(Bloomberg Opinion) -- "When shall we three meet again? In thunder, lightning, or in rain?"

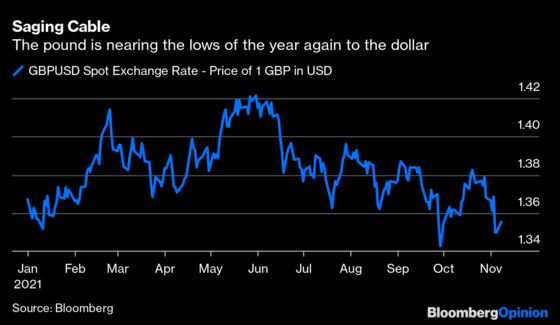

That’s the first witch setting the opening scene in Macbeth but it might as well be any commentator on the current state of the U.K. or outlook for the pound. The lows for sterling this year versus the dollar at $1.34 look set to be tested again soon. Sterling is not going to fall apart suddenly but there are notable headwinds.

It's pretty tough to find anything positive to say after the week the U.K. just had. A sleazy lobbying scandal has hobbled the government. And the Bank of England’s head-fake over interest rates kicked out the last remaining obvious prop for the currency: the prospect for a steady series of hikes.

This might imply that sterling is oversold because all the bad news is out. But there is still plenty that can get worse for the pound longer-term. Some of that is out of the U.K.'s control such as persistent dollar strength or global commodity squeezes. But there is room for harm.

Sterling tracks closely with the euro and there shouldn’t be a dramatic change in the pair’s relationship because the European Central Bank is not expected to raise rates for the foreseeable future. But Europe is still important for how the rest of the world conducts business with the U.K.

That political backdrop very much affects the pound’s value. As the COP26 climate-change jamboree in Glasgow finishes up, political attention will turn back to Brexit and whether the recent skirmishes over fishing and the Northern Ireland protocol burst into a major conflagration. Brexit is becoming a lifetime pursuit, with the pound caught right in the crosshairs.

Since the 2016 referendum, there has been a handbrake on foreign direct investment returning in significant scale and duration due to uncertainty of how global Britain resets itself. Even the most favorable trade outcome with the EU is now growth-neutral at best: It is more about damage limitation.

U.K gross domestic product should grow 7% this year and be not far off that pace in 2022, probably at the top of the G7 economies. But it had further to come back from a tougher pandemic contraction. With the U.S. economy already back above pre-covid levels, the runners-up race between the EU and the U.K. is now of marginal interest.

As Kit Juckes, currency analyst at Societe Generale SA, put it to me in a phone conversation Monday, there is more sand in the British machine, which has a worse growth and inflation balance than its competitors around the world. Growth estimates from the Bank of England, Treasury and the Office for Budget Responsibility all taper off sharply from 2023 onwards.

Now all these official predictions could prove as unreliable as they have in the past. But the openness of the British economy and its dependence on imports just leave it more vulnerable. The British duck needs to be luckier than the rest of the flock; or else it has to be paddling more furiously to get ashore.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2021 Bloomberg L.P.