(Bloomberg Opinion) -- The Covid-19 pandemic arrested the plans of millions of Americans to purchase a home. But what if you lock someone down in a home they had already mentally moved out of? Might they pour their energy into touring homes online to produce a short list of targets? And might they get preapproved for a mortgage so it’s a simple matter of income verification once the economy reopened and they’d submitted an offer on a home?

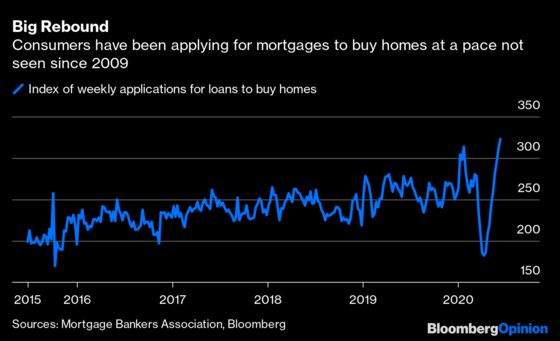

Of course they would, which helps explain the huge surge in the Mortgage Bankers Association of America’s index tracking applications for loans to buy homes. That gauge has risen for nine straight weeks to reach its highest level since the start of 2009, which defies logic when you consider that more than 44 million Americans have filed for unemployment benefits since mid-March. No doubt that some of this is tied to the minor exodus from densely populated cities. After all, long commutes are less of an issue now that we’ve seen the efficacy of working from home play out in real time.

But don’t let mortgage applications fool you. Entering into a deal to buy a home now could prove unwise. Much of the real estate market remains in a deep freeze, with listings down nationwide and borrowers struggling to meet debt payments. Black Knight Inc. reports that 4.73 million mortgages, or 8.9% nationwide, are in forbearance. “During the Great Recession, it took more than two years for the national delinquency rate to increase by the 3.1% seen in April 2020 alone,” Black Knight noted in a report.

Including the emergency programs in the CARES Act, 29.5 million Americans are receiving unemployment benefits, up from 1.7 million in early March before the Covid-19 pandemic took hold. The extra $600 a week many are receiving from the government is set to end July 31. Fresh data from the Federal Reserve showed that Americans’ net worth fell by a record $6.55 trillion in the first quarter to $100.8 trillion, the largest drop in records back to 1952.

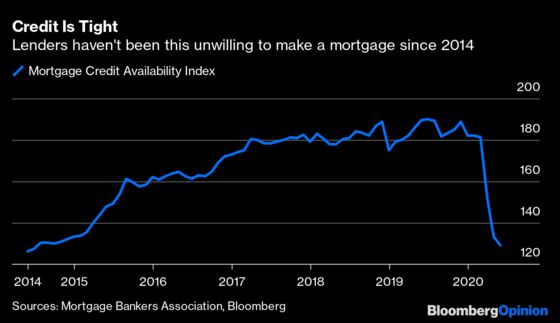

Lenders know all this. Which explains why the MBA’s Mortgage Credit Availability Index has tumbled to a six-year low. Tighter lending standards applied at both ends of the spectrum, from first-time buyers to conforming and non-conforming jumbo loans. Several lenders including Wells Fargo & Co., which is planning job cuts of its own, have shuttered their jumbo loan lending operations and pulled back on home equity lines of credit. Tellingly, homebuilder Hovnanian Enterprises Inc. has announced job cuts with the aim of reducing overhead and other costs by $20 million, which is not what one would expect if the housing outlook was bright.

The elevated number of weekly initial jobless claims are starting to capture a second, potentially more damaging wave of layoffs. A recent study by Bloomberg Economics found that close to six million white-collar jobs are at risk, many in high paying professional services, finance and real estate. A subsequent study found 30% of workers who lost jobs between February and May will become permanent job losses stemming from demand destruction.

A dearth of home supply has buoyed prices for years, a phenomenon that grew exponentially as listings were pulled in the wake of shelter-in-place orders. According to Realtor.com, listings were down by 30% in early May over the prior year. They are still down a hefty 21% and are unlikely to shrink much further. And if they expand, it may be due to millions of retirees deciding to list their homes and monetize any wealthy they have built up.

This will pinch the construction of high-end homes, which has boomed the past decade, putting a drag on the economy. Housing accounted for 15% of gross domestic product in 2018, including residential fixed investment and spending on housing services.

In a first glimpse of what’s to come, Realtor.com on Thursday released a fresh index gauging the recovery of the housing market. While activity was brisk in cities crawling out of shutdown mode, those that reopened the earliest such as Houston, Phoenix and Tampa have all seen their readings come off their post-reopening highs.

The smart and patient buyers see what’s happening. They know to wait until forbearance expires and increasingly tight mortgage lending standards wash out the eager but unqualified. They know that the pent-up demand will be satisfied and that the artificial dearth of supply will become robust, which will pressure prices lower.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Danielle DiMartino Booth, a former adviser to the president of the Dallas Fed, is the author of "Fed Up: An Insider's Take on Why the Federal Reserve Is Bad for America," and founder of Quill Intelligence.

©2020 Bloomberg L.P.