The Market's Garbage Is Starting to Stink

Early warning signs in the junk-bond market lead commentary. Plus Peloton’s plunge, a head-fake for Fed watchers and more.

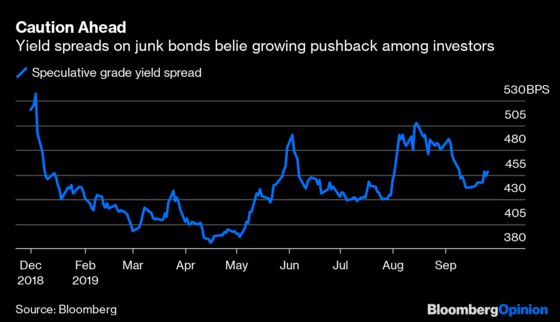

(Bloomberg Opinion) -- While the investing world has been focusing this week on U.S. stocks, Treasury securities and the dollar as an impeachment inquiry against President Donald Trump unfolds, the real action has been in junk bonds. It’s not so much that there’s been a big move in the market for high-yield, high-risk debt; it’s more that there are troubling early signs of a buyer’s strike.

At least four speculative-grade companies have pulled their debt offerings this month, and a growing number of others have been forced to either boost the interest rate offered on their bonds and loans or dangle sweeteners to drum up investor demand and complete deals, according to Bloomberg News. At 4.59 percentage points as of Thursday, the extra yield offered on junk bonds over Treasuries is the highest in more than two weeks. While that’s no reason to panic – spreads are far below this year’s peak of 5.36 percentage points in early January – it still bears watching, especially if the softness in the new-issues market continues. The credit market, especially for lower-rated borrowers, has often proven to be a sort of early-warning system for riskier assets in general, making big moves in advance of those in stocks, as was seen in May and August. A recent monthly survey of credit investors by Bank of America, the second-biggest underwriter of junk bonds this year, provides more reason for caution. It found that 57% of high-yield investment managers are holding above-normal cash levels, up from 35% in July and the most since the firm starting asking about cash levels in 2011. The stakes have never been higher. There are about $1.25 trillion of bonds with below-investment-grade ratings in the benchmark Bloomberg Barclays U.S, Corporate High Yield index, or double what it was before the financial crisis. That’s not including the $1.2 trillion of leveraged loans outstanding.

Maybe the latest pushback will prove to be the pause that refreshes, especially with credit-ratings companies forecasting a relatively benign outlook for defaults. Moody’s Investors Service sees the default rate at 2.9% in mid-2020, compared with 3% in mid-2019. History, though, shows how quickly that can change when the economy turns – and what can happen to markets when those high yields no longer seem worth the high risk.

KEEP PEDALING, PELOTON

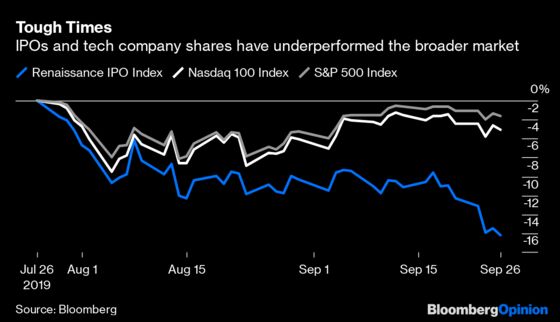

Peloton Interactive Inc. describes itself as “a technology company that meshes the physical and digital worlds to create a completely new, immersive, and connected fitness experience.” Those first three words may be its biggest problem at the moment, with the tech-heavy Nasdaq 100 consistently underperforming the broad market since July after outperforming by a wide margin this year up to that point. Shares of Peloton fell as much as 14.6% Thursday after the company raised $1.16 billion in its U.S. initial public offering. The decline marks the third-worst debut in 10 years among companies that have raised at least $1 billion in the U.S. equity market, according to Bloomberg News. It also adds to an alarming number of listings of unprofitable startups that have flopped as they began trading. As with the softness seen in junk bonds, this isn’t necessarily a bad thing, because it shows that investors are exhibiting caution. Historically, surging IPOs have been a sign of a market top and irrational exuberance. The Renaissance IPO Index of newly public companies has tumbled 14.2% since peaking on July 26, compared with a decline of 1.38% for the S&P 500 Index. The discipline toward IPOs could be a sign that if and when a broad downturn in stocks hits, it might be relatively mild.

