Tencent Is a $43 Billion Headache for Its Biggest Backer

(Bloomberg Opinion) -- It’s one of the most successful investments of all time. The $32 million that Naspers Ltd. invested in China’s Tencent Ltd. in 2001 is now worth more than $200 billion. But the South African company may never be able to reap the full rewards of that bet, because the way that index investing works means Naspers is simply too big for its home market to swallow.

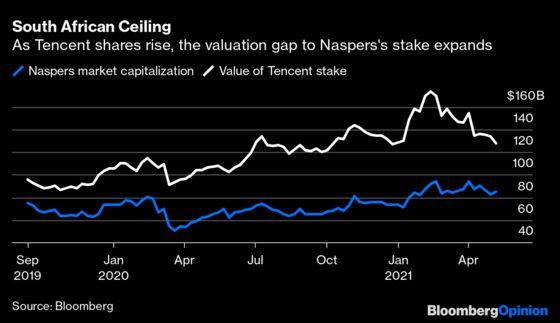

The stake in Tencent has made Naspers the largest constituent of the Johannesburg Stock Exchange, accounting for almost a quarter of the index’s weighting. That creates difficulties for large investors that track the index and often limit themselves to having just 12% of their portfolio in any one stock. Because whenever the Naspers share price increases, which it should in line with Tencent’s gains, it takes up more of their portfolios and they have to reduce their holdings.

All this keeps Naspers stock broadly flat even as its assets get more valuable. The shares consistently trade at a big discount to the value of its investments, not least the Tencent stake.

The conundrum has forced Chief Executive Officer Bob van Dijk and Chief Financial Officer Basil Sgourdos to find ever more creative ways of rejigging the capital structure in an attempt to reduce the discount. In 2019, they spun out the Tencent holding and other tech investments into an Amsterdam-listed subsidiary called Prosus N.V., where the two executives occupy the same roles. Naspers retained 73% of the new company, while curbing the discount — for a while, at least. Prosus’s $141 billion market capitalization makes it one of Europe’s three biggest tech companies.

The problem is, as long as Tencent continues to grow, Naspers will continue to get too big for South African investors. On Wednesday, van Dijk and Sgourdos made a new gambit, offering to let Naspers shareholders swap their stock for Prosus shares. The move is smart, as far as it goes: It gives Prosus a greater free float, and reduces the Naspers weighting on the Johannesburg exchange to about 14%. That should benefit both companies. Naspers shareholders retain just as big a stake in Prosus, even as Naspers itself reduces its economic interest in the Dutch firm.

But this again only looks like a temporary fix. Even at 14%, the weighting is still higher than the 12% concentration with which many investors are comfortable. Should Tencent’s share price recover, the discount on Naspers will surely expand again.

There’s not much more financial rejigging that van Dijk can do. The share swap will give Prosus 49.5% of Naspers stock. Any more than that and the change of control would land the companies with a hefty tax bill — one that could stretch into the tens of billions of euros. But should Naspers’s discount to the value of its holding in Tencent extend beyond its current $43 billion, ponying up the tax payment may be worth it.

At some stage, he may have to accept that realizing the full value of the investment may be impossible. Spinning the entirety of the Tencent stake into a standalone holding company might be an option.

For now, Van Dijk has managed to figure out a short term fix for his problem. Eventually he’ll need to think longer term.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2021 Bloomberg L.P.