(Bloomberg Opinion) -- The third-quarter gross domestic product number is coming out Thursday morning, and it’s going to be huge. The median of the economic forecasts collected by Bloomberg calls for a 29.9% annualized real GDP gain.

This would be the biggest quarterly GDP gain on record, with the previous high of 16.7% set in the fourth quarter of 1949. Quarterly GDP data are only available back to 1947, and it seems likely going by the annual data (which are available back to 1929) that there were several quarters during World War II with annualized growth of 30% or more. Still, 29.9% would be a big deal.

It would not mean, however, that the economy grew 29.9% in the third quarter. The actual change would be 6.8%. It would also not mean the U.S. economy is almost back to where it was before the second quarter’s 31.4% annualized GDP decline. In fact it would take a 45.7% annualized quarterly gain to wipe out the second-quarter loss.

This all can be a bit confusing, and when the GDP numbers come out on Thursday, lots of political hacks, some journalists and even a few financial professionals may jump to incorrect conclusions about what the percentages mean. If the annualized growth rate comes out ahead of consensus and tops 31.4%, for example, we will surely hear lots of claims that the third-quarter gain has wiped out the second-quarter decline. In the interest of heading off at least a few such erroneous assertions, I hereby offer some simple(ish) math.

The first issue is that the Bureau of Economic Analysis, unlike its counterparts in other countries, reports quarterly GDP changes at an annualized pace. When it reports GDP grew 2% in a quarter, it’s actually saying GDP grew at a pace that, if sustained for a full year, would result in 2% annual growth. When GDP is in fact growing at a 2% annualized pace, you can get a close-enough approximation of the actual quarterly change just by dividing the number the BEA puts out by four. At 29.9% annualized growth it’s more important to do the proper calculation, which in this case involves taking the fourth root of 1.299 (1 plus 29.9%) and then subtracting 1. That gets us to 0.068, or 6.8%. The 31.4% annualized decline in the second quarter, meanwhile, comes out to a 9.0% drop.

The other issue is that percentage changes imply different amounts on the way up than on the way down. If you invest $100 in something and it loses 50% of its value, then you’re down to $50. If it then goes up 50%, that only gets you back to $75. This should be obvious to all of us, but it isn’t exactly intuitive. Here’s how it works out with second- and third-quarter GDP: A 31.4% annualized GDP decline in the second quarter followed by a 29.9% annualized GDP increase in the third quarter would add up to a 2.8% non-annualized drop in GDP. A 31.4% decline followed by a 31.4% annualized increase would add up to a 2.6% decline.

The economy actually started shrinking in the first quarter, so a 29.9% annualized third-quarter increase would leave GDP 4.1% short of its fourth-quarter 2019 peak. A 31.4% increase would leave it 3.8% short. Just for comparison, the peak-to-trough GDP decline in the Great Recession was 4%.

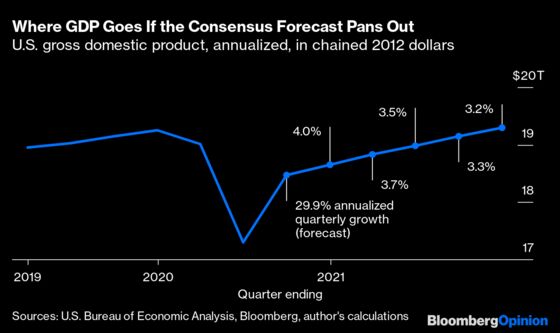

It may be a little easier to take this in visually. Here’s real GDP and annualized quarterly growth as reported by the BEA through the second quarter of this year and according to the Bloomberg median forecast (as of Tuesday) after that. If the median forecast is right, the economy will finally surpass the fourth-quarter 2019 GDP peak in the fourth quarter of 2021.

All of these numbers are subject to revision in coming years as the BEA collects more data, and this year’s second and third quarters will probably be subject to especially large revisions given how abnormal both were. Maybe we’re closer to pre-pandemic GDP numbers than we think. Maybe we’re farther away. But let’s at least try to get the math right on the numbers we’ve got.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Justin Fox is a Bloomberg Opinion columnist covering business. He was the editorial director of Harvard Business Review and wrote for Time, Fortune and American Banker. He is the author of “The Myth of the Rational Market.”

©2020 Bloomberg L.P.