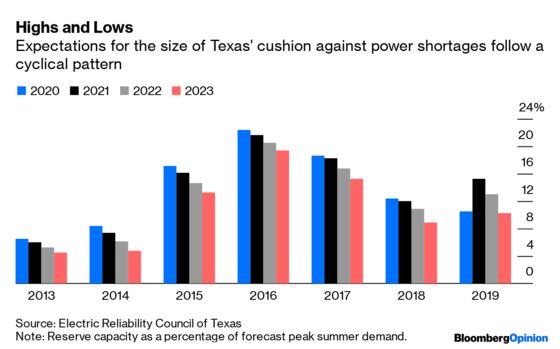

The Electric Reliability Council of Texas, or Ercot, banks on such jackpots tempting developers to build more capacity. The mechanism works, more or less, but the inevitable lag between market signals and new construction can leave the power market dangerously close to shortages — and consequently the spikes. This is shown clearly in the reports Ercot publishes twice a year providing a forecast of the state’s “reserve margin,” or spare capacity. The target level is 13.75% of peak demand. Here are the forecasts for 2020 through 2023 taken from the May report over the past seven years:

The latest forecasts suggest expectations are beginning to turn again. While the expected reserve margin for 2020 has shrunk further, it has expanded further out, moving back above the target level in 2021. That may prove optimistic.

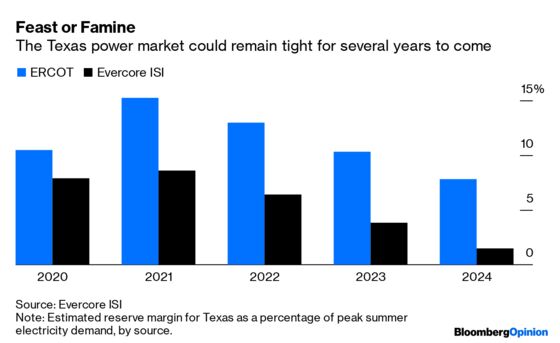

NRG Energy Inc., one of the biggest power generators and retailers in Texas, said on its recent earnings call that Ercot most likely overestimates new capacity and underestimates closings. As warnings go, this one is less a call to arms and more a pitch to buy; NRG’s plants should profit in a tighter, more volatile market. That said, it is safe to assume that much of the roughly 112 gigawatts of proposed projects — substantially bigger than the state’s total existing capacity — will not materialize. Less than a quarter of it had an agreement to hook plants into the grid signed at the end of July. Wind and solar projects dominate Texas’ pipeline and Greg Gordon, an analyst at Evercore ISI, typically discounts these by 35% and 75% respectively. He forecasts much tighter conditions in the medium term:

In theory, this alternative view should spur new projects, especially solar farms. Hot, muggy days can mean air conditioners crank up just as the state’s formidable fleet of wind turbines slow for want of a breeze. Solar power, on the other hand, is tailor-made for those dog-day afternoons. But the state’s solar capacity of 1.9 gigawatts is low, and while there is a nominal 62 gigawatts in the works, most of it will never see the light of day. Tara Narayanan, a solar analyst for BloombergNEF, points to the impending roll-off of the investment tax credit for renewable projects as well as President Donald Trump’s tariffs on imported solar modules. Taken together, these mean the optimal window for building solar capacity approved before the end of 2019 is actually in 2022-2023, when developers can still utilize the highest tax credit while also purchasing equipment unburdened by the tariffs.

Ercot’s pipeline suggests perhaps 3.4 gigawatts of new solar capacity entering service by the end of next summer. Using that as a conservative estimate and plugging it into BloombergNEF’s U.S. “Power Mixer” tool, the result implies a cut to average peak summer prices in 2021 of almost $4 per megawatt-hour, knocking perhaps $270 million off fleet revenue. That’s unhelpful for merchant generators but hardly a game changer.

Yet the game is changing at a broader level. Texas, like so many other power markets, is undergoing a transition. In addition to wind power, cheap shale gas pushes down on power prices while rising demand and the retirement of older thermal power plants offer support. Even if solar power has been slow to take hold, and reserve margins remain low, the Texas power market represents a gamble. After all, last week’s spike came after a months-long slump in power futures as expectations of a lucrative heat wave had declined. Similarly, while 2018’s summer was a hot one, there were no big price spikes that year. This is one reason, even with near-term reserve margins looking tight, investors have been reluctant to price that fully into generator stocks. It is also why, even with the prospect of markets remaining tight, there will be no wave of construction in big conventional plants. Solar’s quick lead times and the ability to scale up alongside demand is a structural advantage.

The price volatility, and expectation of more, is spurring one important part of the market to take matters into its own hands: commercial and industrial customers. As even the likes of Exxon Mobil Corp. have discovered, a long-term renewable supply contract can deliver energy at stable prices, and the cost of such power continues to drop. Corporate power-purchase agreements signed in Texas this year are likely to surpass those for the entire U.S. just two years ago, according to BloombergNEF. Power producers in Texas should enjoy decent odds of more jackpots in the next few years, but the house is moving against them.

This assumes, of course, that neither the tax credit nor the tariffs are extended.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.