Playing Second Fiddle to TSMC Gets a Standing Ovation

(Bloomberg Opinion) -- While the tech industry watches Taiwan Semiconductor Manufacturing Co. amid a global chip shortage, one of its neighbors has been a far better bet for investors.

United Microelectronics Corp. is a distant second to TSMC in the market for pure custom-manufacturing of chips in almost every measure: technology, capacity, revenue, margins. But in the metric that counts the most — share returns — the company has taken the crown. Its Taipei-listed shares have jumped more than 300% over the past year, double that of its rival. Both have done even better with their New York-traded depositary receipts.

This isn’t merely a sentiment-driven rally. UMC’s incredible runup comes in tandem with a vast improvement in earnings. Operating income climbed fourfold last year, despite a meager 19% increase in revenue.

The reason is deceptively simple. While TSMC spends in the tens of billions of dollars each year on capacity and equipment, its neighbor in the Hsinchu Science Park in north Taiwan remains deliberately tightfisted. This year’s planned capital expenditure illustrates the contrast — one company expects to dish out up to $28 billion, the other $1.5 billion.

Because of its significant gap in technology and capacity, UMC doesn’t get the cool clients with the best new chips, like Apple Inc.’s latest iPhone processors. But it doesn’t try. Instead, the also-ran is content with being a solid second-tier player offering older technology — as much as a decade behind TSMC — used in important but more mundane components, such as those that tune radio frequencies or manage power supply in mobile and consumer electronics.

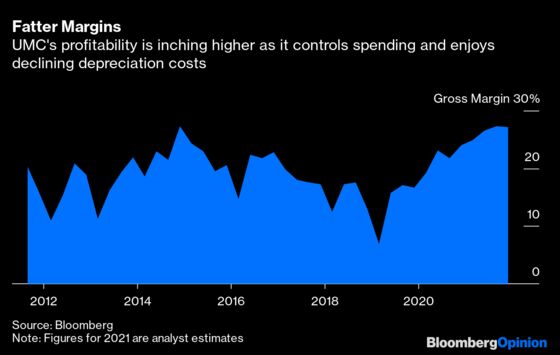

Yet this approach allows UMC to reap the benefits not only of smaller spending budgets, but lower depreciation costs that serve as the single-largest expense for semiconductor manufacturers. In fact, a lot of its equipment has been fully depreciated, at which point gross margins can jump significantly. We saw this happen last year with that figure climbing a massive 7.7 percentage points to 22.1%. Sure, such gross margin still lags behind TSMC, but investors are chasing the change in profitability, not merely the raw figure.

Another byproduct of this deliberate distant-competitor strategy is that it can largely stay out of the political crossfire between Beijing and Washington that saw TSMC forced to stop supplying leading-edge chips to companies like Huawei Technologies Co. While UMC is subject to the same restrictions, it never had to rely on a few major Chinese clients in the first place.

This spending discipline hasn’t been derailed by the current shortage. While some of the company’s capacity is in those categories of manufacturing technology that are most needed for auto chips, management has elected to focus on long-term stability of orders. So, rather than rush to expand capacity to exploit the momentary gap between demand and supply, its strategy is built around a time in the near future when the chip market will fall back into balance. As such, despite being at 100% capacity now, UMC forecasts a mere 2% increase in shipments for the full year.

That approach will limit increases in expenses, which means that improvements in earnings aren’t over yet. In January, President Jason Wang told investors that the gradual drop in depreciation is expected to continue over the next three years, meaning profitability still has room to expand. As a result, we’re likely to see gross margin inch toward its highest level in a decade. Expect investors to reward the stock accordingly.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2021 Bloomberg L.P.