(Bloomberg Opinion) -- For some time now the conventional investment wisdom has been that the global economy may be at risk of a slowdown, posing a threat to companies dependent on international markets. The major exception, this thinking went, was big technology companies, which have so much going for them that they were immune to any minor bumps in worldwide growth.

But now there's reason to believe both sides of that narrative have changed and that there's cause for optimism for global growth but pessimism for Silicon Valley. If that's right, it will mean some stock-market darlings are about to fall from favor while certain laggards suddenly outperform.

There are a variety of reasons why sentiment on industries tied to global growth could improve. The most significant is that although trade relations between the U.S. and China may not improve, there are no signs of further deterioration. Both countries appear to be signaling that they're trying to reach an agreement. With the U.S. presidential election now only a year away and President Donald Trump's favorability ratings slipping amid impeachment inquiries, he may not be willing to risk further escalation. That could make 2020 the first year since 2017 without trade tensions weighing down global growth.

The second is that central banks no longer seem to be behind the curve in responding to trade tensions and slowing global growth. The Federal Reserve is poised to deliver its third interest-rate cut of the year on Wednesday, joining most central banks around the world in lowering borrowing costs. For much of the past year, part of the concern about recessionary risks was tied to fears about the yield curve inverting; when longer-term interest rates fall below short-term interest rates, it often signals impending recession. But thanks to the Fed's rate cuts and reduced trade tensions, the inversion has subsided. We entered 2019 worried about the drag from rate hikes and a flattening yield curve; now we could enter 2020 anticipating a boost to growth from rate cuts.

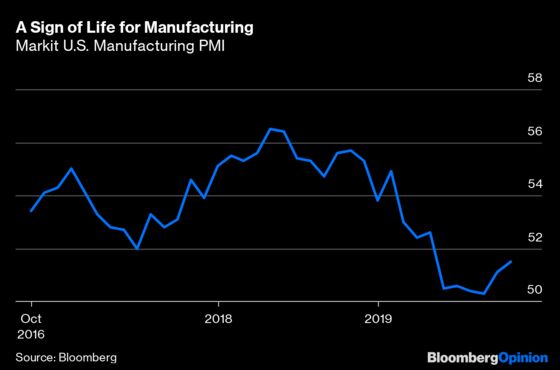

Finally, there's the possibility that manufacturing has bottomed. Two different measures of manufacturing sentiment have given conflicting signals during the past few months. The Markit PMI gauge of sentiment in October had its second straight monthly increase, rebounding from the lowest in at least three years in August.

The more widely followed ISM Manufacturing survey in September reached the lowest level since the Great Recession ended, but there's hope that on Thursday it will confirm what the Markit and other regional manufacturing surveys have shown. The end of the United Auto Workers strike against General Motors Co. should provide a boost to manufacturing activity next month as well.

Although conditions seem to be improving for manufacturing, the same cannot be said for high-flying tech companies. In its third-quarter earnings report, Netflix Inc. reported disappointing U.S. and overseas subscriber numbers while Walt Disney Co. plans to introduce a competing video-streaming service next month. Amazon.com Inc. reported continued slowing growth for its Amazon Web Services cash cow, while profit margins are getting squeezed by spending on shipping as it pushes more one-day delivery service to customers to sustain growth in its e-commerce business. Twitter Inc. also reported a disappointing third-quarter performance because of weak ad revenue, while Google parent Alphabet Inc. on Monday reported earning that fell short of analysts’ estimates after the market closed. Meanwhile, the threat of regulation and antitrust looms over the industry.

Nor have investors been enthusiastic about the newly public tech companies, such as Uber Technologies Inc., Snap Inc. and SmileDirectClub Inc. The failed initial public offering of WeWork parent We Co. will add to the pall -- at least for several quarters, as the company cuts costs by laying off thousands of people. That could echo throughout the industry, potentially depressing spending on everything from catering to office space to software to online advertisements. Stocks that now are expensive by normal valuation benchmarks could be hurt.

With the Standard & Poor's 500 Index breaching its all-time closing high on Monday, investors will be wondering what can drive further gains. For the first time in a while, steering away from tech stocks and toward stocks that have suffered from the sluggish global growth environment may be the way to go.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Conor Sen is a Bloomberg Opinion columnist. He is a portfolio manager for New River Investments in Atlanta and has been a contributor to the Atlantic and Business Insider.

©2019 Bloomberg L.P.