FED WATCHERS ARE FLYING BLIND

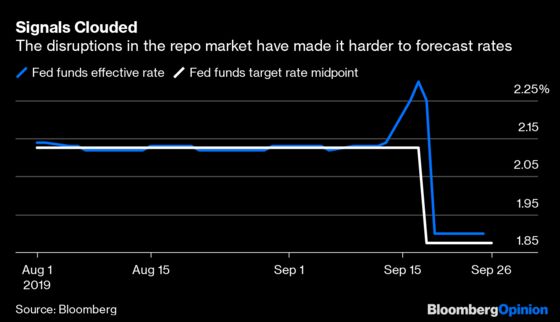

One byproduct of the ruckus in the repo market is that it may be making it harder to deduce what signals are being sent by the bond market regarding the outlook for Federal Reserve monetary policy. The market is pricing in only about a 50% chance of another interest-rate cut by the Fed at its next policy meeting at the end October, which would be its third since July. The problem is, such implied odds are based on the effective federal funds rate and not the actual target rate. That’s an issue because with the problems in the repo market, the effective rate has diverged from the target rate to trade at a premium, according to James Bianco of Bianco Research. “As the effective fed funds rate moves higher relative to the Fed’s set target, it lowers the probably of a cut” as calculated by various programs traders use to gauge such odds, Bianco wrote in a research note Thursday. A better proxy of what the Fed may do is the yield curve – specifically, Bianco says, the difference between three-month bill rates and 10-year yields. That gap has been inverted, with short rates higher than longer-term yields,since May, a clear sign that the bond market feels Fed policy is still too tight.

IT’S A GAS

The market for natural gas is one of the more wild ones anywhere in the world. Big swings are the norm, and nobody really knows when they will come or how much joy or pain they will cause. The final months of 2018 are a good example. Prices soared more than 41.4% in November only to tumble 36.3% in December and an additional 4.29% in January. Events in recent days have traders wondering whether the market is poised for another wild ride. Natural gas futures dropped as much as 4.48% Thursday in their biggest decline since January. Not only that, but prices have dropped for eight straight days, their longest losing streak in more than seven years, as U.S. shale production has outrun demand and inflated stockpiles, according to Bloomberg News’s Naureen S. Malik. Government data Thursday showed a triple-digit gain in inventories last week, the biggest increase since 2015 for this time of year. The rout comes as a key Permian Basin pipeline starts up, inundating the market with gas extracted as a byproduct of soaring crude output in the biggest U.S. oil patch. While lingering heat has kept air conditioners running, boosting gas demand for power generation, the price slump is poised to deepen as the weather cools in October, Malik reports.

MEXICAN DOVES IN HAWKS’ CLOTHING

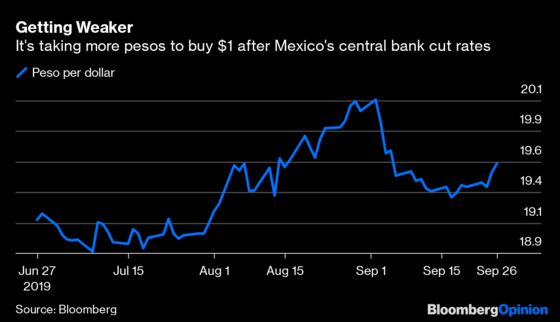

Few central banks topped the Fed in recent years in terms of hawkishness. One was the Bank of Mexico. It raised interest rates 15 times between the end of 2015 and the end of 2018. The Fed, by contrast, boosted rates nine times in the same period. Mexico’s central bank had every reason to be cautious. The nation’s inflation rate jumped to more than 6% in 2017, and policy makers didn’t want runaway prices to wreck its economy like it has historically done to so many other emerging markets. The hawkishness worked, and the inflation rate has since come down to 3%, allowing the central bank to cut interest rates on Thursday for the second time since early August, to 7.75%. And even though the central bank said the risks for the economy remain biased toward slower-than-expected growth, it stopped short of projecting a further easing of monetary policy. Currency traders, though, are expecting more rate cuts. They pushed the peso lower for a second straight day, making it one of the biggest losers in emerging markets. The median estimate of economists and strategists surveyed by Bloomberg expect the peso to weaken to 19.75 per dollar by year-end, and to 19.90 in the first quarter, compared with a recent 19.6534 per dollar in Thursday trading.

TEA LEAVES

Reports this week have painted a mixed picture of the economic health of U.S. consumers. On one hand, the Conference Board’s consumer confidence index for August fell the most since December. On the other, new home sales for August rose more than forecast. A government report Friday on personal income and spending for August may help tip the balance one way or the other. Economists surveyed by Bloomberg estimate real spending, or expenditures after inflation, rose 0.2% last month after jumping 0.4% in July, according to the median forecast. If spending comes in as expected, it would be in line with the average of the last five years, so neither hot nor cold. Pull back the curtain, though, and you’ll see that the recent strength in consumer spending appears to be coming out of savings, according to Bloomberg Economics. The personal savings rate stood at 7.7% in July, down from 8.8% in the beginning of the year. Although the current savings rate is still above its four-year trailing average of 7.3%, “dwindling savings suggest the robustness of consumers may be living on borrowed time,” a team of economists with Bloomberg Economics wrote in a research note.

DON’T MISS

Repo Meltdown Shows Budget Deficit Has Limits: Brian Chappatta

This Flight From Global Risk Has an Unhealthy Look: John Authers

There’s Plenty of Room at the Hotel Permania: Liam Denning

The Siren Song of Private Equity Grows Ever Louder: Mark Gilbert

Trump's Trade Policy Is 200 Years in the Making: David Fickling

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.