(Bloomberg Opinion) -- The popular narrative around the GameStop Corp. saga this week was that the episode exposed the excessive froth in financial markets. What other explanation could there be for how an army of neophyte day traders was able to push shares of the down-on-its-luck retailer from less than $20 earlier this month to an intraday high of $483 on Jan. 28 and force some heavyweight Wall Street hedge funds that were betting against the stock to capitulate? There could be no clearer sign that a market top had been reached, even if Warren Buffett had appeared on the floor of the New York Stock Exchange and waved a checkered flag.

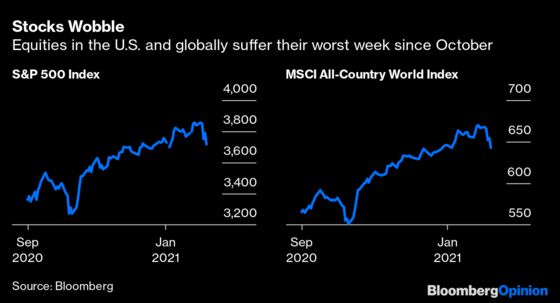

After all, most have heard of the Wall Street adage that when the dumb money — small investors — is buying, it’s time for the smart money — institutional investors — to sell. Such thinking would help explain why the S&P 500 Index had its worst week since October, falling 3.31%, and the MSCI All-Country World Index tumbled 3.57%, also the worst since October.

The reality is a bit different when it comes to the broader market. Despite the tremendous — and largely unexpected — rally in equities since the end of March amid a worsening pandemic and the greatest economic downturn since the Great Depression, investors big and small have been downright cautious. The strategists at JPMorgan Chase & Co. put it in perspective with a report showing that equity positioning sat in the 30th percentile of a 15-year range. It’s normally in the 60th percentile.

That’s a lot of dry powder waiting for a pullback. That’s not me speaking, but JPMorgan, one of the world’s biggest and most successful banks, and it’s market analysts led by Marko Kolanovic, who has dominated Institutional Investor’s annual rankings of top strategists for a decade or so. It’s another adage, but Kolanovic and his team are so confident in the outlook for equities that the subtitle to their report issued Wednesday was “Buy the Dip.”

“Currently there are no signs of exuberance in institutional equity positioning,” Kolanovic wrote. “Any market pullback, such as one driven by repositioning by a segment of the long-short community (and related to stocks of insignificant size), is a buying opportunity.”

What about evidence of excessive froth? True, the rally in equities has pushed the S&P 500 to about 21 times earnings estimates for this year, which is not far below the record highs during the dot-com bubble of the late 1990s. But the benchmark has gained only about 30% over the last three years, far below what Kolanovic says is considered an asset bubble, which is a quadrupling of prices over the same period.

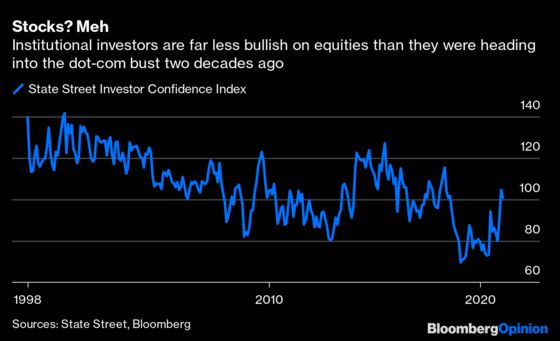

It should be comforting to the bulls that JPMorgan isn’t the only one finding a lack of, well, irrational exuberance toward equities. A State Street Global Markets monthly index — which is derived from actual trades rather than survey responses and covers 15% of the world’s tradeable assets — shows that investors are mostly neutral. The latest index reading of 100.7 (where 100 indicates investors are neither increasing nor decreasing their long-term allocations to risky assets) is below the average of 106.4 going back to 1990. In the recent past, it reached as high as 115.3 in April 2018 and 127.1 in June 2015.

This not to say that pullback or even a correction, which is defined as a 10% or greater decline of an index or asset from its peak, shouldn’t be expected. In fact, the positioning indicators suggest investors think such a drawdown is probably likely.

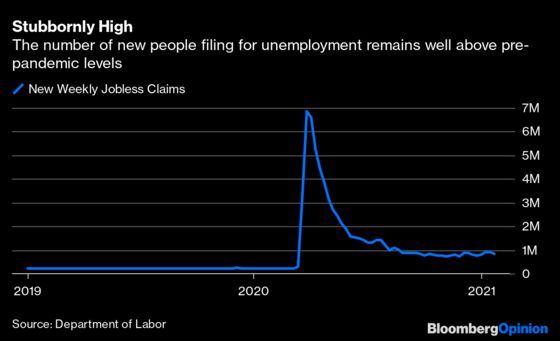

It’s understood that the economy, although on firmer footing, still faces stiff headwinds. Some 10 million Americans who lost their jobs during the pandemic remain out of work. The government said Thursday that new weekly jobless claims totaled 847,000, having risen from about 711,000 in early November in a concerning trend. Without an improvement in the labor market, the economy will be hard pressed to meet consensus growth forecasts of 4.1% for this year.

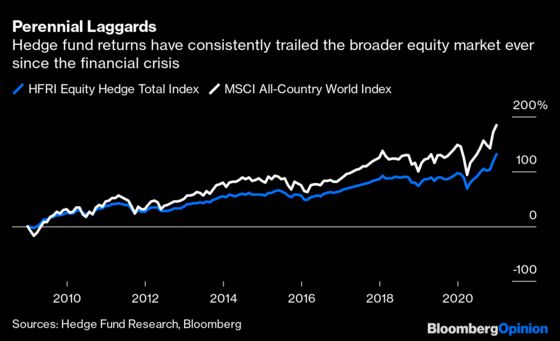

One last thought on hedge funds: There’s a myth that they have some secret knowledge, formula, insight or whatever you want to call it that allows them to consistently rack up superior market-beating returns. If only that were true. The fact is, they have consistently underperformed since the financial crisis more than a decade ago.

Many studies have tried to determine why they have lost their edge. Explanations range from more transparent markets to too much competition to a simple misunderstanding of how asset prices would respond to an extended period of low interest rates and easy money. Whatever the reason, perhaps the assumption about who is the dumb money and who is the smart money needs to be rethought.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is the Executive Editor for Bloomberg Opinion. He is the former global Executive Editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2021 Bloomberg L.P.