(Bloomberg Opinion) -- If every leveraged-loan and high-yield bond deal is “cov-lite,” then none is.

This line of reasoning, loosely inspired by “The Incredibles,” might be how investors have to start thinking about the riskiest corners of the debt market. “Cov-lite,” a catch-all term for weak or nonexistent creditor protections known as covenants, has long been a popular buzzword among those concerned about excessive corporate leverage and how the leveraged-loan market has roughly doubled in size to $1.2 trillion just since 2012.

For money managers, the proliferation of cov-lite deals is an easy target — who could dispute that fewer safeguards is an overall negative development for investors? Indeed, I wrote a column last month that highlighted some of the phrases used recently to describe risky debt, ranging from “dangerous and aggressive” to “abuse of documentation.” Seemingly day after day, news articles question whether the leveraged-loan market is overheated, using the growing share of cov-lite issues as proof.

By now, though, it should be clear that the proverbial genie is out of the bottle with regards to looser bond and loan covenants. As long as those keeping score of investor safeguards don’t move the goalposts, a vast majority of deals seem certain to earn the cov-lite moniker.

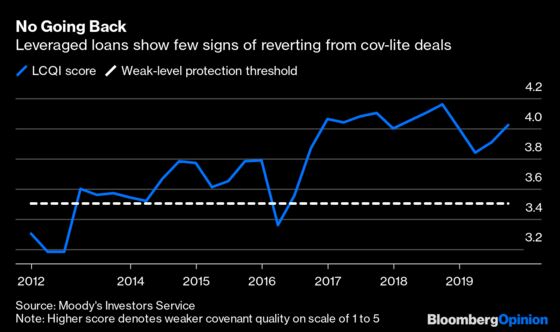

Moody’s Investors Service released a fresh batch of “covenant quality indicator” reports that back this up. In high-yield bonds, the rating company’s CQI remains pinned near its worst level ever. The gauge rates certain investor protections on a scale of 1 to 5, with 5 representing the most flagrant disregard of covenants. Overall, the junk-bond market scored a 4.48 in January. In leveraged loans, the overall CQI was 4.02 in the third quarter of 2019, the weakest since the all-time worst score of 4.16 a year earlier.

If there were ever a time for loan covenant quality to improve, it should have been the third quarter. U.S. leveraged-loan funds experienced 43 consecutive weeks of outflows between November 2018 and mid-September 2019, according to Refinitiv Lipper. The S&P/LSTA Leveraged Loan Price Index fell in the three-month period as fears of a recession escalated, which in theory would have given investors an opportunity to extract more favorable terms. In May, at the Milken Institute Global Conference in Beverly Hills, big investors declared they were coming up with ways to fight back against weakening covenants. What happened? It certainly wasn’t a change in fund flows.

The market moves didn’t go unnoticed by Moody’s. “The weakening protection is all the more striking because it continued even as volumes declined and spreads widened from Q2 to Q3,” analysts Derek Gluckman, Enam Hoque, Evan Friedman and Christina Padgett wrote. “Normally, covenant protections would improve in such market conditions. But the findings suggest that risks are increasing and that while investors are voicing caution, they are not effectively pushing back on permissive covenant terms.”

This suggests that investors, who seek the strongest possible protections, have lost the battle with companies, private-equity firms and their lawyers, who aim to cram in as many favorable terms as possible. Covenant Review, an independent research firm that analyzes debt documents for investors, is among those who have valiantly pushed back against the trend toward looser safeguards. But even it acknowledged in its 2019 year-in-review that documents have become so loaded up with offensive covenants that few deals are ever fully scaled back to what they looked like several years ago.

All this is to say, it’s too simplistic for investors to say they’re staying away from cov-lite deals. If anything, clinging to the few deals that still have strong covenants might somewhat counter-intuitively increase the risk of losing money.

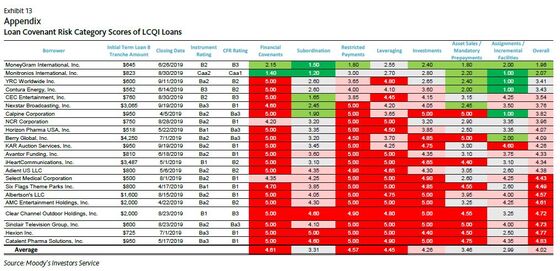

Among the loans listed by Moody’s in its report, only two managed to avoid receiving the worst-possible score of “5” in at least one of the seven categories assessed by the credit rater. Those were MoneyGram International Inc. and Monitronics International Inc. MoneyGram took more than a month to finalize its deal after price talk, paying an extra 50 basis points over the London Interbank Offered Rate compared with where it was set to price initially. The financing also included a second-lien secured term facility that will pay 13% a year, according to Moody’s. Monitronics emerged from Chapter 11 bankruptcy on Aug. 30. As part of that process, $823 million of its term loans were converted into a new facility.

Those don’t sound much like thriving companies, even if the head of Monitronics contended it “emerged as a stronger, more focused organization.” Certainly, risk comes with the territory of investing in junk bonds and leveraged loans. But these are some of the worst-rated securities, and the strongest covenants only go so far when an issuer is in deep distress. By contrast, a better-situated company may have the weakest safeguards but never actually put them to the test.

This is the trade-off that investors have to get used to. Sure, they would be smart to raise a fuss if a borrower tries to sneak unprecedented favorable terms into a deal. But for better or worse, these markets have shown that once one a company sails through the market with weakened covenants, many others will attempt to do the same — and probably succeed.

If and when the credit cycle turns, the aggressive push toward weakening protections virtually ensures that recovery rates will be worse than in 2008, as Moody’s has predicted. But there’s no going back now: The risky debt markets are full of cov-lite deals. Investors either have to acclimate to that reality or get out of high-yield and leveraged loans.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.