The Secret to the Trump Economy? More Government Spending

(Bloomberg Opinion) -- As you’ve probably heard, House Democrats have cut a two-year budget deal with Senate Republicans and President Donald Trump to suspend the federal debt ceiling and increase federal spending by $320 billion. The debt ceiling is an arbitrary and possibly counterproductive construct, while the spending increases aren’t all that big if you assume that inflation will continue at about 2% a year, and may not even represent increases in federal spending’s share of gross domestic product. Long-run concerns about the burgeoning federal debt left aside — since almost everybody seems to be leaving them aside these days — this seems like a reasonable enough deal.

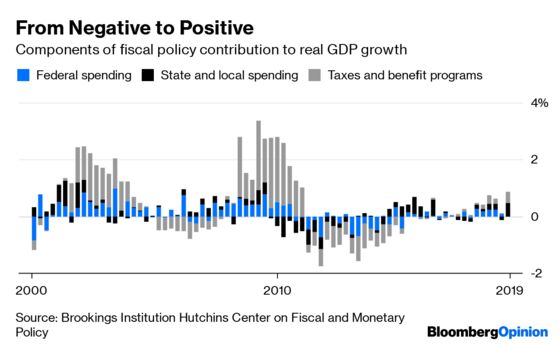

It’s a big contrast, though, from what happened in budget negotiations during the six years of this economic cycle when Republicans ran the House of Representatives and a Democrat was in the White House. From 2011 through 2016 there were repeated threats of a debt default due to House Republican opposition to raising the debt ceiling, and budget sequestration that helped bring on a three percentage point decline in federal spending’s share of GDP. Coupled with belt-tightening at the state and local level, this resulted in an impact on real GDP growth of negative 0.5 percentage points a year, according to the quarterly fiscal impact calculations of the Brookings Institution’s Hutchins Center on Fiscal and Monetary Policy.

Since Trump took office, fiscal policy has by contrast contributed an average of 0.3 percentage points a year to GDP growth. That represents a 0.8 percentage point shift. Meanwhile, the average real GDP growth rate has risen from 2.1% a year during those six years to 2.8% since the beginning of 2017, a difference of 0.7 percentage points. Coincidence?

My numbers here are a little dodgy — because it’s all I could do with the available data, I simply averaged quarterly GDP growth and fiscal impact estimates rather than calculating compound annual growth rates — and government spending probably doesn’t translate quite that directly into economic growth. But with the president and his supporters claiming variously that tax reform, deregulation, and/or tougher trade policy has generated the acceleration in economic growth, it does seem like we ought to be giving more credit to the shift from relative austerity to fiscal easing on Capitol Hill. “It’s often overlooked,” economist Mike Madowitz of the left-leaning Center for American Progress declared on Twitter after the budget deal was announced, “but the biggest economic improvement since Trump took office is more government spending.”

Also noteworthy are the asymmetric politics of this shift. Economist Daniel Altman wrote a 2012 manifesto about House Republicans’ deficit hard-lining titled “Sabotage: How the Republican Party Crippled America's Economic Recovery.” Since 2016, by that reasoning, the sabotage has stopped — and the economy has improved.

Is that a fair characterization? I don’t doubt that many House members elected in the Tea Party wave of 2010 truly thought they were helping the economy by trying to bring federal spending down. Moreover, former House Tea Partier Mick Mulvaney keeps proposing cuts as director of the White House Office of Management and Budget and spending-averse hard-line Republicans could conceivably still torpedo the current budget deal. But Congressional Republicans’ overall loss of interest in deficit reduction after Trump’s inauguration does seem to indicate that partisan calculations were paramount. House Democrats, meanwhile, have far less ideological reason to oppose increases in government spending. But their unwillingness since taking charge in January to play hardball on legislation that might endanger the ongoing expansion also seems to bespeak a different attitude toward partisanship and macroeconomic policy. House Republicans were willing to hold the U.S. economy hostage for partisan advantage. House Democrats have not been.

In 2012, Joe Weisenthal, now a colleague of mine at Bloomberg News, argued repeatedly that electing Republican Mitt Romney president would be good for the economy in large part because it would lead House Republicans to stop trying to cut federal spending. Given the evidence of the past couple of years, you’d have to say he had a point. Now that Democrats have control of the House, and seem likely to maintain it after the 2020 elections, the choice on these grounds seems less stark. Whomever Americans elect as president in 2020, federal spending will keep going up.

At some point I would guess that the returns to fiscal stimulus will begin to diminish and possibly even turn negative, and the trade-offs discussed here will change. Given how wrong deficit hawks have been in their predictions in recent years, though, there’s no way I’m going to try to put a date on that. For now, this is our economic and political reality.

For GDP, for which the necessary data is available, compound annual real growth was 1.7% in Obama's last six years in office and 2.8% so far in Trump's term.

To contact the editor responsible for this story: Sarah Green Carmichael at sgreencarmic@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Justin Fox is a Bloomberg Opinion columnist covering business. He was the editorial director of Harvard Business Review and wrote for Time, Fortune and American Banker. He is the author of “The Myth of the Rational Market.”

©2019 Bloomberg L.P.