(Bloomberg Opinion) -- The European Central Bank has been at the forefront of the euro zone’s economic response to the Covid-19 crisis. As political leaders scramble to conjure up a joint fiscal response, the central bank’s governing council can afford to stand still when it meets on Thursday.

Since the pandemic in Europe appears relatively contained, some central bankers may find it tempting to discuss when and how to begin withdrawing emergency stimulus measures. President Christine Lagarde should ignore such suggestions: The ECB has to continue supporting the economy and be ready to do even more if needed.

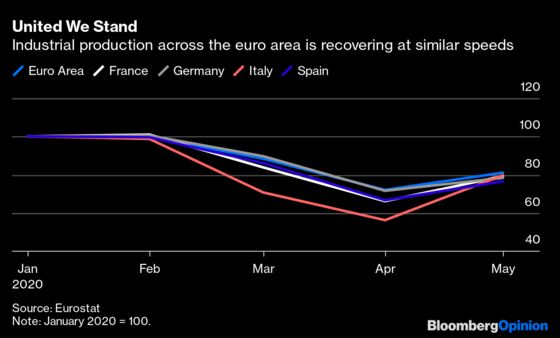

The outlook in the euro area is somewhat less gloomy than it appeared just a few weeks ago. Unlike other parts of the world, including the U.S., member states have managed to reopen their economies without triggering a second wave of infections. A string of encouraging indicators, including rising industrial production and retail sales, point to an economic rebound. The uptick is being seen across all member states, assuaging fears of a two-speed recovery: fast in some countries, such as Germany, slower in others, including Spain and Italy

These signs will strengthen the voices of those who are fearful of the side effects of the ECB’s recent interventions, which include launching a 750 billion euro ($855 billion) program of bond purchases and then expanding it to 1.35 trillion euro; relaxing its buying criteria so that it can direct its firepower where it is most needed; and offering a very generous lending scheme for banks.

In particular, Jens Weidmann, president of Germany’s Bundesbank, has expressed concerns that deviating from the standard rules for allocating purchases may offer governments the wrong incentives. Isabel Schnabel, a member of the executive board from Germany, has said the ECB could buy fewer bonds than anticipated.

Still, the ECB would be wise to err on the side of caution and delay any discussion on its exit strategy. The health situation remains precarious: While most countries appear to be successfully containing the virus through a strategy of local lockdowns, there is a growing fear over cases being imported from other countries where the pandemic is still raging.

There are also questions over how fast exports can rebound so long as the outlook abroad remains uncertain. Governments across Europe are shielding the labor market through unprecedented furlough schemes, but domestic demand is bound to suffer when this support ends. And it is unclear how ambitious the deal over the “recovery fund” European leaders are set to negotiate over the weekend will be, given the divisions between member states.

Given all this, it is very unlikely that inflation will return close to the ECB’s target of just below 2% anytime soon.

After a shaky start, the ECB has given the euro zone all the help it needs to mitigate a catastrophic downturn and maintain financial stability. However, the recovery is still in its infancy, and numerous threats to it remain. Lagarde shouldn’t give in to the overly optimistic. It’s best to be content with staying the course.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ferdinando Giugliano writes columns and editorials on European economics for Bloomberg View. He is also an economics columnist for La Repubblica and was a member of the editorial board of the Financial Times.

©2020 Bloomberg L.P.