(Bloomberg Opinion) -- Heh. Come on. Really?

Year over year, positive impacts from volume growth, regulatory credit revenue growth, gross margin improvement driven by further product cost reductions and sale of Bitcoin ($101M positive impact, net of related impairments, in “Restructuring & Other” line) ... [Emphasis mine.]

You might be surprised to learn that’s a snippet from the earnings report of a car manufacturer. But this is Tesla Inc.

Now, selling Bitcoin for a profit isn’t a bad thing on its face; better than making a loss, after all. Still, having that gain account for roughly a quarter of the entire net income of a — forgive the repetition — car company might be. You may recall Tesla only got into the Bitcoin game the very same quarter, announcing it would also start accepting the stuff for car payments. The latter was entirely irrelevant to taking a $1.5 billion crypto-punt, of course, which this “Restructuring & Other” line item only serves to confirm.

Ordinarily, a car company attributing a quarter of its profit to playing the digital slots would be a cause for concern. At the very least, an investor might put a 10x multiple on the regular profits but something much lower on the crypto-gain because of higher risk, volatility or so forth. Such considerations are perhaps moot when the company’s stock already trades at 600x trailing earnings.

Yet the Bitcoin gain helps to draw attention to the core issue here: elusive operating leverage.

Tesla tends to emphasize its automotive gross profit margin as the figure to watch: This quarter’s was a robust 25.8%, or 21.1% once you strip out the regulatory credits. Indeed, in absolute dollar terms, this was the biggest quarter ever for that margin, at about $2.25 billion. Vehicle deliveries also set a new record.

Somehow, though, this has no discernible effect on the bottom line. Strip out the Bitcoin gain, and Tesla’s adjusted net income was $337 million. That’s roughly the same as the third quarter of 2020, when Tesla reported $331 million — even though vehicle deliveries and revenue are 31% and 18% higher, respectively. Possibly, Tesla’s capacity utilization running below 70% even as it spends money on new factories may be a problem here.

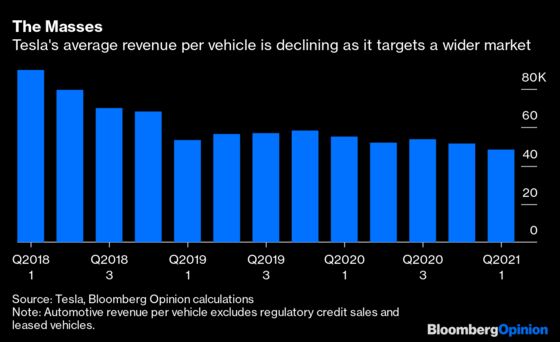

It also reflects the big drop in sales of Tesla’s higher-priced Models S and X as the company prepares to launch new versions. Even as those come back, though, the trend in average sales price of the company’s vehicles is downward. The investment case rests on Tesla growing faster (much faster) than margin-per-vehicle declines.

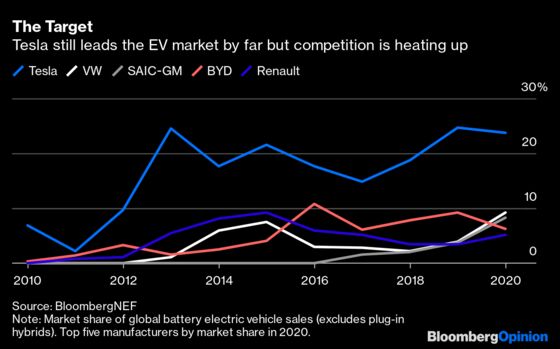

On that front, it’s worth noting Tesla’s revenue actually fell slightly, quarter over quarter. More importantly, there are signs of competitors finally starting to catch up in electric vehicles. For example, Tesla still led the global market by far in 2020, with a market share of about 24%. But that share actually fell while the share of Volkswagen AG, for example, jumped from 4% to almost 9%.

Tesla’s resort to price cuts on vehicles — autos marketing 101 — speaks to this competition. And as traditional manufacturers launch their own electric models, so their demand for Tesla’s regulatory credits should wane. Hence, rising competition presents a challenge to both the top and bottom line. That’s not an existential problem for a car company; moving metal by cutting into your margin is nothing new in this industry. But it is a problem if you have a market cap north of $700 billion and your margins are already thin and reliant on subsidies. On that basis, the odd Bitcoin windfall starts to look useful, if not downright necessary.

Tesla obtains various greenhouse-gas emissions credits due to selling zero-emission vehicles. It then sells these to other automakers who require them to offset their sales of traditional vehicles, with the proceeds effectively offering 100% margin.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2021 Bloomberg L.P.