(Bloomberg Opinion) -- Time to bag that sunlounger – all of the European bond market’s obvious barriers to a peaceful summer holiday have been removed.

Dovish central bank ready to cut rates again and restart QE? Double-tick. Political headaches? All removed (before you say “Brexit,” remember that Prime Minister Boris Johnson’s deadline for withdrawal is Oct. 31. That’s months away).

Greece now has a majority center-right government after the populist Syriza party fell from power. The reward is the drop in its 10-year yield below that of the equivalent U.S. Treasury bond. The handover of top European Union jobs has been completed. It’s nice to have some certainty on both these sticking points.

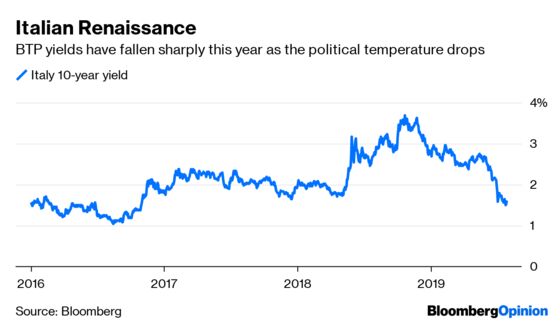

What really helps is that Italy has settled, for now, its budgetary dispute with Brussels. Of course that is largely because the impending recession in Europe makes haggling over 2 billion euros ($2.2 billion) seem futile.

But equally, the 2020 budget approval process is not about to be derailed by a snap election. Italian Deputy Prime Minister Matteo Salvini had been on the verge of quitting the government, claiming that key policies of his League party weren’t getting through. But now that coalition partner Five Star Movement has been made to swallow its environmental objections to building a rail link with France, something Salvini had long wanted, the partnership looks like it will last a little while yet.

An Italian election over the summer would have turned markets into a completely different ballgame, if the sharp selloff when the current populist government took power in May 2018 is any guide. It would totally disrupt the budget process, irritate Brussels, and introduce so much volatility into Italian yields that other risk markets would come under pressure.

Instead it’s ice cream all round and in theory every reason to load up further on bonds that yield something. Anything.

So where are the logical places left to look for some decent carry, in a world where even some short-dated junk-rated bonds have turned negative? Longer maturities are not necessarily the answer. Though longer duration bonds yield more, there is increasingly scant reward for the considerably higher risk.

Italy is the only large liquid government market in Europe with any juice left – 10-year bonds yield around 195 basis points more than equivalent German debt. That’s far more than what’s on offer from less liquid European alternatives, such as Spain, which now has a spread of about 74 basis points.

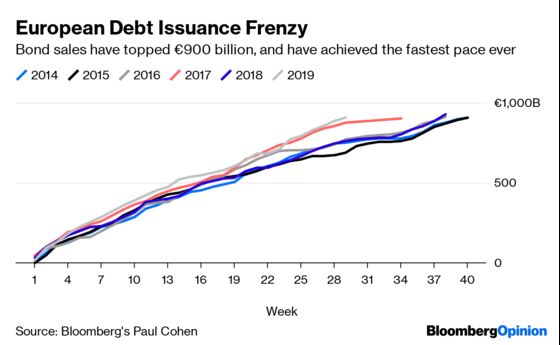

The other logical alternative is the euro-denominated credit markets. It has been a banner year for corporate, supranational and financials issuance. The 900 billion euro-mark ($1 trillion) has been reached at a record pace, two months earlier than last year. It is also notable that 344 billion euros of this, or 38%, has been from maturities of 10 years or longer, compared to 33.7% for the same period in 2018. These are classic symptoms of a desperate dash for yield, and it’s fair to ask how long it will last.

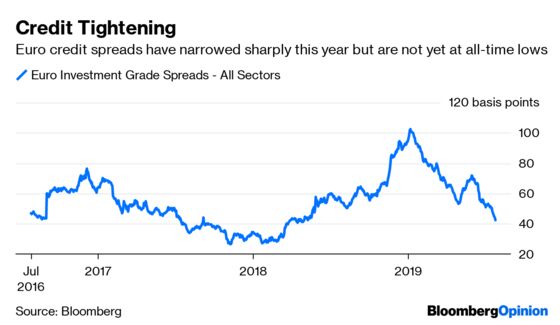

But it isn’t obvious what would prevent spreads from tightening even further. Even though euro-denominated investment grade corporate credit spreads have more than halved this year, the market still has room before touching the record lows of November 2017, when the European Central Bank’s corporate bond buying QE program was in full flow. It has even more chance of getting there now that President Mario Draghi has promised to restart stimulus.

Normally credit spreads should widen if the euro-area economy is struggling, which it clearly is. But as the majority of liquid European government bond market yields are negative, investors have little alternative if they want to produce any kind of return. At least it’s not so bad if the ECB has your back.

But this is dealing with the known knowns and there is no accounting for the unexpected. As the mixed reaction of the euro to Draghi's press conference Thursday shows, investors have limited patience to wait for extra central bank action. This is all the more so now that, just as Draghi was calling for fiscal stimulus to take the emphasis off monetary measures, German Finance Minister Olaf Scholz ruled it out.

Given what the market can see, it could almost be said to have reached nirvana. But once you achieve nirvana, where is there left to go? That's probably September's business. In the meantime, don’t forget the suncream.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.