(Bloomberg Opinion) -- “Some modest tightening of monetary policy over the forecast period is likely to be necessary” was how the Bank of England worded the forward guidance at its quarterly review on Thursday. It sounded like tough talk. Indeed, the BOE is the first of the major central banks to set out a template for reducing stimulus, with parameters for when the flow of quantitative easing will stop, when the balance sheet will be allowed to naturally taper — and even when it will be actively sold down.

But, in reality, the BOE is playing for time. What Governor Andrew Bailey has done is set out his shop stall for others to peruse. The others being fellow central bank chiefs preparing for their annual conference at Jackson Hole, Wyoming from Aug. 26 to 28. They are just as focused as Bailey on how markets and economies will respond when they finally have to roll back their own stimulus programs.

Among them is Fed Chair Jay Powell, who has one eye carefully focused on his own reappointment for a second term, a decision that is due from the Biden administration in the fall.

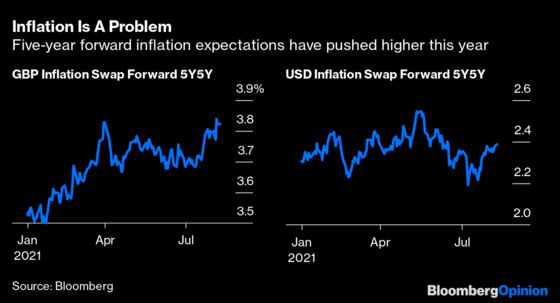

With U.S consumer inflation running at a 5.4% annual pace, there has to be a Fed contingency plan if the economy continues to run super hot. A near-1 million job gain in July non-farm payrolls released on Friday, shows recovery momentum is still impressive. It seems a touch crazy then that the Fed is still adding $120 billion monthly (a third in mortgage-backed bonds) to a balance sheet in excess of $8 trillion, especially as U.S. house prices (and perhaps even more significantly rents) are rising at the fastest pace in over 30 years.

With the European Central Bank and the Bank of Japan lagging in the rear-view mirror, it is incumbent on the Fed and BOE to run reconnaissance on how and when it is prudent to reverse stimulus. Unfortunately, the Fed still has nightmares about the May 2013 Taper Tantrum that caused a credit crunch and saw a lot of hard work unwound.

Yet persist they must as a loss of inflation-fighting credibility is a risk no central bank can toy with. Despite recent comments from Powell focusing on the still-high levels of underemployment, the Fed really can't wait until all the pandemic economic effects are nullified. Employment is a lagging indicator, and by the time it returns to pre-pandemic levels, you won’t be able to push the inflation genie back in the bottle.

Realistically, no one wants to tinker with liquidity in the system (code for maintaining the stock as well as the flow of QE) until after a mini-rate hike is tried out. From there it’s all in the sequencing between when interest rates rise and when QE is gently rolled back. It needs to be a harmonious blend.

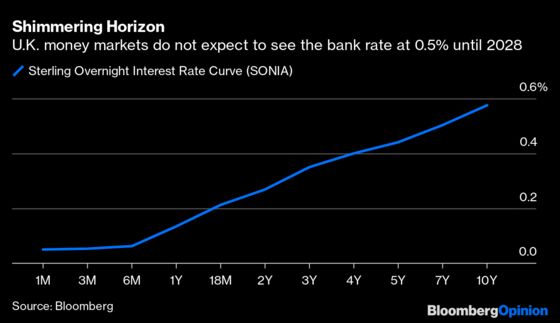

The BOE’s balance sheet of 895 billion pounds ($1.2 trillion) is the equivalent of 40% of gross domestic product and proportionally the largest of the big four central banks. A quarter of its holdings will mature between now and end-2025 but all these (and coupons) will continue to be fully reinvested until the official bank rate of 0.1% is lifted to 0.5%, according to the new guidance. Yet the money markets are not pricing for any rate hike for at least a year and not until 2028 to half a percent, so it maybe several years before the balance sheet is meaningfully reduced, as Bailey suggested last year. It is quite the disconnect between hawkish rhetoric and dovish reality.

Moreover, Deputy Governor Ben Broadbent was keen to distinguish between letting the balance sheet drift lower when 0.5% is reached and the seismic effect of actively selling Gilts when the bank rate reaches 1%. That will require additional unquantified measures to have been achieved. So real tapering is still but a twinkle in the central banker’s eye.

Indeed, after the BOE’s guidance and its auguries of tapering, U.K. government bond yields barely budged. That’s because of persistent market expectations that central banks will find it nearly impossible to either raise interest rates meaningfully — or ever kick the QE habit. Still, the response may provide data points for central banks as they test their way forward. Bailey has shown a possible way which the Fed can finesse.

Playing theoretical games that have no practical consequences may suit the Fed as much as the BOE but it is vital to signal that central banks have a measure of control — even if it can be drawn out as a way to tamp down rampant inflation. The market doesn’t really care how strong the economic data might be — just how the Fed reacts.

It is going to be hard to wean central bankers everywhere off their policy fix of choice but, at the very least, Jackson Hole has to set out a realistic timetable. Getting it right in the market’s eye is more important than securing a second term for Powell. But both, if handled neatly, could be compatible. He may have his fellow central banker Bailey to thank for shining a light.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2021 Bloomberg L.P.