(Bloomberg Opinion) -- Alan Jope’s efforts to instill purpose into the British heritage tea brand, PG Tips, have been all about bringing people together over a nice cup of tea. Now Unilever NV’s chief executive officer wants to cleave the tired tea business apart from the rest of the consumer giant.

He’s conducting a strategic review of the division, which also includes the Lipton and Pure Leaf lines, that could lead to a sale or partnership, and possibly even herald a broader exit from the group’s sluggish food business. Facing the slowest quarterly growth in a decade, even before any impact from the deadly coronavirus, Jope must improve performance at the company whose businesses range from Dove soap to Ben & Jerry’s ice cream.

Tackling tea, where demand has shifted away from the traditional black beverage to flavorful herbal options, is a good start. The unit, including its operations in emerging markets, generates annual sales of about 3 billion euros ($3.3 billion). Martin Deboo, an analyst at Jefferies, estimates it could be worth about 6 billion euros, assuming a multiple of two times sales.

Jope, a long-time Unilever veteran, should have scrutinized Unilever’s portfolio earlier in his tenure that began just over a year ago. But now that he’s finally grasped the nettle, he should go further. His predecessor Paul Polman sold the margarine and spreads arm in the wake of the $143 billion approach from Kraft Heinz Co. three years ago. But since then meaningful disposals in the division have stalled

The food and refreshments unit as a whole generates about 20 billion euros a year of sales, and could have an enterprise value of about 60 billion euros, according to Deboo. Selling it off would leave Unilever concentrated on the household and personal care businesses, which Jope previously oversaw, potentially lifting the company’s growth rate, and its valuation.

But such a chunky disposal would require a buyer with a big appetite. Kraft Heinz, already highly leveraged, would struggle. Private equity firms may be interested, but it would still be a large transaction, likely requiring more than one player to join forces.

So a more piecemeal approach looks sensible. Other disposal candidates beyond tea are dressings, with annual sales of of about 3 billion euros; savory sauces, stocks and food, including Pot Noodle, with revenue of 6 billion euros; and ice cream, which generates about 7 billion euros of sales. While still sizable deals, they are not impossible for a buy-out group to digest. As my colleague Chris Hughes and I have argued, food businesses may be expanding more slowly, but their stable cash flows can support borrowings, and there is scope to lift margins.

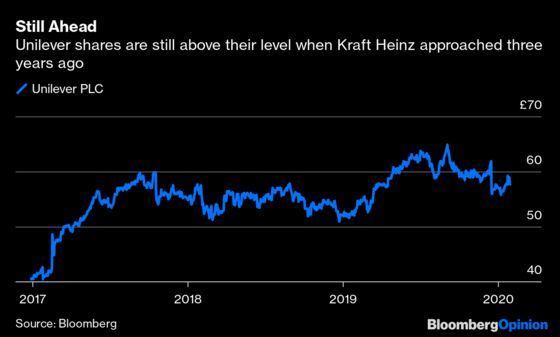

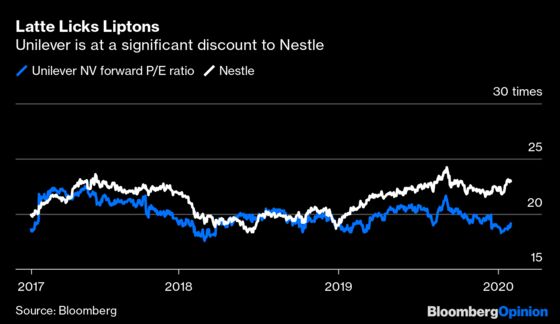

Unilever shares, which rose as much as 2% in London on Thursday, are still above their level at the time of Kraft Heinz’s bid in February 2017. But they are at a significant discount to rival Nestle SA. Its CEO, Mark Schneider, is already doing many of the things that Jope should, selling off underperformers for good prices and recycling the proceeds into focused acquisitions.

As I have long argued, Kraft Heinz isn’t in a position to come back. But an activist investor might be tempted to weigh in. At current valuations, the prospect of a breakup may be more appealing to a hedge fund than even a double cherry Magnum. So it would be good for Jope to share a brew with some willing private equity buyers. Otherwise he might find it’s an aggressive investor he’s bringing closer. That would make for a far less cosy cuppa.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2020 Bloomberg L.P.