(Bloomberg Opinion) -- If you believe in the adage that a healthy economy can’t exist without a healthy financial system, then you’re in luck. It wasn’t looking good for large banks when news broke last weekend that Wall Street firms were liquidating the positions of Bill Hwang’s Archegos Capital Management after it failed to meet margin calls. Estimates of the firm’s total positions reached $100 billion. The first question that came to mind was whether this had the potential to turn into a financial crisis; early reports focused on “excessive leverage” and Archegos’s generous use of derivatives to amplify bets.

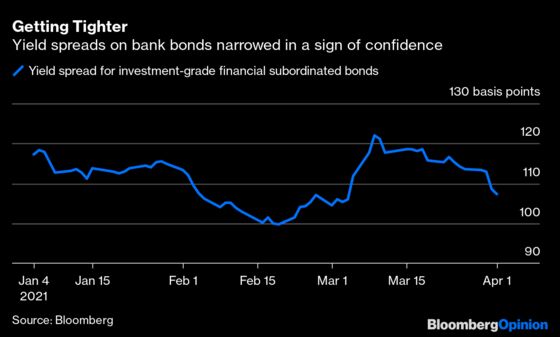

Sure, a number of Wall Street banks said their earnings — not to mention their reputations — will take a hit, but it’s nothing that can’t be handled. That is clearly evident in the benchmark KBW Bank Index, which was little changed for the week, as well as in the corporate bond index, where a tightening of yield spreads suggests banks are more creditworthy now than before the Archegos revelations.

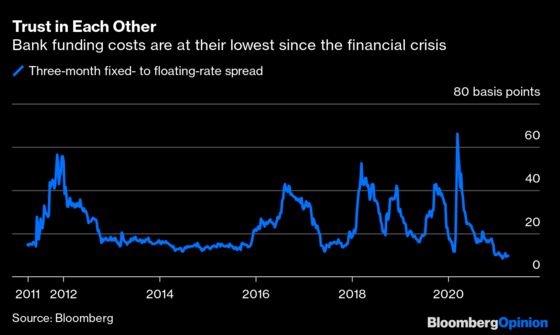

If the Archegos episode had the potential to devolve into a true crisis, nobody would know better than the banks themselves. And yet overnight funding costs for banks barely budged. This critical gauge of stress in the financial system ended the week right around 10 basis points, which compares with about 80 basis points in the early days of the pandemic in March 2020 and the average of 23 basis points since the global economy began to recover from the Great Recession.

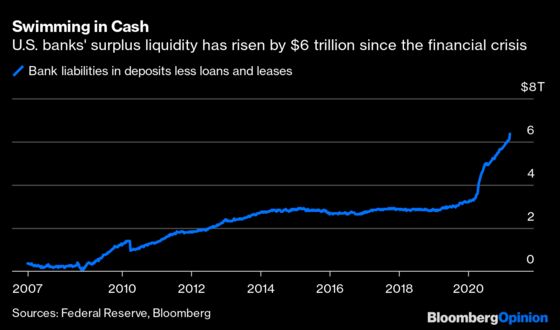

Thanks to reforms put in place after the financial crisis more than a decade ago — the Volcker Rule, the Dodd-Frank Act, Basel III — the banking sector is in strong shape. It’s certainly fine to quibble with the various stress tests that the Federal Reserve conducts on banks, but it’s hard to say they don’t keep enough in reserve to cover unexpected shocks and blowups. Fed data show deposits at U.S. banking institutions exceed loans — a measure of surplus liquidity — by about $6.37 trillion. That’s up from about $3 trillion entering 2020 and about $250 billion in 2008 just before the financial crisis.

The Archegos collapse does raise some important questions about leverage in the financial system. Namely, if an unregulated “family office” can use debt and derivatives to leverage $10 billion of capital into market positions totaling $100 billion, what else are bankers allowing to happen, especially among hedge funds?

The strategists at JPMorgan Chase & Co. published a report this week that said that although the amount of leverage in use at hedge funds — 1.5 times — has reached a level not seen since just before the collapse of Lehman Brothers in late 2008, it’s “significantly below” the historically high levels of about 2.25 times seen around the Long-Term Capital Management crisis in 1998. Here’s how they summed up their findings:

At the aggregate level neither bank leverage nor overall leverage via derivative exposures appear to be an acute source of concern for the financial system.

Cynics might say that’s exactly what you would expect JPMorgan, as America’s largest bank and a key cog in the financial system, to conclude. That’s fair, but the banking system has been tested multiple times in recent years and passed each one with flying colors. Some examples include last quarter’s global bond selloff, which would have brought the banking system to its knees before the financial crisis; the plunge in equities in February and March of last year, which resulted in the fastest bear market in history; the “Volmageddon” episode in February 2018, which caused market volatility to go haywire; the Brexit referendum in 2016; and China’s botched currency devaluation in 2015.

This is not to say that regulators can ease up on banks. They need to stay vigilant, moving quickly as they did last June when the Fed barred big banks from raising dividends as the pandemic worsened and concern intensified that mass defaults by borrowers would ensue. The economic recovery can’t happen unless banks are in a strong financial position.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is the Executive Editor for Bloomberg Opinion. He is the former global Executive Editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2021 Bloomberg L.P.