The Hedge Fund Roller Coaster Ride Got Even Wilder Last Year

(Bloomberg Opinion) -- It’s time to bury three myths about the hedge fund industry. First, that any investor can tell in advance which manager will produce superior returns. Second, that active management outperforms in volatile markets. And third, that the most popular funds are more loss-proof than their smaller rivals.

In aggregate, hedge funds had a great 2020. Hedge Fund Research estimates assets under management reached a record $3.6 trillion by the end of the year, boosted by surging asset values and net inflows that added $290 billion in the fourth quarter. For the industry’s customers, though, returns depended greatly on which particular manager their money was with — with the range of potential outcomes at its widest in more than a decade.

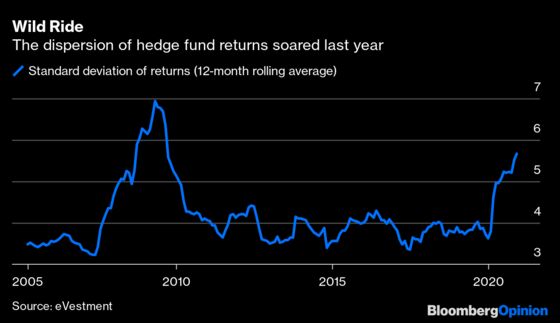

Hedge funds delivered average gains for investors of a bit more than 11% last year, their best performance since the tumultuous markets of 2009 enabled them to generate more than 19%, according to industry research firm eVestment. At the same time, the volatility of overall returns within the industry — the standard deviation from the mean — climbed to its highest since September 2008.

So while the overall picture is one of double-digit gains, the experience of individual investors varied wildly. As in any other year, it would have been impossible to know in advance which portfolio manager would have been above, below or in line with the industry average. But the cost of getting that selection wrong was particularly acute last year.

Moreover, not only did the most popular hedge funds as measured by size underperform the broader industry, they also delivered widely divergent results. The eVestment data shows that the ten biggest funds it collects data from — all of which have assets of about $20 billion or more — delivered average returns that were less than a third as good as the broader hedge fund universe in 2020.

Since 2015, the top 10 by size has only outpaced its peer group during years when the industry as a whole lost money — useful, I guess, but not exactly what clients are seeking when they allocate capital to an alpha-chasing strategy.

Those aggregate numbers mask an even broader dispersion than usual for the largest portfolio managers last year. Only one fund within the top ten by size was close to that average return, one had a gain of almost 30%, while the biggest loser suffered losses of more than 30%. The numbers “are among the worst and the best I’ve seen them produce,” Peter Laurelli, eVestment’s global head of research, told me. “There were more large funds with double-digit gains and double-digit losses than not in 2020.”

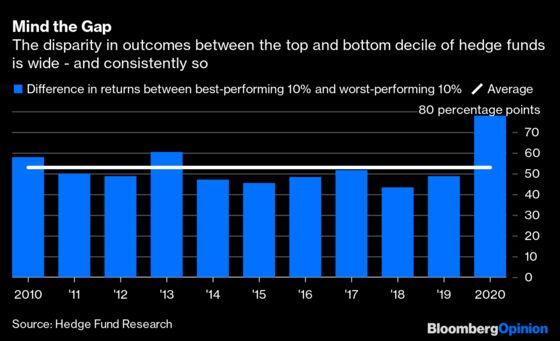

In the first quarter of last year, which includes the March market turmoil that roiled prices as the scale of the pandemic started to become clearer, the difference in the returns generated by the top-performing decile compared with the worst-performing slice soared to more than 56 percentage points, according to Hedge Fund Research. The top group made more than 15%, while the bottom of the pack lost almost 41%. The increased volatility that hedge fund traders have been wishing for didn’t smooth returns for their clients.

What’s interesting, though, is how persistent that differential has been. For the past decade, it’s averaged almost 53 percentage points, and year after year, it’s been close to that mean gap. And last year, the chasm exploded to 78 percentage points.

So while the standard deviation for the hedge fund industry as a whole was relatively benign for the decade until last year, the cleft between the top and bottom 10% has remained monotonously high.

That yawning average gap illustrates the difficulty investors face in choosing a hedge fund to manage their cash. Pick a manager who made it into the top 10 by performance in the second quarter of 2020, for example, and you’d have made more than 41%. A laggard in the bottom decile would have cost you more than 9%. As I wrote earlier this month, you pays your money and you takes your choice. But be prepared for a wild ride.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2021 Bloomberg L.P.