Target Crammed a Year’s Worth of Growth Into a Quarter

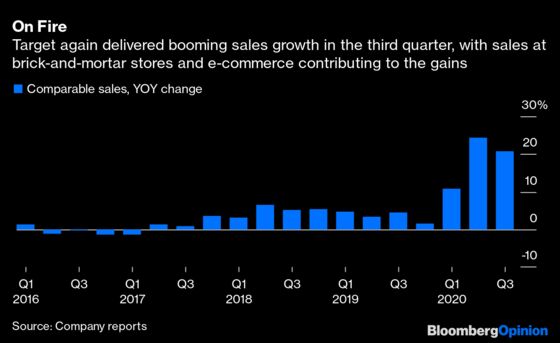

(Bloomberg Opinion) -- Target Corp. had a monster third quarter – both because of the pandemic, and in spite of it. The big-box retailer reported a blockbuster 20.7% surge in comparable sales, blowing past analysts’ expectations. The result reflected a 15.6% increase in average sales per receipt, as well as a 4.5% lift in transactions.

Just how big was Target’s quarter? Let’s put it in perspective. The retailer’s sales totaled $22.3 billion in the three months ended Oct. 31, a $3.9 billion increase from the same period last year. By comparison, the chain’s increase in sales for the entire preceding fiscal year was $2.7 billion. In other words, in the third quarter alone, it had to figure out how to manage the equivalent of a more than a year’s worth of growth. And that’s after experiencing a huge sales increase in the second quarter. It’s an utterly herculean operational lift — requiring a rethinking of supply chain, inventory management and labor models — and it bodes well for Target’s long-term prospects that it was able to adapt to these conditions so quickly.

In some ways, it’s logical that Target reported such strength given the ways the pandemic has upended shopping patterns. Consumers have been consolidating their store trips amid public health concerns, and Target, by carrying a wide array of merchandise, is well positioned to benefit from that pattern. The desire for one-stop shopping has likely pulled some grocery sales toward Target that would’ve otherwise gone to traditional supermarkets, and also helped it poach some sales of electronics and beauty products away from category specialists or small-format stores.

It also makes sense that consumers’ embrace of spending on home goods has given Target a boost. This area has long been a real strength for the retailer; its lineup of private label merchandise is much more stylish and well-priced than much of what is offered at department stores or Bed Bath & Beyond Inc. No wonder, then, that Target notched “mid-20%” comparable sales growth in its home category.

But if scoring sales in home goods was something of a layup for Target, its sales increase in apparel was more hard-fought. Comparable sales in this category jumped nearly 10% from a year earlier, a striking result when the clothing business overall has been battered by shoppers skimping on new outfits when they’re not regularly going to the office, the classroom or parties.

The pandemic, in theory, also could’ve been tough a break for Target because it has nudged so many shoppers online, and that channel accounted for a relatively small share of its business before the pandemic. But the retailer recorded a 155% increase in e-commerce sales, enabled by long-term investments in curbside pickup and same-day delivery that have it helped it grab more market share in this area this year.

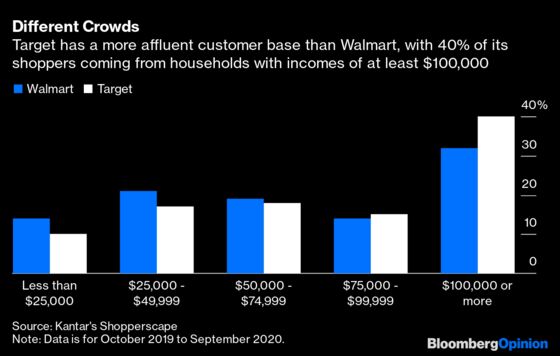

Both Walmart Inc. and Target have been riding high on the pandemic-fueled surge in grocery and general merchandise spending. Target’s comparable sales growth, though, has been the more turbocharged of the two. This may largely reflect the fact that Target has a somewhat more affluent customer base. According to Kantar’s Shopperscape, the average household income of a Walmart shopper was $78,262 in the period from October 2019 to September 2020, compared with $88,596 for Target.

Amid widespread job losses and uncertainty about additional stimulus support from the federal government, it makes sense that more affluent shoppers would be in a better position to trick out their backyards or spring for a new TV to make at-home living more enjoyable.

Target says it has added $6 billion in market share year to date across a variety of categories. The benefits to the retailer of making those inroads with consumers should outlast its pandemic boom.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Sarah Halzack is a Bloomberg Opinion columnist covering the consumer and retail industries. She was previously a national retail reporter for the Washington Post.

©2020 Bloomberg L.P.